State-owned banks have emerged as relative winners in the Reserve Bank of India’s (RBI) rate cut cycle, managing to protect their net interest margins (NIMs) far better than private-sector lenders.

Even as the easing of policy rates put pressure on lending yields across the banking system, lower funding costs and a stronger, more stable deposit franchise helped public-sector banks (PSBs) cushion the impact, analysts said.

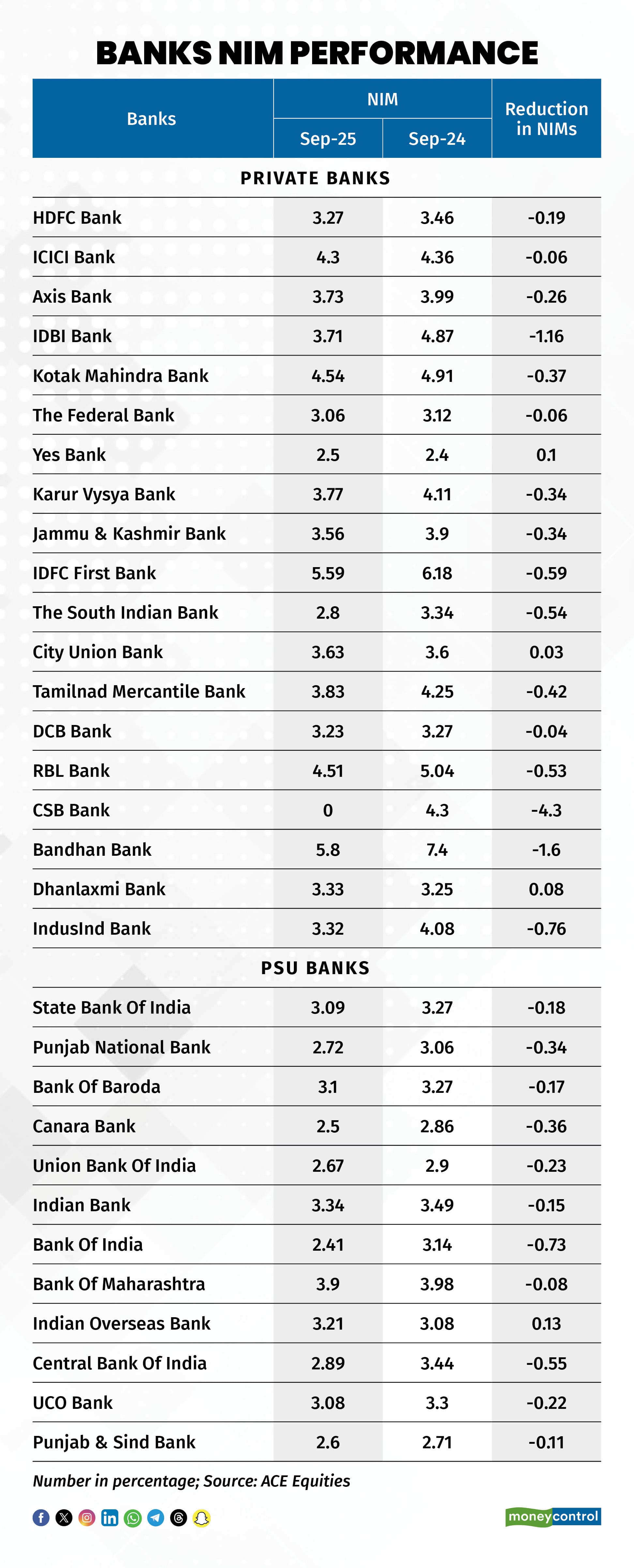

According to data compiled by Moneycontrol, PSBs reported a contraction in NIMs in the range of 8–73 basis points in Q2FY26. In contrast, private banks saw a much sharper compression, with margins declining by 8–116 basis points during the same period. ICICI Bank saw lowest margin erosion of 6 bps, whereas, Bandhan Bank saw 116 bps margin erosion.

This was on back of 125 basis points (Bps) rate cut by the RBI in 2025 to support growth, which was lagging for few quarters.

Banks NIM performance

Banks NIM performance

Funding Costs & Deposit Mix:

One of the biggest factors in this divergence has been the cost of funds. PSBs typically have a higher share of low-cost current and savings account (CASA) deposits and a deep, relationship-driven deposit franchise.

These liabilities reprice more slowly and provide more insulation when benchmark rates fall. By contrast, many private banks depend more on bulk and market-linked deposits, which reprice more quickly and can keep funding costs elevated even as lending yields fall.

The RBI’s rate cuts cumulative reductions of 125 basis points in the year 2025, has been transmitted into lower loan yields across the system, albeit the December policy reduction of 25 bps, which is work in progress from a transmission perspective for banks. TTtransmission has been faster on the asset side than on the liability side, especially for private banks, which tend to have larger portfolios of external benchmark-linked loans. Deposit costs in many cases lag the decline in lending rates, squeezing spreads, experts said.

How much rate transmission taken place for banks?

In response to the cumulative 100 basis points reduction in the policy repo rate during February-October 2025, banks have reduced their external benchmark-based lending rates on fresh loans linked to repo rate by the same magnitude.

The weighted average lending rates on both fresh and outstanding rupee loans also eased during this period. On the deposit side, banks reduced interest rates on fresh term deposits significantly.

The decline in the weighted average lending rate on fresh and outstanding rupee loans was higher in the case of private banks relative to public sector banks. On the deposit side, transmission was higher for public sector banks compared to private banks in case of fresh term deposits.

According to the RBI’s data, transmission of 100 bps rate cut on fresh rupee loans by PSU banks were lower at 70 bps, as compared to 105 bps for private banks. Similarly, on the fresh loan, it stood at 57 bps for PSU banks and 90 bps for private banks.

On the deposit side, PSU banks leads the transmission with 104 bps on fresh deposit, as compared to 99 bps for private banks.

Outlook

According to Sachin Sachdeva, Vice President & Sector Head – Financial Sector Ratings at ICRA, the outlook for India’s banking sector remains stable for FY2026. Banks are not expected to face major capital-raising needs, supported by healthy credit growth across retail and MSME segments.

The anticipated improvement in net interest margins from Q3 FY2026, as deposit repricing progressed, is expected to get slightly delayed because of recent rate cut. ICRA will continue to track margin trends and credit quality of unsecured loans and MSME amid global macro-economic developments, Sachdeva added.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.