India's monetary policy has tightened rapidly over the last 12 months, with the Reserve Bank of India's (RBI) Monetary Policy Committee (MPC) raising the repo rate by 250 basis points to 6.5 percent before finally hitting pause — albeit temporarily, it has stressed — in April.

A rise in the repo rate is expected to lower inflation by curtailing demand. However, high interest rates do not necessarily lead to a slowdown. One only has to look at India's high-growth years prior to the global financial crisis, when inflation was regularly above what is now the upper-bound of the RBI's 2-6 percent tolerance band.

What matters, instead, is the real — and not nominal — interest rate.

What is the real interest rate?In common parlance, the real interest rate is the nominal interest rate adjusted for inflation. For an individual looking to make investments, it makes sense to subtract the inflation number from the rate of return on, say, a fixed deposit. If the result is negative, then the investment is not worth it.

When it comes to making decisions that have a far greater impact, such as the RBI's monetary policy decisions, the calculation of the real interest rate is not so straightforward.

To be sure, monetary policy is not primarily driven by real interest rates and it is only one of many indicators the MPC looks at. Further, it is notoriously difficult to arrive at on account of it being a derived number and can therefore be imprecise. But its importance cannot be denied and policymakers repeatedly cite it as a guiding principle.

RBI's changing definition of real ratesIn modern Indian monetary policymaking, the real interest rate first made a concrete public appearance in the latter half of 2014, when former RBI governor Raghuram Rajan started talking about raising real rates as the central bank's focus shifted from wholesale inflation to tackle the elevated Consumer Price Index (CPI) inflation that had been instrumental in households' huge gold imports as a hedge against price rises. Rajan went on to spell out a range of 1.5-2.0 percent as acceptable for real rates.

But how was this range being computed?

Interest Rates

Interest RatesIn September 2014, Rajan called the difference between the nominal rate and expectations of inflation as the expected real rate. In February 2015, he said the RBI would like the real risk-free policy rate to be 1.5-2.0 percent. In April 2015, he shed some more light on how the RBI liked to define the real rate: repo rate minus "look-forward" retail inflation.

There was a slight twist in September 2015, with Rajan defining the real rate as the difference between the yield on the 364-day Treasury bill and the one-year-ahead inflation forecast.

More recently, members of the MPC have preferred to adjust the repo rate with the one-year-ahead forecast for CPI inflation to arrive at the real rate.

Why so uncertain?The repeated changes to the real interest rate definition itself can be disconcerting as they lead to different numbers at any given point in time.

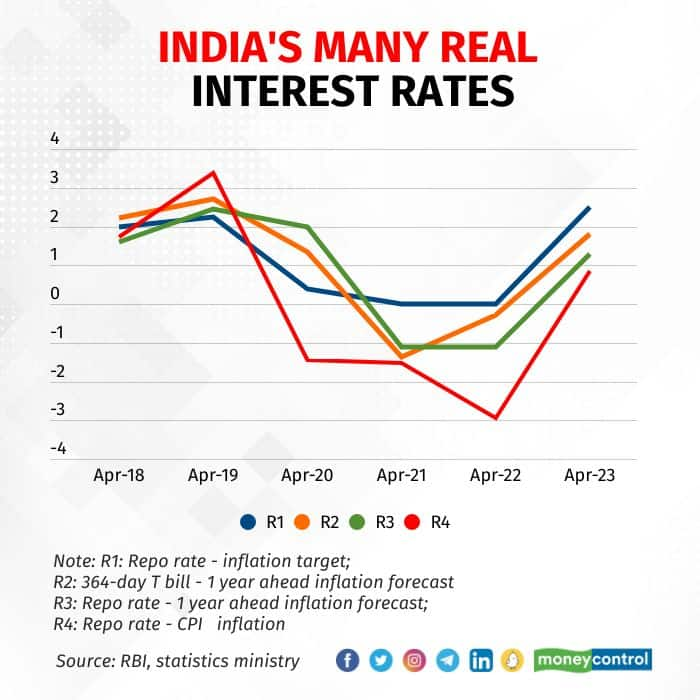

Consider the latest set of numbers. Depending on which definition one uses, the real interest rate can be as low as 0.84 percent (repo rate minus CPI inflation) or as high as 2.5 percent (repo rate minus CPI inflation target), or somewhere in between: 1.8 percent if the one-year-ahead CPI inflation forecast is subtracted from the 364-day T-bill yield and 1.3 percent if one takes it to be the difference between the repo rate and the one-year-ahead inflation forecast. These are all definitions mentioned by RBI officials over the last 10 years.

To its credit, the RBI has highlighted the subjective and imprecise nature of the real interest rate.

"We do track real interest rates, (but) there is no one standard accepted definition for it," Viral Acharya, then the deputy governor in charge of monetary policy, said in February 2019.

"My sense is most of these measures over time should co-move," Acharya had gone on to add. As the above chart shows, that is indeed the case.

By 2019, the RBI's revised range of 1.25-1.75 percent for the real interest rate had become a thumb rule of sorts for those looking for clues about the future course of monetary policy; so much so, that Governor Shaktikanta Das refused to even say what the RBI's assessment of the rate was.

"…it is for you to judge, it is for you to take a call how close we are to the real interest rate calculated by you. Somebody may calculate it slightly differently. As the central bank, I would not like to spell out a real interest rate at this point of time," Das had said in June 2019.

What is India's real interest rate?Luckily, those days of obfuscation are behind us.

The RBI and members of the MPC have been clear in what they think is the appropriate level of the real interest rate at the current juncture — 1 percent — and have seemingly decided the way it will be defined going forward: repo rate minus the one-year-ahead inflation forecast.

What has helped is that the central bank's staff have calculated the economy's natural rate of interest. According to an RBI staff paper from June 2022, India's natural rate of interest — an abstract concept used to assess the stance of monetary policy — has fallen to 0.8-1.0 percent from 1.6-1.8 percent in early 2015.

Source: 'Revisiting India’s Natural Rate of Interest', RBI Bulletin, June 2022

Source: 'Revisiting India’s Natural Rate of Interest', RBI Bulletin, June 2022If the real interest rate — as defined now – is close to the natural rate, monetary policy is said to be neutral. If it is higher, it is contractionary; if it is lower, the policy is expansionary.

Given that the RBI's real interest rate is currently around 1.3 percent, and therefore, higher than the natural rate of 0.8-1.0 percent, monetary policy is contractionary. But for how long, and to what extent can it afford to be so, given that questions are being raised about the strength of India's post-pandemic recovery?

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.