I have always believed that there are two India's: one, viewed from the lens of fund managers managing local public money, i.e., " Caged Capital." And second, the India from the lens of the rest of the world.

Back in the '90s, the stock market used to experience (as I used to call it) a " 2 square mile bull market", when our entire stock market used to be clustered in the only civilized part of India: South Bombay, or Fort and Nariman Point, more precisely. The decollete of Bombay.

The rest of the country used to be untouched by the decaying charm of this 2 square mile bull market.

We, then, had none of the financial services blight of recent vintage in the armpit of Bombay, aka, Lower Parel (Alyque Padamsee spent his best years, trying to convince the un-convincables that Lower Parel 's pavements would miraculously improve if we started calling it Upper Worli, which, let's accept it, was a far prettier name. But somehow, the malodorous charm of Lower Parel stuck on).

And horror of horrors, the financial industry found its way to the groin of Bombay, Andheri, and then, even to the Prostate of Bombay, Thane, etc.

Last five years, the equity cult has even reached Purulia.

Viewed from the occiput of investors of Caged Capital, India was this beautiful damsel wrapped in a gossamer dream: endless growth.

Surprisingly, the damsel actually even delivered. On equity market returns, anyway.

On the other hand, Uncaged Capital, the capital that luxuriates in Manhattan, London, Singapore, never found India alluring. Visually, that is. But they held their noses, drove through and around the garbage called urban India, and bought quite amazing companies by the dumpster-truckload. It was an extraordinary act of patriotism by folks who were not even citizens.

In fact, it was an article of faith for our generation that FIIs (F2s as the Kalkatiyas would colloquially call them) would always support India. And F2s obliged, almost without fail.

But not anymore.

Uncaged and unimpressed

Now, this Uncaged Capital doesn't like India. In the past 12 years, we have had about 10 years of net secondary market outflows from F2s. The pace has increased markedly in the last two or three years but that is simply a function of their being given graceful, knife- through- butter exits by folks from Mofussil India. You can only sell if somebody is buying. If there is no buyer, there is no sale and vice versa. The massive inflows from local investors have made massive outflows by foreigners possible.

But of course, outflows always match inflows, and have no lasting impact on market direction, even though lazy 'analysis' by lazy financial pros tells us they do.

But this time, something seems broken with the chiffon-clad, Yash Raj Films sylph: the chiffon is fraying, if not downright tattered.

Four types of Bear Markets

You see, Bear Markets in a stock, sector or country can be of four types.

Type 1 Bear Market: the security in question collapses in absolute terms by 20-80%, and something similar in FX and relative terms.

Type 2 Bear Market: the Security in question doesn't collapse in absolute terms, but relative to the rest of securities, it collapses. Basically, it can mean that (almost) everything else rallies a lot while this security remains flat. Think HUL for a decade after its highs of the late 90s: the stock did nothing, while the Sensex did very well. So HUL was in a relative Bear Market.

Type 3 Bear Market: This happens in context of a country, generally: this is when a country's index is flat-ish, but the currency depreciates a ton, so in FX terms, the country enters a bear market.

Type 4: An overall Bear Market where pretty much everything falls similarly in absolute terms. Think 2008.

Now, when you start looking at what defines a bear market this way, you start to understand what kind of pickle we are in. And there is no getting away from the unspeakable conclusion: India is in a Bear Market all right. A Type 2 locked in conjugal bliss with a Type 3 one, but that doesn't make it any less problematic.

Let's look at some data, shall we?

