Madhuchanda DeyMoneycontrol Research

The great Indian debt saga has had many victims, more of them lenders than borrowers. So far we have seen very few changes in control of companies – barring Essar Oil’s deal with Rosneft and Jaiprakash Associates sale of cement assets to Ultratech.

These two deals brought some relief to beleaguered lenders. Now, with the President signing the ordinance giving the RBI more powers t tackle the bad loan mess, will the lenders finally breathe easy?

Since the NPA problem is likely to be addressed at the systemic level, high indebtedness at the individual company level will not be the only criterion of resolution.

To put it rather simply, there are many Indian companies that have very high level of indebtedness – as measured by their Debt/EBIDTA (earnings before interest, depreciation and tax) ratio. However, if the resolution doesn’t impact the banking system as a whole, these companies are unlikely to deserve significant attention.

For instance, companies like NEPC India, XL Energy, Ramswarup Industries, Uttam Galva, Mirc Electronics, Visa Steel, VIP Clothing, Shri Lakshmi Cotsyn etc. have astronomically high levels of debt/EBIDTA ratio indicating the magnitude of the debt-servicing challenge. However, their cumulative debt of little over Rs 14,000 crore is minuscule compared to the size of the overall problem, which is close to Rs 7 lakh crore.

Similarly, if we scan through the list of companies with the highest reported debt/equity ratio, it throws up names like Tanfac Industries, Sri Ramakrishna Mills, Wartyhully Estates, Webfil, C&C Construction, Deccan Chronicle, Electronica Machine Tools, Real Strips, Kanchan International, Global Vectra, KDJ Holidayscapes, and Sakthi Sugars etc. Even for this group of a dozen, the cumulative debt of Rs 8,089 crore is too small, seen in the context of the systemic problem, to deserve much focus.

