The market staged a smart but gradual comeback after hitting the lows of 2018, thanks to hopes of an earnings growth in FY19 and easing of US-China trade war tensions.

Also, normal monsoon forecast by two Skymet and India Meteorological Department has boosted sentiment and brightened outlook for the consumption space, which is expected to be the top theme on analysts' radar.

Some analysts expect a rate cut from the Reserve Bank of India rather than status quo or rate hike post the normal monsoon forecast.

Geopolitical tensions that lifted Brent crude to a near four-year high has been taken by the market in its stride. In fact, some experts feel a rise in Brent crude prices till USD 80 a barrel is not worrisome for India, which imports over 80 percent of its oil requirement.

The Nifty has rallied more than five percent from the lowest point of 2018, which it hit last month, after falling as much as 10 percent from record levels touched in January end.

A gradual recovery is largely possible from hereon, if the Q4 earnings season meets expectations and companies deliver a strong growth in FY19 as has been forecasted by every analysts on the Street. A positive outcome in state elections for the Bharatiya Janata Party going forward could add fuel to the rally, though there could be some volatility due to geopolitical tensions or any other global event, experts said.

S Ranganathan, Head of Research at LKP Securities, said corporate earnings season which kicked in last week and monsoons would decide the medium-term outlook for markets in a year which has several state elections lined up starting next month.

Rakesh Tarway, Research Head, Reliance Securities is much more positive. He sees a gain of 10-12 percent for the Nifty in FY19 as earnings growth is expected to be better with higher certainty and liquidity flow remains supportive. “However, geopolitical tensions leading to higher oil prices, assembly elections in FY19 in several states, slow pace of GST collections, et al, can be major constraints in FY19.”

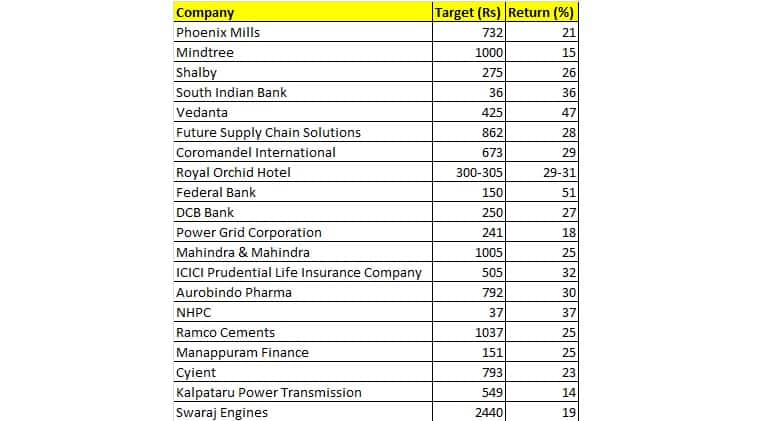

Here is the list of 20 stocks that could give up to 50 percent return over a period of one year:-

Brokerage: Motilal Oswal

Phoenix Mills: Buy | Target - Rs 732 | Return - 21%

We see huge growth opportunity in India’s retail industry, which is expected to reach a size of USD 2 trillion by 2020, growing at a CAGR of 12 percent. We believe that Phoenix Mills is a unique way to play India’s retail growth story.

Moreover, clarifications and issues surrounding REITs are now behind, and we expect India to attract strong inflows, where Phoenix Mills can become a great choice.

We prefer Phoenix Mills due to its a) strong operational performance (which provides a competitive edge), b) scalability (through the CPPIB deal), and c) robust cash generation (leading to a reduction in gearing and providing opportunities to acquire new malls).

The stock trades at a PE of 29x/23x FY19/20E, P/BV of 2.6x/2.3x FY19/20E and EV/EBITDA of 13.7x/11.4x respectively.

We value retail assets based on NAV approach, assuming a cap rate of 8 percent and a discount rate of 13 percent. We initiate coverage on Phoenix Mills with a Buy rating and an SOTP-based target price of Rs 732 (upside 21 percent).

Mindtree: Buy | Target - Rs 1,000 | Return - 15%

With business momentum back on track, we expect a CAGR of 14 percent in USD revenue and 29 percent in earnings over FY18-20. This brings Mindtree (MTCL) in the league of well-performing tier-II IT peers like LTI, MPHL and HEXW (their average multiples discount FY20E earnings by 18x). Pegging MTCL's multiple at the same level, we upgrade target price to Rs 1,000 (15 percent upside). Maintain Buy.

