“One touch, and done.” That’s how 40-year-old Manish Devulkar was introduced to the Unified Payments Interface (UPI) by a neighbour. Devulkar has been running a sandwich stall near Goregaon railway station in Mumbai for the last two decades. Soon after the COVID lockdown ended, he recalls getting agents from the fintech PhonePe to install a UPI Quick Response (QR) code at his sandwich stall. As COVID spread like wildfire, many Indians embraced digital payments in order to avoid any infection handling cash and coins. Given this reality, Devulkar needed UPI to retain and attract customers.

“Two months later, I realised my business had picked up by around 20 percent because payments had become easy and quick. Customers generally ask if they can make payment via the phone to avoid the hassle of loose change and/or to avoid a rush,” said Devulkar, as he dexterously buttered freshly made toast. More than 40 percent of his customers opt to pay via UPI now, and his monthly income has increased by around Rs 5,000.

A few metres away from Devulkar’s stall is a kirana store. Kamal Gudhka, the owner, is a veteran in the grocery business and has been running the store for the last 40 years. While he has seen many shifts in consumer spending over the years, the UPI-led “revolution” has been quite stark and noteworthy, he said.

“I started accepting UPI payments after COVID, because customers insisted on avoiding physical contact. Now, more than 50 percent of my customers pay via UPI,” said Gudhka. “In due course, I realised it saves my time in terms of keeping track of daily transactions and I do not have to haggle with consumers for loose change. It’s a win-win for all.”

Gudkha and Devulkar are not alone. Like them, millions of Indians, both merchants and customers, have embraced UPI. Thanks to this radical shift, particularly after the onset of the COVID pandemic, UPI has become part and parcel of the common man’s life. And fintechs have been at the vanguard in driving that shift.

(L-R) Manish Devulkar and Kamal Gudhka

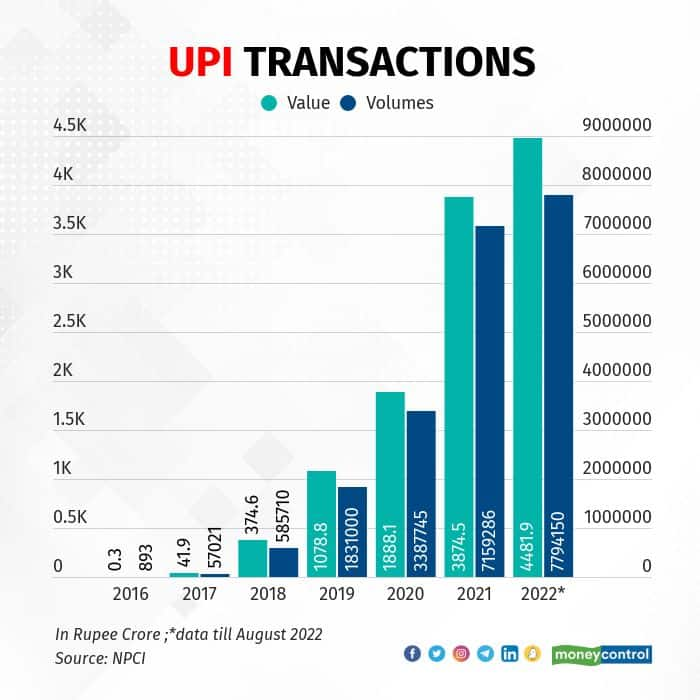

(L-R) Manish Devulkar and Kamal GudhkaThanks to the innovations and scale enabled by the fintechs, UPI is now the leading mode of retail merchant payments by value and volume, comparable to credit cards and debit cards. According to data released by the National Payments Corporation of India (NPCI), UPI reported transactions amounting to Rs 10.72 lakh crore in August 2022 alone. In FY22, UPI processed more than 46 billion transactions amounting to over Rs 84 lakh crore. In comparison, debit card spends stood at Rs 7.3 lakh crore in FY22, while credit card spends stood at Rs 9.7 lakh crore that same year, according to a CLSA report.

In terms of volume, around 47 percent of all payments made by customers in FY22 are estimated to have been made through UPI, 26 percent through credit cards, 21 percent through debit cards and 6 percent through mobile wallets, according to CLSA.

The numbers say it all. When it comes to digital payments UPI is the king.

Also read: PhonePe CEO Sameer Nigam makes renewed pitch for MDR, warns there is no path to recovery otherwise

How UPI worksWhen it was launched in 2016, little did anyone know that UPI would account for the lion’s share of retail payments in India within six years. In essence, UPI is a payment platform that allows a person to link his bank account(s) to a smartphone app and transfer money instantly, either to pay a merchant or send money to a peer. Simply put, it enables the transfer of money from one bank account to another, in a secure way.