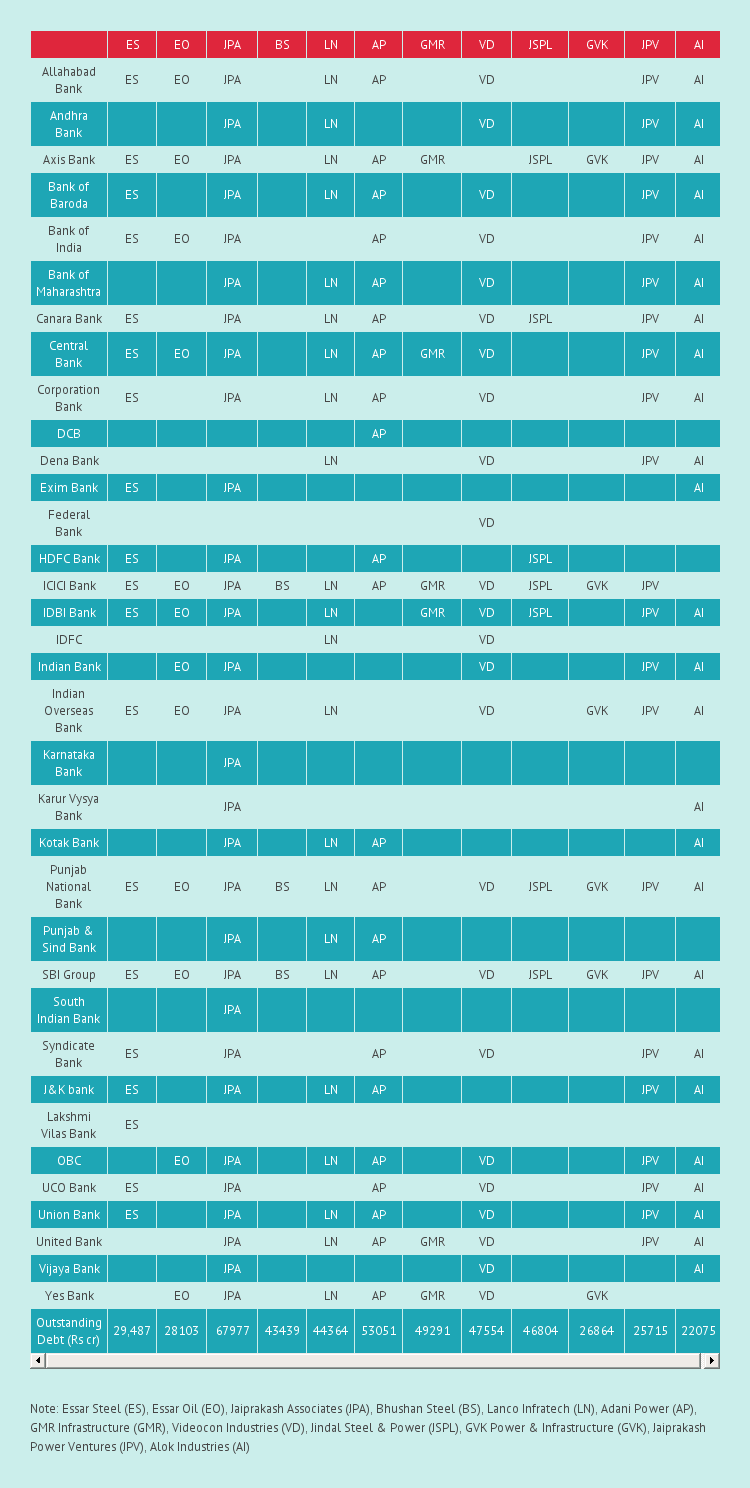

Our research throws up a dozen companies that account for around 70 percent of the Indian banking system’s current non-performing asset problem. We feel, any resolution mechanism will focus on these names as a starting point.

While the modus operandi of a resolution in each of these cases is unclear and could be a combination of asset transfer to ARC (asset reconstruction company), part conversion of debt to equity, slump sale to PSUs or getting strategic investors to these companies, the end result is likely to be unequivocally beneficial for the lenders who are presently reeling under the cloud of their business judgement gone awry.

While the Street often treats the corporate lending space as one single entity, it may be amateurish to adopt such an approach. It’s prudent to take a deep dive into these dozen companies to check who they bank with to ascertain the impact on the lenders, should the government adopt an approach that is targeted and aimed at having the maximum impact.

Jaiprakash Associates is on the top of the chart with D/E of 5.3X and Debt/EBIDTA of 13.9x. GMR, Videocon, JSPL, Lanco and Bhushan Steel have Debt/EBIDTA ratio of 10x, 23x, 12x, 16x and 20x respectively. Alok Industries and Lanco have negative networth and GVK has debt/equity ratio of 20x.

While we have no details of the exact quantum of exposure of the banks to these troubled corporates, our analysis suggests that some of the corporate-focused banking entities are lenders to most if not all of these dozen companies. Hence, in the event of any serious resolution, these lenders should gain disproportionately.

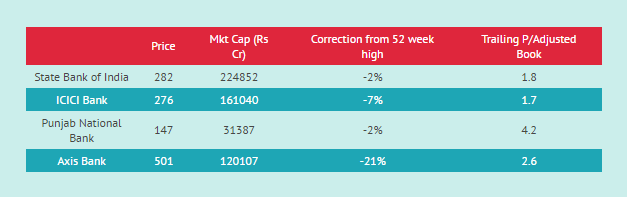

The cumulative exposure of banks to these companies is close to Rs 4,85,000 crore and hence resolution of these cases lie at the heart of India’s NPA problem. As the exhibit suggests, the banks that have exposure to most if not all these cases are State Bank of India, ICICI Bank, Punjab National Bank & Axis Bank. So, it is the big boys of Indian banking rather than the smaller, nimble-footed guys who are likely to benefit the most if any systemic resolution takes place.

The next set of gainers are going to be a bunch of public sector banks who have rarely caught the fancy of serious investors, given their poor track record in managing the problem so far. A couple of them may have negative net worth adjusted for their non-performing assets.

While the contrarian trade of backing the underdog has often captured the imagination of momentum traders, it is time for serious investors to play the contrarian.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.