In FY18, MTCL's revenue grew by 8.6 percent YoY to USD 847 million, EBITDA by 3.1 percent YoY to Rs 7,400 crore and PAT by 29 percent YoY to Rs 570.1 crore. Excluding the one-offs from the reversal of acquisition liabilities, PAT grew 19.6 percent YoY to Rs 500.7 crore.

However, the exit to the year was far healthier on the operational front, with USD revenue up 15.6 percent YoY to USD 226 million, EBITDA up 26 percent YoY and PAT up 87 percent YoY to Rs 182.2 crore. QoQ revenue grew 5.5 percent versus our estimate of 4.3 percent. EBITDA margin expanded 100bp QoQ to 16.1 percent, largely in line with our estimate of 15.9 percent.

Our FY19/20 earnings estimates are up 4.4/10.5 percent, despite lower other income and a higher tax rate, for two reasons - strong revenue momentum and levers to cost are in place as well.

Brokerage: Elara Capital

Shalby: Buy | Target - Rs 275 | Return - 26%

We initiate coverage of Shalby with a Buy rating and a target price of Rs 275 on 20x FY20E EV/EBITDA. The company has one of the most scalable healthcare models in India, with focus on the orthopedics segment, which draws around 60 percent of revenue as on 9MFY18.

Steady growth across its two flagship hospitals along with scalability in new hospitals should result in a 27 percent overall sales CAGR and a 25 percent EBITDA CAGR over FY18-20E.

Moreover, zero net debt largely aided by Shalby’s recent IPO would further add to growth. It is currently trading at 15.7x FY20E EV/EBITDA, which is trading at a compelling valuation.

Brokerage: Ventura

South Indian Bank: Buy | Target - Rs 36 | Return - 36%

We re-initiate the coverage on South Indian Bank with a Buy recommendation and a price objective of Rs 36 (target Adjusted P/BV multiple of 1.2x FY20) implying a potential upside of around 36 percent

With most of the provisioning of the stressed assets behind us and South Indian Bank (SIB) focusing on aggressively growing its retail book, we expect the growth story to start unfolding.

We expect the loan book to grow at a 16 percent CAGR to Rs 72,810 crore by FY20, driven by a 21 percent CAGR in the retail book.

Further we expect NPAs to normalize to historical levels and, as a result, earnings are expected to grow at 28.6 percent CAGR to Rs 834.4 crore over the same period.

With the board already having given approval for fund raising through equity placement (20 crore shares) to qualified institutional buyers (QIB), capital adequacy will not be a constraint and should help sustain growth momentum over the forecast period FY17-20.

Brokerage: Edelweiss Securities

Vedanta: Buy | Target - Rs 425 | Return - 47%

We view Vedanta's (VEDL) acquisition of Electrosteel Steels (ELSS) as value accretive in the near term as: i) enterprice value per tonne of USD 546 is significantly lower compared to recent transactions; ii) EBITDA per tonne accretion potential via captive iron ore use & capacity ramp up; and iii) opportunity to expand beyond 2.51mtpa.

Assuming EBITDA per tonne of Rs 6,500-7,000 post capacity ramp up and iron ore self sufficiency, we envisage returns for VEDL's shareholders to be between 20 percent and 25 percent.

We see additional benefits of economies of scale if VEDL decides to expand the plant further as it has sufficient iron ore capacity in Jharkhand to support a 5mtpa plant.

We maintain 'Buy/SO' with target price of Rs 425 on FY20E EBITDA.

Future Supply Chain Solutions: Buy | Target - Rs 862 | Return - 28%

We anticipate a demand boom for third party logistics (3PL) services as manufacturers sharpen focus on core competencies and outsource complex supply chain needs.

Future Supply Chain Solutions (FSC) is geared to capitalise on this led by: i) customer stickiness due to focus on contract logistics business (70 percent of revenue); ii) fast expanding anchor client—Future Group; iii) diverse clientele in rapidly-growing consumer-facing businesses; and iv) moderate competitive intensity—given huge growth pie, we expect 3PL players to emerge as segment specialists.

Hence, we estimate FSC to clock 36 percent CAGR in both revenue and PAT over FY18-20 (almost 2x industry) with strong return on equity (RoE) and return on capital employed (RoCE) of 21 percent and 36 percent, respectively, in FY20.

Moreover, an asset-light model ensures strong free cash flow—surplus cash at 26 percent of net worth in FY20.

