Shares of ICICI Bank, the country's largest private sector lender, gained more than 2 percent on October 29, but brokerage houses maintained their bullish stance on the stock and raised target price after strong numbers in quarter ended in September.

The stock rallied more than 45 percent in last one year, which indicated that most of positives seem to have priced in and the street could be waiting for more.

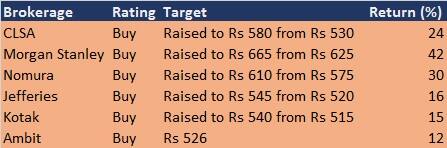

Morgan Stanley has overweight call on the stock and raised target price to Rs 665 from Rs 625 earlier, implying 42 percent potential upside from current levels as current valuations are attractive at 1.7xF21e core book and 11x Core EPS.

"Asset quality remained strong despite the weak economy. Deposit growth is the strongest in a decade. We have taken up credit cost estimates to 130 bps from 100 bps for FY20," it said.

ICICI Bank on October 26 reported a 28 percent year-on-year (YoY) decline in its September quarter profit at Rs 655 crore due to deferred tax assets adjustment (DTA), but overall earnings (except credit growth and increase in 'BB' and below rated book) were healthy with improvement in asset quality.

Here is what other brokerages say about ICICI Bank after Q2 earnings:

Brokerage: CLSA | Rating: Buy | Target: raised to Rs 580 from Rs 530

Topline growth and lower credit costs will drive earnings rebound. The Q2 core results were better than expectations with lower fresh NPLs though the profit missed forecast due to a larger reversal of a deferred tax asset.

The key disappointment was larger additions to its watchlist. Credit costs will be manageable at near 50 bps of loans.

ICICI is among the top picks in the sector as it would inch toward a 15-16 percent return on equity (RoE) over the next two years.

Brokerage: Nomura | Rating: Buy | Target: Raised to Rs 610 from Rs 575

Nomura expects 18-20 percent CAGR in core pre-provision operating profit (PPoP) over FY19-22 as Q2 was stronger-than-expected, with a 3 percent PPOP beat driven by NIM expansion.

"We are not very concerned about the more than Rs 2,000 crore of watchlist addition. We see standalone ROE at 16-17 percent by FY21-22. ICICI and Axis Bank are our preferred picks in the sector," it said.

Brokerage: Jefferies | Rating: Buy | Target: Raised to Rs 545 from Rs 520

The brokerage pencilled 1-3 percent higher core PPoP driven by better NIM and marginally lowered FY20 loan growth driving a 2-3 percent uptick in EPS over FY20-22.

It sees loan CAGR At 15.5 percent over FY19-22 and NIM around 3.7 percent for FY20-22. Fee income CAGR is seen at 15.9 percent over FY19-22 and credit cost at 98 bps over FY20-22, it said.

Brokerage: Kotak Institutional Equities | Rating: Buy | Target: Raised to Rs 540 from Rs 515

Kotak expects second half of FY20 and RoEs moving closer to 15 percent. It expects the bank to deliver on its guidance from Q1FY21.

"ICICI and SBI are preferred choices to ride the corporate recovery cycle. Trends on slippages suggest business has moved closer to best-in-class peers. Earnings trajectory should result in RoEs moving to 16 percent in FY21," it said.

Brokerage: Ambit | Rating: Buy | Target: Rs 526

Credit cost should remain elevated at 170 bps in FY20 and credit cost should moderate to 70 bps in FY21 leading to 16.5 percent RoE by FY21.

Disclaimer: The above report is compiled from information available on public platforms. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.