Engineering major ABB India is likely to report a mixed result for the second quarter (the company follows a January-December reporting calendar, and its Q3CY25 corresponds to Q2FY26). The company is scheduled to announce its earnings on November 6. ABB India provides electrification, automation, motion, and digital solutions to the industrial, utility and infrastructure sectors.

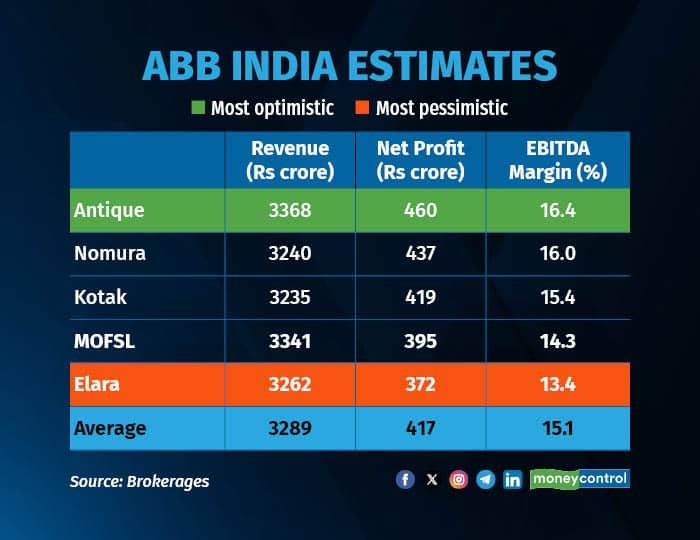

According to a Moneycontrol poll of 5 brokerages, revenue is expected to increase from Rs 2,912 crore in 3QCY24 to Rs 3,289 crore in 3QCY25, marking a projected growth of 12.95 percent. Net profit is expected to decline from Rs 440.5 crore to Rs 417 crore, a decrease of 5.33 percent, while EBITDA margin is expected to contract from 18.6 percent to 15.1 percent, a reduction of 3.5 percentage points or 18.82 percent on a relative basis.

The most optimistic of brokerages is Antique, which expects the net profit to decrease to Rs 460 crore and revenue to increase to Rs 3368 crore. On the other hand, the most pessimistic is Elara which expects net profit to decline to Rs 372 crore.

Key drivers for earnings

Growth across businesses

Revenue growth is expected to remain healthy, with brokerages forecasting 11–15 percent YoY expansion driven by stronger execution across core segments. The electrification segment is likely to lead the momentum, supported by ongoing electrification demand and QCO-related compliance-driven ordering. Kotak expects the electrification business to be the key growth engine, while other segments may remain flattish. MOFSL sees additional support from end-markets such as data centres, renewables, railways and transportation, which continue to provide structural tailwinds. Execution of base orders in Motion is also expected to support topline performance. However, revenue growth will still hinge on sustaining short-cycle momentum and converting a healthy enquiry pipeline into orders.

Margins to moderate

Margins are expected to contract owing to a combination of factors, most notably weaker pricing power amid heightened competitive intensity—particularly in the motors market—and the cost impact of QCO compliance, which has increased reliance on higher-cost imports. Kotak models a ~300 bps YoY decline in EBITDA margins, while MOFSL expects a deeper ~430 bps YoY contraction, citing additional pressure from forex volatility and pricing competition. Nomura also flags lower gross margins due to weaker pricing power. Despite the YoY moderation, Kotak expects sequential improvement as utilisation normalises and Q2 pricing pressure eases slightly.

Order inflow

Order inflow trends remain a critical driver. Kotak expects overall inflows to decline modestly YoY, primarily due to a high base of large orders last year, though it projects 7 percent YoY growth in base orders. Nomura will be watching for base order inflow momentum and any visibility on large project wins. MOFSL highlights the need for incremental inflows from transmission, railways, data centres, transportation, food & beverages, and private capex to sustain growth. Order visibility, especially in Motion and Electrification, will remain a key determinant of execution strength over the coming quarters.

What analysts will be watching for

Analysts are likely to focus on management commentary around order flows, pricing power, competitive intensity, and margin trajectory. Updates on localisation levels, export outlook and the sustainability of demand from new-age sectors such as data centres and renewables will also be key monitorables, along with the impact of QCO compliance and foreign exchange volatility on profitability.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.