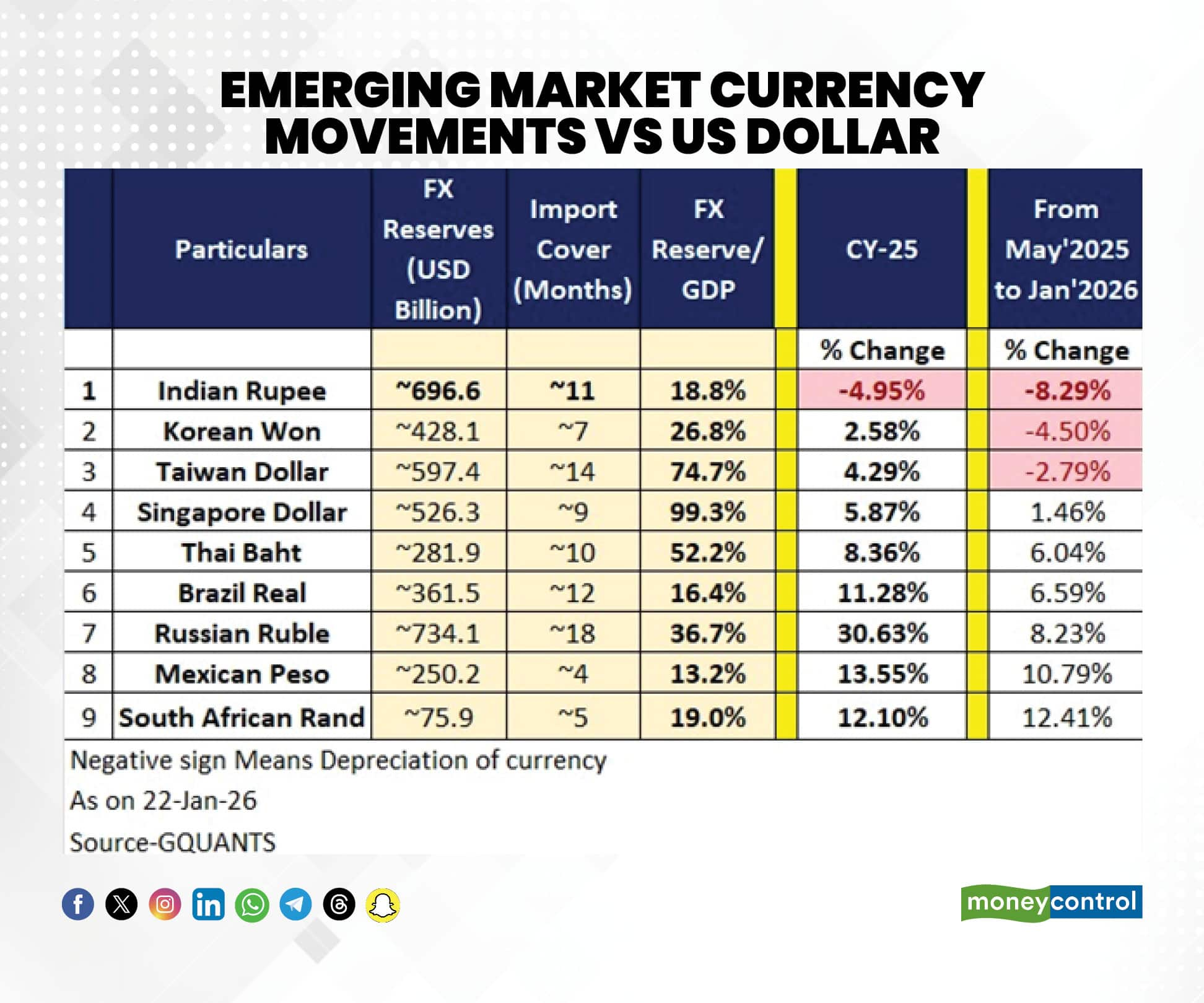

First, the currency

The dreaded Fragile One Category

If you look at the performance of the Indian rupee in calendar year 2025, it makes almost the entire emerging market currency basket look stellar: the Russian Rouble , the Brazilian Real, and horror of horrors, the Thai Baht, have trounced the INR much like Australia did England in the Ashes.

Even a longer 5-6 year analysis of the INR's trajectory isn't chicken soup for the soul: it has lost around 37% Vs the USD since 2019, the worst of any well-bred currency.

The more recent data points for the Indian rupee since the real syncope started in May, are even more sepulchral: in the general peer group, it is the worst performing one, by a factor of 2.

