Highlights:- - The inorganic growth initiative would help diversify ABFRL’s business

- Revenue traction would be visible right away

- Margins in the new segments may remain under pressure

- ABFRL’s stock is consideration-worthy for the long haul

--------------------------------------------------

By virtue of taking over Jaypore and TG Apparel, Aditya Birla Fashion and Retail (ABFRL) is moving into ethnic wear, a fast-growing and promising market in the Indian context.

However, considering the heavy upcoming spends on brand building and store infrastructure set-up, it may take a while for any sign of profitability to be visible from these acquisitions.

Deal contours - Buyer: ABFRL

- Entities to be acquired: Jaypore E-commerce Pvt Ltd, TG Apparel and Décor

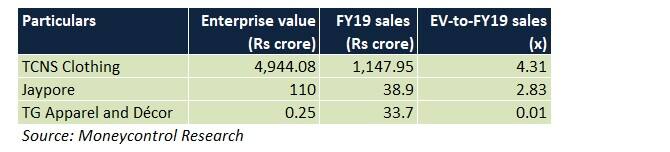

- Enterprise value: Rs 110 crore (Jaypore), Rs 25 lakh (TG Apparel)

- Completion timeline: 30-45 days

About Jaypore

Jaypore is a B2B (business-to-business) online-cum-offline retailer. It sells curated collections of apparel (hand-made, -woven and -crafted), jewellery (fashion and silver variants), gift items, home textiles and craft articles from different parts of India. It clocked sales of Rs 38.9 crore in FY19.

About TG Apparel and Décor

It is a B2C (business-to-consumer) online-cum-offline retailer of ethnic fashion clothing and accessories. The company reported a turnover of Rs 33.7 crore in FY19.

How does ABFRL benefit?

Foray into ethnic wear

While ABFRL has been active in the women’s wear space (through Pantaloons), Jaypore and TG Apparel’s acquisitions would help the company strengthen its presence in the ethnic category. In men’s wear, the company, as of now, doesn’t have too many ethnic offerings.

Owing to a high number of festivities and marriages in the country every year, demand for such products is fairly steady (growing in double digits, according to the management), even if there is some degree of seasonality.

New segments

Inclusion of new product lines such as jewellery, home, textile and art -- traditional and contemporary -- products in ABFRL’s portfolio would help it reach out to a new set of customers. This also provides cross-selling opportunities since ABFRL’s core products (under the brands - Van Heusen, Allen Solly, Peter England, Louis Philippe and Pantaloons) may be under the same roof as well.

Better access to export markets

Jaypore sells its products in more than 60 countries worldwide. This, by itself, is a large market for ABFRL to capitalise on.

Outlook

Though the move will help ABFRL drive its top-line growth, in our view, significant investments will have to be undertaken to penetrate the target markets. These would be in areas like store additions, inventory management, marketing and dealer margins. This may necessitate a new round of borrowings amid the ongoing debt repayment drive.

Flat revenue in the case of both the acquired companies for the last three financial years is also a cause of concern. Competition from established brands such as TCNS Clothing, Manyavar, Biba and numerous other local/unorganised players across geographies will also persist. Thus, ethnic wear margins may be pretty low in initial years.

To some extent, this, in turn, may offset the strong set of numbers that the Madura segment -- a cash cow for the company -- is capable of delivering and improving operational metrics in the Pantaloons segment.

Since TCNS Clothing’s revenue base and store network are significantly higher than Jaypore’s, it is not surprising to see it command rich valuations compared to Jaypore. Nevertheless, prima facie, it appears that the EV/FY19 sales multiple of nearly 3 times for Jaypore is pretty demanding.

Initial impressions suggest that TG Apparel, in all likelihood, may not be as profitable as Jaypore. Hence, it is being acquired at a considerably lower valuation multiple.

Keeping the above-mentioned factors in mind, we believe the disruption in ABFRL’s short-term cash flows (because of these deals) can be neutralised once economies of scale and size are visible from Jaypore’s and TG Apparel’s online and brick-and-mortar verticals.

ABFRL’s stock trades at a steep 40 times its FY21 projected earnings. Though the scope for an appreciable upside is restricted, the possibility of a sharp price correction is unlikely, too. Nonetheless, investors may still want to keep the company on their checklist.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.