As the Motor Vehicles (Amendment) Bill, 2016 edges a step closer to becoming an Act, subject to approval by the Rajya Sabha and the President, policyholders have more reasons to cheer, much to the chagrin of general insurance companies.

The Insurance Regulatory Authority Of India (IRDAI) introduced a cap of 28 percent (compared to 40 percent previously announced) on the percentage increase in insurance premiums for cars with a displacement of more than 1000cc and bikes with an engine capacity exceeding 150cc, besides leaving the premiums unchanged for the less powerful vehicles. While this, prima facie, looks like a negative update for general insurers, given the rapid expansion of the auto sector and growth in demand for third-party insurance products in recent years, an increase in the number of policyholders may possibly offset the disadvantage to some extent.

Even though an upper limit for grievous injury and death cases was proposed to the extent of Rs 5 lakh and Rs 10 lakh, respectively, in what seems to be a complete turnaround of stance, the final Bill passed in the Lok Sabha set the minimum compensation (to be awarded to the victim or his/her family only if the driver of the vehicle is not at fault) for serious injuries and loss of life at Rs 2.5 lakh and Rs 5 lakh, respectively, thereby leaving the determination of the maximum amount open-ended. To seek a higher compensation amount, the vehicle driver should be proven guilty of the offence.

Insurers have been given the right to deny claims in situations where the driver/rider does not hold a valid permit/license/policy or was under the influence of alcohol at the time of the accident. Secondly, unlike before, insurance companies can exercise a better degree of control over their claim management processes since they would not be required to pay the entire compensation amount first and then follow up with the policyholder for subsequent recovery, if necessary. Thirdly, insurers may be allowed to offer plans with varied levels of compensation too, thus giving them some degree of autonomy to charge premiums accordingly.

Will the capping of premium dent insurers’ profitability in the near to medium term?

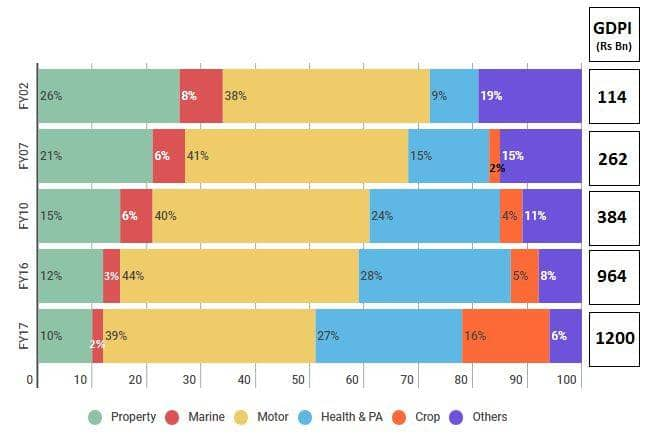

Industry Product Mix: An Overview Source - IRDAI

Source - IRDAI

IRDAI’s data reveals that the gross domestic premium income (GDPI) in respect of motor insurance constitutes around 39 percent (Rs 46,800 crore) of the Indian insurance industry’s total GDPI of Rs 1,20,000 crore. Roughly 60 percent of the motor insurance GDPI (ie Rs 28,080 crore) relates to third party insurance products, which is mandatory, whereas the balance pertains to insurance schemes for own damage, which is optional. The percentage of premium vehicles (ie two-wheelers and four-wheelers with cylinder capacities greater than 150cc and 1000cc, respectively) covered under the third party plans of indemnifiers is unlikely to be higher than 5 percent, ie not more than a GDPI of Rs 1404 crore.

Furthermore, a deeper analytical drilldown indicates that the share of private insurance players, a preferred choice by vehicle owners in recent times, in the third party indemnity space in comparison to their public sector counterparts, is not more than 42 percent, effectively indicating that the impact of the revised provisions of the Bill on vehicular insurance GDPI may be restricted to the tune of approximately Rs 590 crore only, which is insignificant.

The move to restrict the premium hike in certain categories of vehicles should result in better compliance with more riders opting for third-party insurance, consequently improving policy volumes and making roads safer. Contrary to the initial perception of a dent on insurers’ profitability, our analysis suggests that the quantum is not meaningful enough in the insurers’ overall pie to cause investors much concern.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.