Let's sashay onto Equity markets now:

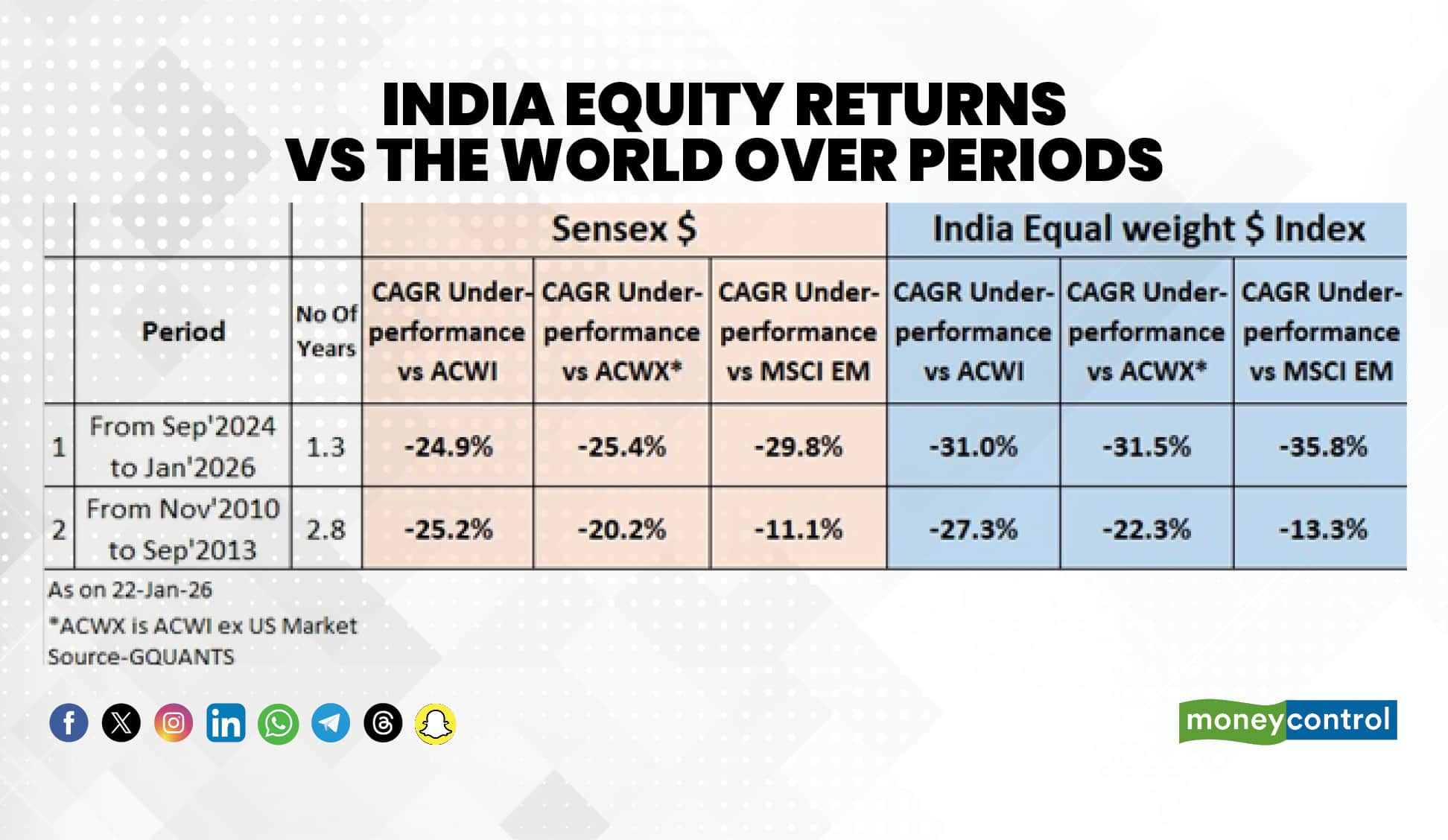

The performance, or rather, the lack of it, for the Indian equity markets relative to the world tells us how the Type 2 and Type 3 Bear Markets conjugate, much like glucose attaches to hemoglobin, giving you your HB1AC.

Indian social media, the largest refuse landfill excluding Delhi "s Ghazipur, is full of stuff like " The NIFTY is down only 5-6% so why the maudlin mood ". That's sophistry, or maybe, just plain idiocy.

Table 2 lays bare the Emperor: India's performance in US dollar terms, relative to the All Country World Index ( ACWI), to the ACWI excluding the US, and to Emerging Markets, is the tale few Financial TV anchors will tell.