Thanks to UPI, many Indians today no longer bother to carry a wallet in their pockets. The wallet has made its way into their smartphones, just as the camera, radio and watch did before it.

Payment championUPI was launched when the country was looking to shift towards digital payment modes, right after the demonetisation of Rs 500 and Rs 1,000 bank notes in November 2016. It got a boost when the COVID-induced nationwide lockdown in 2020 brought a chunk of users to the platform amid the increased need for safety through cashless transactions.

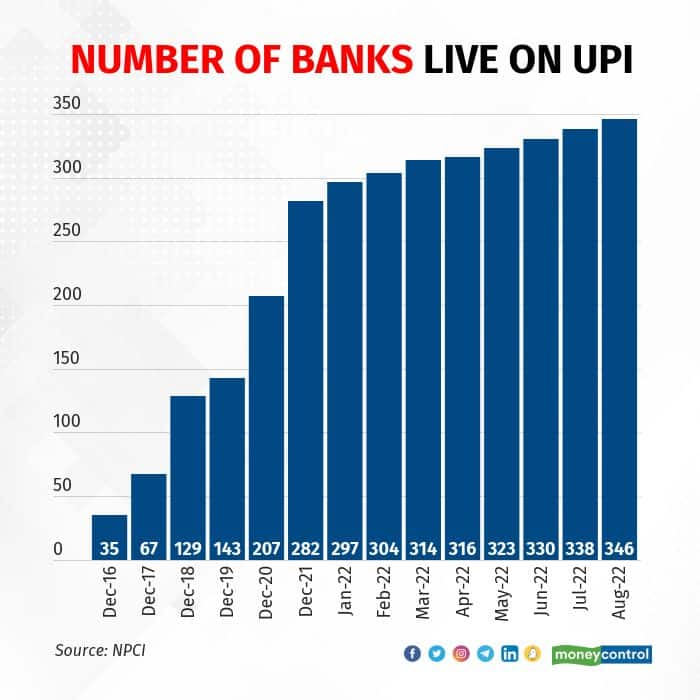

There are 346 banks live on UPI today, up from 35 in December 2016.

Recently, NPCI launched RuPay credit cards with a UPI facility. Customers can use these credit cards to make payments by scanning QR codes. This is, however, at a very early stage.

Why customers are drawn to UPIAt least five consumers Moneycontrol spoke to for this story said that they preferred UPI transactions over cash payments, largely due to the ease of payment, the safety of the transaction, and convenience. For payment receivers, it eliminates issues involving cheque defaults, counterfeit notes, tendering exact change, holding large amounts of cash, and needing to deposit it in the bank, among other benefits.

Additionally, apps such as Amazon Pay, Google Pay and Paytm offer incentives via cashbacks and reward points, luring customers to stay on the app and make payments via UPI. Paytm, for example, has tied up with popular food delivery start-up Zomato and offers cashbacks to customers.

Since the habit has set in, QR codes for UPI payments are no longer the preserve of restaurants and bigger establishments but can be seen even at roadside stalls and vegetable pushcarts.

“Right from food, grocery, childcare and domestic bills to medical and pharmacy bills, the whole payment ecosystem has gone digital, and the need for cash has been completely minimised,” said Bhagyashree Satpute, a Mumbai-based engineer. “The smartphone has completely taken over payments.”

UPI has also completely eliminated the physical transaction process, eliminating the need to visit bank branches and ATMs. Those who do visit banks are able to wrap their business up quickly as footfalls have come down thanks to UPI. The process of using UPI is also simple and user-friendly, as compared to issuing a cheque or getting a demand draft, point out users.

“My mother previously had trouble collecting rent in cash and then depositing the same in her bank account. That process was tedious and she had to depend on another family member for the same,” says Rahul Kumar, an MBA graduate. “With the help of the QR code and UPI, she gets the rent directly into her account.”

Sumit Gwalani, co-founder of Fi Money, a fintech, concurs with Kumar’s view. NEFT (National Electronic Fund Transfer) and UPI are “an example of how improved customer experience and financial inclusion go hand-in-hand,” says Gwalani, who was earlier product lead at Google Pay and was instrumental in launching the app, then known as Tez.

Interestingly, third-party apps PhonePe and Google Pay command a market share of 48 percent and 34 per cent, respectively, in monthly UPI volumes. In contrast, big banks such as State Bank of India, Yes Bank and ICICI Bank have a market share in low single digits.

