With consumer inflation plunging to a 5-year low, calls for a rate cut ahead of the RBI’s policy meet in August have got louder. Chief Economic Advisor Arvind Subramanian added to the pressure on RBI by remarking that policymakers must reflect “very very carefully” on the latest macro economic data.

RBI had begun the fiscal on a hawkish note in its April policy and then softened its tone in the June policy. But a rate cut at the upcoming policy meet on August 1-2, cannot be taken for granted.

The central bank had flagged five concerns while sounding hawkish in April.

In the recently released Financial Stability Report, the RBI has said that weak investment demand because of a double whammy of a debt-saddled corporate sector and stressed banking sector is a major challenge. And while they are an alternate source of funds, NBFCs, mutual funds and the capital market cannot fully substitute for banks. Hence, steps to restore the health of the banks assume urgency.

Against this backdrop let us explore what factors could possibly lead to a much disappointing pause from the RBI once again.

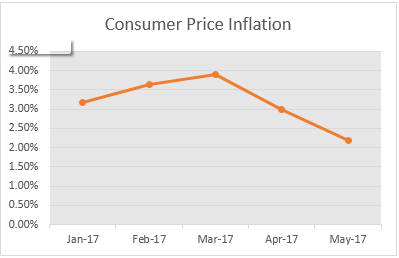

Soft PricesCPI inflation slipped to a record low of 1.54 percent in June compared to 2.18 percent in May and 2.99 percent in April, led largely by favorable base effect and weak core inflation. Core inflation slipped to a record low of 3.73 percent, down from 4.13 percent in May.

What could still weigh on RBI’s thought process is the inclusion of 106 percent HRA (house rent allowance) increase of central government employees from July and assuming if one-third of the states implement a similar increase from January 2018. The recent sharp uptick in fruits and vegetables prices could also be a cause for worry, although disinflation in pulses and muted price pressure in cereals coupled with prompt government intervention are expected to contain sharp surge in food inflation.

Till July 11, India received 260 mm of rains, a mere 1 percent short of normal. Usually, the monsoon enters into a ‘break,’ in the middle of July and sometimes August. If the breaks were to last too long, it could be a cause for concern. Most regions in India have got their normal quota of rains except a few.

Why Monsoon Is Critical For India And Its EconomyWeak GrowthThe Index of Industrial Production (much more broad-based now, post the revamp of the index) is also following CPI closely in its decline. IIP for May 2017 stood at 1.7 percent versus 2.8 percent in April. While weakness in May could be partially be attributed to de-stocking in the run-up to GST implementation, what is worth noting is the sizeable downward revisions in the February and April indices. With GST implementation likely to impact business for a quarter or two, IIP numbers are unlikely to look up in a hurry.

The moot question remains will RBI act on the softer IIP or will it wait for the first quarter GDP print to be released on August 31? It is worthwhile to note that RBI has revised down its growth for FY18 in its last policy by 10 bps to 7.3 per cent.

While there appears to be a near consensus on the imperative to act on the basis of soft growth and equally soft prices, what else matters to the RBI?

First and foremost, the resolution of the bad debt problem that could free up banking sector balance sheet. While the government has put the RBI on the drivers’ seat and a big bang beginning has been made with the identification of the first dozen troubled companies, the spate of litigation can slowdown the process.

Farm loan waiver, that starter with UP has now spread like wild fire with Maharashtra, Punjab, Karnataka joining the fray. There is high probability that more states like Madhya Pradesh, Gujarat, Rajasthan, Haryana, may join the bandwagon. These farm loan waivers could be funded by debt issuance rather than expenditure cuts and even if the state government staggers the fiscal burden over 3-4 years, it will still imply annual fiscal cost of 0.3-0.5 percent of Gross State Domestic Product.

On the global front, growth appears to be coming back in the developed world and central banks look set for unwinding accommodative policy stance. The impact of the same on commodity prices, flows to emerging markets and currency would also deserve RBI’s attention.

So while we might endlessly argue for a rate cut in August and the movement of the ten-year G Sec also appears to be suggesting the same, let us trust the judgement of the expert – RBI.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.