The Sensex in dollar terms, solidly hugs the bottom decile of house -broken markets. But when we expand this to an equal weight Index, that we at Gquant use, for the entire Indian market, the picture becomes rather macabre: the broad market has had a relative collapse of astonishing magnitude: in fact, it puts to shame the much reviled 2010-2013 period, when India was put by some low IQ British analyst in London in some category called " Fragile Five".

India's current performance is between 2 and 3 times worse than India's performance in the 2010-13 period Vs the ACWI ex US, and Emerging Markets Indices. The Gquant All India Equal Weight Index goes down the same potholed road as its vaunted brethren, the Sensex and the NIFTY.

It's not just underperformance; the speed of it is shocking

Keep in mind also a crucial detail: the time period in which this under -performance has happened: this time around, India has lagged quickly and furiously, in a compressed snapshot, like an unclassy T20 game.

Our underperformance of lower magnitude in the 2010-13 period was more protracted. This time, metaphorically, a lifetime of performance lag has been isostatically compacted into a single brutal year.

So what explains all this?

To be honest, almost all Indian investors with Caged Capital, are presently suffering from a rare medical condition called Anosognosis: the patient doesn't understand what he's suffering from. But suffering, he is.

The perplexing thing is that based on the data of forex reserves, India does not seem to be in the worst category but the currency clearly is. The answer to this riddle eludes me, save for a fig leaf masquerading as serious analysis: that forex markets perceive a far more uncertain Indian macro environment than what is currently meeting the eye.

Net FDI is a problem

However, I would've been less worried about simply an equity market lag had it not been accompanied by a massive FII exodus, but equally, a net FDI figure that is looking more North Africa than rocking Asia.

Our Balance of Payments (BoP) has had numbers like +$ 15 billion to + $65 billion over the past 25 years. Negative figures have been few and far between, and generally, in crisis years, like 2008-9.

But we had a negative $5 billion in FY25, and this year, looks shaky as well. Overall, for the two years combined, we could end up at near zero. That's probably best case.

Net FDI is also phantasmal today: we are getting around $5-10 billion last couple of years. To lend some perspective, even in the Pro-Max crisis 2008-09 years, we got close to $40 billion! I will not even get into calculating these figures as a percentage of GDP.

A net FDI collapse is far more perilous than an FII exodus. FDI is like molasses. FII is like In dian whiskey. They flow very differently even though they have the same origins.

(To be fair, the gross FDI figures are still good, at around $60-80 billion, but what matters to the currency is ultimately the BoP.)

One of the critical things I look for while making broad macro investment decisions is this: if the bear market falls in the category of Type 1, 2, 3, whether it is for a stock or a country, I would tend to be extremely cautious. Because those point to a specific problem in a specific security which could well be a country.

This time India is in the Type 2 x Type 3 Bear Market. (We certainly hope it does not become a Type 1 variant). And that is because there is no bear market pretty much anywhere else in the world. 2025 was an extraordinarily profitable year for anybody with an IQ above 50, doing Global macro.

To some extent, India's Bear market is the correction of a period of excess returns which started from the pandemic lows. This was posited by me in Lake of Returns Theory prediction made a couple of years ago that the next few years from India would be a period of near zero Returns.

However, for India to have done this poorly in a period of quite magnificent Global investing environment, across regions and asset classes, is quite out of character with India's long term relative performance.

Post-tax returns aren’t attractive

I have mentioned several times in the last one year about how our policies have made our national fisc dangerously dependent on equity markets IE, "stockmarketification" of the Budget. The point that has been missed in this is that taxation on equity investing has made equity investing very unattractive, whether for domestic or foreign investors.

Quite frankly, if all that the equity markets in India promise are around 8-9% CAGR in INR terms, after factoring in capital gains taxes (average 15%), annual volatility of ~10%, the net returns of around 6-7% are a poor bargain. For foreigners, even less so.

We need policy to be ego-free. We need policy thinking to be absorbent of current reality, and not of Excel fantasies. (Let's leave that to analysts & Indian social media)

Because we never can tell when chest -thumping alchemizes into chest -beating.

(Shankar Sharma is a well-known investor, and Founder of GQ FinXRay at Gquant, an AI firm.)

Views are personal and do not represent the stand of this publication.

")

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.