“Banks are hesitant about developing a new app dedicated to UPI because that involves a lot of additional costs, besides maintenance and marketing,” said the technology head of a state-run bank, requesting anonymity.

“What we (banks) would prefer is to develop and enhance existing mobile banking applications rather than blindly aiming to take a greater share in the pie,” said the banker.

That’s where fintechs come in.

“The long-term effect of digitisation is financial inclusion at scale,” said Adhil Shetty, chief executive officer, Bankbazaar. “For the industry, digitisation also improves efficiencies and cuts costs. Fintechs have brought technology, data, and innovation. Banks have legacy, market maturity, compliance, and excellence. The result of the collaboration is great financial products.”

According to Jaikrishnan G, partner (financial services consulting) at Grant Thornton Bharat, agility and personalisation are the two key differentiators of fintechs that have left banks “far behind”.

“Today every large banker in India wants to continuously re-invent their customer journeys, bring in flexible, customisable product propositions and accelerate service delivery,” says Jaikrishnan. “Partnership with fintech players and investment in digital are top priority for all leaders in India’s banking sector,” he said.

But it is also important to note here that most of the fintechs offering UPI are not profitable, while their expenditure to drive adoption has been huge. There is no merchant discount rate (MDR) as is the case with card payments.

For instance, PhonePe reported a consolidated net loss of Rs 1,728 crore for FY21, against a consolidated loss of Rs 1,771 crore a year earlier. Paytm operator One 97 Communications posted a consolidated loss of Rs 645.4 crore for the quarter ended June 2022, against loss of Rs 382 crore in the corresponding quarter of the previous financial year.

As the pandemic ebbs, banks are stepping up credit card issuance, betting that an economic revival will lift consumer spending and lead to lower delinquencies. Lenders are coming up with innovative products, entering co-branded partnerships and luring customers with attractive cashbacks as they look to tap the ongoing festive demand.

“There are a lot of ecommerce companies and retailers coming up with attractive discounts for electronic gadgets such as smartphones,” said Rahul Poojary, a Mumbai-based product manager working for a leading pharmaceutical company. “I would definitely not withdraw cash for such payments and UPI may not be feasible because of the limit. A credit card is the best option here.”

Last September, the total number of outstanding credit cards stood at 6.50 crore. But between January and June this year, outstanding credit cards in force increased from 7.03 crore to 7.8 crore, according to data from Reserve Bank of India (RBI). The trend of higher credit card spends, according to bankers, is likely to gain momentum as the festive season approaches.

“Customers applying for a co-branded credit card are known to the merchant,” Sanjeev Moghe, President and Head - Cards and Payments, Axis Bank, had told Moneycontrol In August. “Issuing banks are better placed to underwrite these customers as they show an association with the merchant and thus, co-branded credit cards come at lower risk as compared to completely open market customers.”

Also read: Payments industry body warns scrapping MDR will kill them

Cash still rulesAccording to a Mastercard survey, cash is still seen as a "very" secure payment method among Indians. More than three out of four Indian consumers, or 76 percent, believed cash is a safer payment method, showed the survey findings. Among this group, 82 percent were between the ages of 44-57.

According to RBI’s annual report for FY22, the value of banknotes in circulation had increased 9.9 percent to Rs 31.05 lakh crore. To put that in perspective, the cash in circulation just before the demonetisation of Rs 500 and Rs 1,000 notes on November 8, 2016 stood at Rs 17.97 lakh crore. The goal of India becoming a less-cash economy is clearly still some distance away.

Also, though digital payments are the need of the hour, issues regarding data theft and cybersecurity continue to haunt consumers, which is why a complete shift towards cashless payments may not be feasible at this stage, say experts.

To minimise the risks involved in using UPI, customers should not divulge sensitive and confidential information regarding the UPI username or password or OTP (one-time password) to third parties, said Avinash Khard, Partner, DSK Legal. They should not access any unauthorised sites or provide any sensitive information to unauthorised, unknown and unverified websites or applications.

While paying via a QR Code or phone number, customers should always verify the ID of the recipient and check if the payment has reached the intended recipient or not. They should also refrain from using multiple UPI apps and logging in from various devices, added Khard.

In case such a thing happens, customers should immediately call the toll-free grievance redressal number of the bank and block the account through which the payment was made, said Khard. Customers can report unauthorised transactions to the bank, file a police complaint or call the National Cyber Crime Helpline number, he added.

(This is the second story in a Moneycontrol series highlighting the growth and evolution of the Indian fintech industry. The series intends to capture the changes fintechs have wrought in the business ecosystem and customer experience in the Indian market so far and what can be expected on the journey forward. You can read the first part here)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.