Ten days ago, the Reserve Bank of India (RBI) permitted a proposal by financial services firm Centrum Financial Services to take over the troubled Punjab and Maharashtra Co-operative (PMC) Bank. Centrum, along with payment service company BharatPe, is poised to form a small finance bank to run the co-operative bank under an RBI-supervised amalgamation scheme that will be announced soon.

The RBI action ends nearly two years of uncertainty for PMC Bank depositors who have been anxiously waiting to get their money back. Several of them survived on charity and loans.

A quick recap is in order because it is a two-year-old case.

In September 2019, RBI imposed restrictions on the bank after discovering financial irregularities, including under-reporting of bad loans. Around 9 lakh depositors were bound by curbs on withdrawing money. PMC’s dire finances intensified worries about the health of India's financial institutions, coming as it did after the IL&FS collapse. The case is also mired in a litany of litigations.

After the torrent of bad news, the RBI-orchestrated resolution finally spells good news for depositors. Yet, it begs the question: how did things come to such a pass? Could the PMC Bank crisis have been averted?

New evidence unearthed by Moneycontrol shows that there were enough alarm bells that could have prevented, if not alleviated, the troubles that PMC Bank sank into.

As early as 2011—eight years before the PMC Bank scam became public—the RBI was warned about the shenanigans at the bank by a whistleblower.

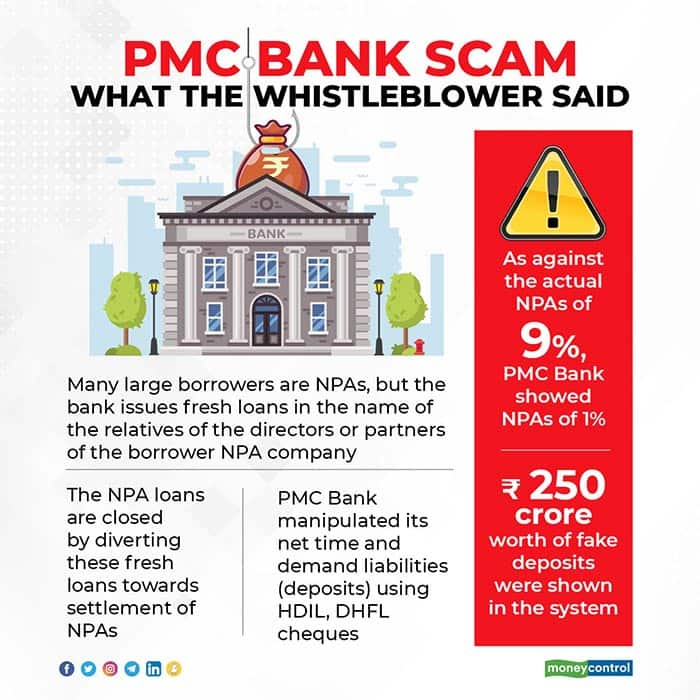

On January 28, 2011, the whistleblower—an employee of PMC Bank— shot off a letter to A Udgata, chief general manager-in-charge of Reserve Bank of India (RBI)’s Urban Banks Department. The letter raised a raft of alarming violations of rules in the Mumbai-based co-operative bank. It especially highlighted the bank’s dealings with two entities named Housing Development and Infrastructure Ltd (HDIL) and Dewan Housing Finance Corporation (DHFL).

DHFL was once one of India’s top non-banking finance companies, or so-called shadow lenders, but would later collapse under the weight of debt. Realty company HDIL would become bankrupt.

The letter underscored the nexus between PMC Bank brass and the two companies, which were controlled by the same family—the Wadhawans. The Wadhawans are now facing a litany of investigations into various financial irregularities.

PMC Bank manipulated its net time and demand liabilities (deposits) using HDIL, according to the letter. “In return, all black money of HDIL and group companies which are received in cash are deposited in the bank accounts of PMC Bank and these cash deposits, above the specified limits, are not reported to the RBI or sometimes window dressed so that RBI cannot make out that black money is being made white here,” said the letter.

The whistleblower was not immediately available for comment. Moneycontrol is ergo withholding the identity.

