")

ITC’s Q1 FY20 sales growth of 5.8 percent YoY (year on year) was lower than our expectations, but broadly in line with the traction seen for the FMCG sector. While volume growth for cigarettes was uninspiring, improved operating performance for cigarettes and FMCG segments was noteworthy.

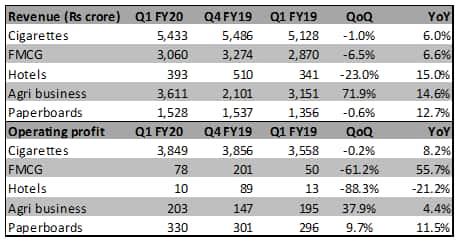

Table: Q1 Financials

Volume growth in the cigarette businesses (39 percent of Q1 sales) is estimated to be in the vicinity of 3 percent. Though this comes after a decent volume growth (7-8 percent) in the previous quarter, it signals weak traction on the demand side. However, what comes as a positive surprise is cigar operating margin has expanded by 140 bps YoY, helped by price increase to the tune of 2.5 percent. Note that margin contraction was a key concern in the previous financial year amid trend for downtrading among consumers.

FMCG sales (22 percent of total sales) grew by 8 percent YoY after excluding the impact of restructuring of Lifestyle retailing. The company highlighted that FMCG EBIT witnessed a strong move of 56 percent YoY, led by better product mix and operating leverage.

Hotels business (3 percent of sales) witnessed another strong quarter (growing 15 percent YoY) benefiting from traction in new properties (ITC Kohenur, Hyderabad, ITC Royal Bengal and ITC Grand Goa). However, additional deprecation on account of new properties impacted the segment’s earnings before interest expense and tax (EBIT).

Overall, EBITDA margin expanded by 105 bps YoY, aided by strong execution, restructuring and gross margin expansion (+180 bps).

Key negativeThough agribusiness sales expanded by 15 percent YoY, EBIT margin declined by 60 bps. The segment was impacted by weak trading opportunities in oilseeds and pulses and subdued demand for leaf tobacco in international markets.

OutlookCigarette volume growth moderated in the current quarter though improved operating performance was noticeable. As the cigarette business still contributes a major chunk of operating profit, it remains a segment to watch amid consumer demand slowdown and the competitive intensity.

Having said that, we believe that the thesis of broadening of growth levers for ITC remains on track. A few of ITC’s other businesses have witnessed encouraging traction in recent times: volume growth in the FMCG space and outlook in the hotel and paper business.

We are particularly enthused about operating leverage playing out for FMCG business. A back of the envelope calculation suggests that a normalisation of ITC’s FMCG business margins in line with its peers could help the conglomerate's overall EBITDA margin looking up ~250 bps, ceteris paribus.

Pls also read: ITC’s hospitality forays – the less talked about business interest of tobacco/FMCG giant

Furthermore, the stock (20 times FY21 estimated earnings) is trading at a significant discount to the FMCG sector’s trading multiple (~35-40x). We believe that this discount should narrow, given the stable tax regime for the cigarettes business and improving operating leverage in other businesses.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.