Goldman Sachs is of the view that the consumer sector has seen the most widespread deceleration in the last 10 years. FY20 started off on a weaker footing than any year in the recent past with a tepid outlook for the near-term consumption.

However, the global investment bank has three buy and sell ideas for FY20 amid tough macro demand. The global investment bank has put Avenue Supermarts and ITC to 'Buy' list but downgraded Dabur India to 'Sell'.

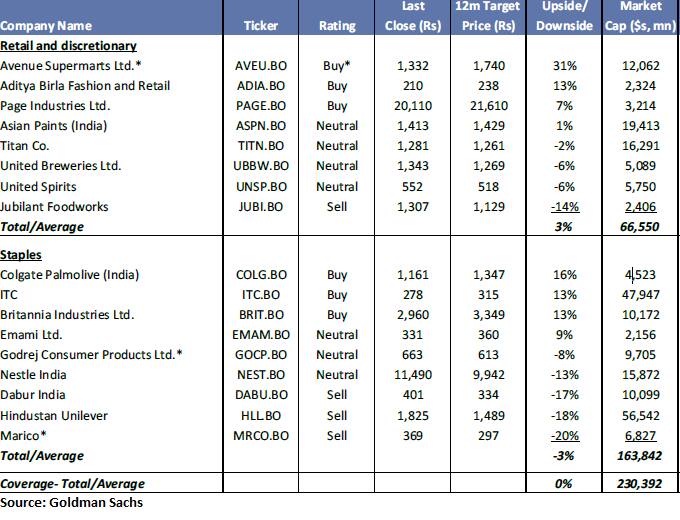

The global investment bank believes that buy ideas that include companies like Avenue Supermarts, ITC, Colgate Palmolive and Page Industries have tailwinds that insulate them from macro demand headwinds and are not yet factored into their valuations.

At the same time, its top sell ideas include Marico, Jubilant Foodworks, Dabur and Hindustan Unilever that have risks to growth that are currently not priced in.

According to Goldman, the March quarter results from consumption sector saw a slowdown in domestic revenue growth across India consumer coverage, with each of the 17 companies seeing sales growth decelerate on a year-on-year basis.

“This is the first quarter in 10 years that has seen every company in our coverage witness domestic revenue growth decelerate,” said the Goldman Sach report.

Management attributed the deceleration in demand to slower rural income growth, disruption due to general elections, liquidity constraints for the channel and a tougher base for GST-led market share gains for organised players.

Goldman Sachs expects the trend to continue for at least the next two quarters as benefits of any government measures to revive rural demand will take time to reflect in demand.

The global investment bank expects a growth in sales from 4QFY20E partly driven by softer comps.

In terms of valuations, consumer stocks have corrected from their mid-2018 peak, but remain 24 percent above the 10-year coverage average, Goldman said. For consumer staples, excluding ITC, multiples are 38 percent above the 10-year average and 12 percent above the 5-year average.

“We run a bear-case scenario, where we assume FY20 growth will continue on the trends seen in 4QFY19 and growth in FY21/FY22 will be similar to the lacklustre growth seen in FY15-18. Under this scenario, on average, we see our FY20/FY21 EPS being cut by 3/6 percent and our valuation having further downside of 13 percent,” said the report.

Goldman Sachs’s three ideas for a weak demand environment:Avenue Supermarts: Target: Rs 1,740| LTP: Rs 1,340| Upside: 30 percentGoldman Sachs added Avenue Supermarts back to the Conviction List for three main reasons. First, Avenue is likely to surprise investors on store additions. Investors have been concerned about Avenue new store additions, which missed expectations in FY19.

However, management was categorical about the company being well-positioned to accelerate store adds, with the delay in FY19 being due to regulatory factors.

Secondly, the company has significant room to grow SSSG through an increase in throughput per sqft or by increasing store area in areas where the cost of real estate is lower; and lastly, margin reset largely behind us.

Third, Avenue remains competitive on pricing while delivering strong returns. Its low-cost model is far more resilient to pricing-led competition than some peers with significantly higher operating costs.

ITC: Target: Rs 315| LTP: Rs 275| Upside: 14 percentGoldman Sachs turns positive on ITC for three reasons: (1) Moderate tax increase can spurt cigarette EBIT acceleration, (2) FMCG (others) poised to see better profitability as the business gains scale; and (3) valuations are un-demanding relative to domestic consumer peers in an environment that could see EBIT growth accelerate.

The initial underperformance was a function of a decline in cigarette volume driven by very sharp tax increases. In FY19, ITC missed expectations despite an improvement in cigarette volume growth as EBIT growth missed expectations.

Dabur India: Sell| Target: Rs 334| LTP: Rs 387| Downside: 13 percentGoldman Sachs downgraded Dabur to sell primarily because of two main reasons. Firstly, three key segments for Dabur such as juices, hair care and oral care are seeing heightened competition.

And, secondly, significant exposure to rural India, which has seen challenges to consumption growth driven by a slowdown in wages for both agricultural and non-agricultural labour.

Dabur India has amongst the highest exposure to rural India for its domestic business.

Disclaimer: The views and investment tips expressed by brokerages and research houses on Moneycontrol.com are their own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.