In the letter, the whistle-blower also warned about gross underreporting of non-performing assets (NPAs), evergreening of loans, fudging of loan accounts and entry of fake deposits.

Several warningsAs against the actual NPAs of 9 percent, the bank showed NPAs of 1 per cent. Many large borrowers were related to the directors of the bank and bank executives were asked to manipulate the accounts to facilitate loan sanction by creating fresh proprietary firms and issuing new loans to these companies to close earlier NPAs, the letter said.

Fake deposits were shown to inflate the loan book, the whistleblower complained. “About Rs 250 crores of deposits are updated in the system as fake deposits, just to portray themselves as big banks and receive awards …,” the letter said.

The whistleblower asked RBI to investigate these violations.

What did the RBI do?

The central bank acknowledged receipt of the letter. It then sent a letter on March 7, 2011, to the chief executive officer (CEO) of PMC Bank asking him to investigate the issue and give a response to the regulator.

The then CEO was a man named Joy Thomas, who was arrested by The Economic Offences Wing (EOW) of Mumbai Police on October 4, 2019. Investigations revealed that Thomas led a double life converting to Islam with the name, Junaid Khan to marry his personal assistant and gifted her nine flats in Pune.

Moneycontrol has reviewed a copy of the RBI letter. RBI did not comment for this article.

The whistleblower essentially alerted about the abject collapse of corporate governance and rampant fraudulent practices. Those wrongdoings would grow into a full-blown scam because the person assigned to investigate was allegedly one of the protagonists of the scam.

Talk about letting the fox guard the henhouse.

The EOW also found the bank officials replaced 44 loan accounts of HDIL with 21,049 fictitious accounts to camouflage huge loan defaults by the real estate group. This action would play a vital role in landing PMC Bank in the current crisis.

Another shot at checks and balancesThe RBI had another crack at halting PMC’s descent into financial ruin.

In 2018-2019, statutory auditors handed PMC Bank an audit classification ‘A’ rating. The ‘A’ audit classification is the highest rating for such exercises, signalling things are kosher at a financial institution.

This rating was given at a time when a massive fraud was gnawing at the bank and its balance sheet was fudged with large scale underreporting of NPAs.

The ‘A’ audit classification given by the statutory auditors finds mention in the bank’s 2018-19 annual report. The role of the auditors, Lakdawala and Co, has since come up for question in the light of the massive scam.

Moneycontrol couldn’t contact the auditors as no email address or website is available. The copy will be updated if they reach out with a comment.

The RBI inspects a co-operative bank once in 18 months based on audit reports. PMC Bank’s auditors not only failed to unearth gross financial irregularities in the bank for years, but continued to give top audit classification to the bank.

If the auditors had done their job, depositors could have been warned of the impending crisis.

A curious appointmentSoon after the whistleblower’s letter reached the RBI, a former senior RBI official joined PMC bank as general manager in charge of HR and training.

LN Kamble, who served in the RBI’s Department of Urban Cooperative Bank supervision, joined PMC Bank as general manager two months after he retired in March 2012.

Kamble held on to the post between 2012 and 2019—when the scam festered— and resigned in October 2019. That was one month after the RBI superseded the PMC Board.

Kamble also happened to be the chairman of the RBI Officers’ Credit Society that deposited Rs 100 crore in PMC Bank. RBI Officers’ Credit Society, the Reserve Bank Officers' Cooperative Credit Society Ltd (RBOCCS) and Reserve Bank Staff & Officers Co. Op. Credit Society Ltd together deposited nearly Rs 190 crore in PMC Bank.

According to Section 37 A of the RBI staff regulations, no officer of the central bank can take up private employment after exit either by resignation or retirement. To do so, an officer requires the permission of the RBI governor.

Kamble told Moneycontrol that he received all necessary permission from the RBI to join PMC Bank and his role in the bank was centred on HR and training.

“I was among the two general managers in PMC Bank. None of us had access to the credit department. I was in charge of HR and training in the bank,” Kamble said.

Kamble said the PMC Bank scam was due to the creation of fake FDs after the credit exposure limit to HDIL was hit, adding that under rules for loan against FDs, there is no limit.

“Nobody was aware of this scam.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.