Similar to other pharma stocks, the market has not spared Jubilant Life Sciences in recent months, crushing its share price to Rs 500 level from an all-time high of Rs 1,039 in February 2018.

However, analysts now expect the stock to outperform and breach Rs 1,000-mark in the next 12 months, driven by the potency of speciality business. This translates into up to 100 percent gain from current levels.

According to analysts at IDBI Capital, Jubilant Life's performance would be driven by market share gains in key radiopharmaceutical products, a ramp-up in CMO business with new clients/capacity additions, capacity additions in finished dosages and Life Science Chemical (LSI) segment and opportunities from the supply of ethanol to government.

"Jubilant emerged as a key beneficiary of the uptick in speciality pharma, generics and favourable pricing environment in its chemical business during FY16-19. While some of the benefits have started eluding the company, we do not see structural changes in industry dynamics. We expect revenue and adjusted PAT CAGR of 9 percent and 17 percent over FY19-21," said the brokerage.

ICICIdirect expects the pharmacy business of the company to grow at 20 percent CAGR in FY18-21E to Rs 7,097 crore and the speciality sub-segment to grow 20.5 percent CAGR in FY18-21E to Rs 3,856 crore, on the back of the recent long term contracts in the radiopharma business, as well as approval for Rubyfill, in the US. Rubyfill is the radiopharma product of Jubilant Life Sciences.

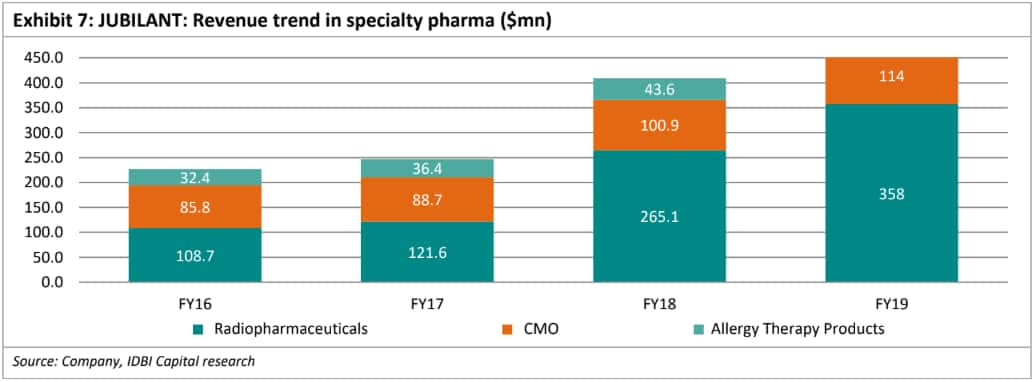

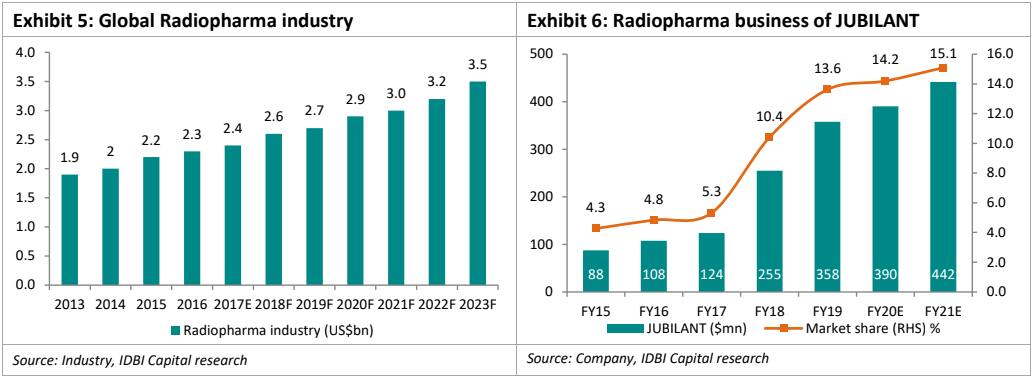

"The radiopharma industry is currently estimated at $2.6 billion and is growing at 6 percent annually. With 14 products in the market, Jubliant commands a 10 percent market share in the US," said IDBI Capital.

IDBI expects a resurgence in LSI business, which includes speciality intermediates, nutritional products and life science chemicals. The segment was under pressure in the last fiscal, declining 38 percent in the fourth quarter of FY2018-19.

"Past few quarters witnessed lumpiness in its Vitamin-B3 (low demand) and Acetyl (drop in global prices). However, we expect the demand for Vitamin-B3 to improve and prices of Acetic acid to stabilize in H2FY20. We expect LSI business to post 15 percent CAGR over FY19-21E," said IDBI.

Meanwhile, ICICI hypothesized that despite showing good potential in the past, LSI remains more or a less a commodity play, the prospects of which hinges upon the global commodity cycle.

"On the LSI front, despite inventory adjustment, EBITDA margins were disappointing and things are unlikely to improve in the next few quarters," said ICICI Direct.

While analysts maintained a positive outlook for Jubilant Life Sciences, the company has received warning letters from USFDA, which can dampen growth.

The USFDA recently issued a warning letter to the company's Roorkee facility, after notifying two lapses on GMP compliances, which is set to block new approvals.

It also issued form 483s on its Nanjangud API facility with 12 observations and the unit has been classified at official action initiated (OAI).

The issues are linked to the use of inferior excipients in valsartan. Jubilant had to recall over 46,000 bottles of Valsartan tablets manufactured by at its Roorkee plant on the ground of using incorrect/undeclared excipient.

According to IDBI, this could hinder the generic business of the company.

"We have built a 17.6 percent fall in finished dosages business in FY20 but a growth of 5 percent in FY21, assuming the resolution would be reached in 12-18 months, supplies of existing products are not materially disturbed in the US, and non-US business continues to see growth," said IDBI.

"We have also built a 22.6 percent downside in revenues from API business (high base in FY19 on limited period opportunity from valsartan) in FY20 but 5 percent growth in FY21," the brokerage added.

Brokerage callsIDBI Capital: Buy (Initiated coverage) | Target price: Rs 620 | Upside: 23 percent

ICICI DIrect: Buy | Target Price: Rs 710 | Upside: 40 percent

HDFC Securities: Buy | Target Price: Rs 1,005 | Upside: 99 percent

JM Financial: Buy | Target Price: Rs 698 | Upside: 38 percent

Dolat Capital: Buy | Target Price: Rs 750 | Upside: 48 percent

Disclaimer: The views and investment tips expressed by brokerages on moneycontrol.com are their own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.