We initiate with Buy and target price of Rs 862, given its almost 2x industry growth, healthy RoE and cash generation.

Coromandel International: Buy | Target - Rs 673 | Return - 29%

We recently interacted with the newly appointed CFO of Coromandel International (Coromandel) Jayashree Satagopalan. She stated that the company has benefited from: i) robust fertiliser volumes; ii) uptick in fertiliser margins driven by improved industry dynamics & favourable product mix change; and iii) strong profitability in agrochemicals riding firm Mancozeb prices.

Driven by these positives, we estimate 61 percent PAT growth and around 700bps improvement in return on capital employed to 25 percent in FY18.

We maintain our positive stance on the stock given its pole position in complex fertilisers and expanding portfolio of non-fertiliser business. However, we expect earnings growth to moderate in FY19 to 9 percent on limited margin improvement due to raw material pressures.

We believe, Coromandel is a proxy play on domestic agri due to its leadership position in complex fertilisers and expanding agrochemicals portfolio & retail network. We expect it to continue to enjoy rich valuations and we value the stock at 20x FY20E EPS leading to target price of Rs 673.

We maintain Buy. While direct tax benefit will continue to be key near-term catalyst, volatility in fertiliser input (phos acid) & Manacozeb prices could adversely affect our estimates.

Brokerage: ICICI Securities

Royal Orchid Hotel: Buy | Target - Rs 300-305 | Return - 29-31%

The hotel industry occupancy has reached an inflection point that may trigger a sharp rise in ARR and EBITDA margin in FY19E. Further, the company expects to clock EBITDA of around Rs 50 crore on a consolidated basis in FY19E. Based on this, the stock is available at EV/EBITDA of 14x (vs. industry average of 25x).

Hence, we note that despite the recent run up, the company is still available at attractive valuations. On an enterprise value per room basis, the stock is trading at Rs 1.7 crore/room (below industry average of Rs 2.5-3.0 crore/room). Given this, we arrive at a target price of Rs 300-305/share (i.e. EV/adjusted room of Rs 2.2 crore/room).

Royal Orchid Hotel's (ROHL) ability to rapidly scale up through management contracts augurs well in improving demand dynamics. Further, comfortable debt levels and favourable tax rate are key positives.

ROHL's five star property at Bengaluru (195 rooms) is worth over Rs 600 crore versus current enterprise value of Rs 703 crore.

In the pre-GST regime, the company used to pay 21.3 percent. However, the same has come down to 18 percent under GST. We believe this will enable ROHL to effectively compete against unorganised segment.

Brokerage: Reliance Securities

Federal Bank: Buy | Target - Rs 150 | Return - 51%

Federal Bank is expected to deliver further improvement in operational performance led by improving loan book growth and improving assets liability mix. Advances grew by 5.3 percent QoQ to Rs 85,000 crore in Q3FY18, as SME, wholesale and retail (including agri) book grew by 13.3 percent, 4.4 percent and 6.85 percent QoQ respectively.

Further, continued moderation in SMA-2 balance clearly suggests fresh slippage will show declining trend in FY19. Notably, the bank is gradually coming out of the scenario marked with higher provisioning and continued stress on asset quality for last few quarters. Management expects credit cost to remain in comfortable level of 60-70bps in FY19.

Looking ahead, we expect the strong traction in earnings to continue owing to robust growth in loan book, moderate credit cost and healthy margins.

We expect the bank’s earnings to witness 33% CAGR through FY17-20E and reiterate our Buy recommendation on the stock with an target price of Rs150 based on 2.3x FY19E adjusted book value.

Brokerage: JM Financial

DCB Bank: Buy | Target - Rs 250 | Return - 27%

DCB Bank (DCBB) reported a strong growth quarter (+28 percent YoY loan growth) with softening opex (cost-to-income ratio down around 300bps QoQ) as the bank completed its planned branch expansion.

Adjusting for portfolio buyouts in FY17, organic loan growth was more than 30 percent in FY18. Margins were aided by improved yields and remained stable despite tighter liquidity conditions affecting cost of funds (+10bps QoQ).

Even as slippages declined sequentially, PCR was ramped up to 60 percent (+580bps QoQ) and adequately covers the stress on books.

Going ahead, we expect lower branch additions and controlled credit costs to offset downward pressure on margins.

As we roll forward to FY20E, we raise target price to Rs 250 per share valuing DCBB at 2.3x FY20E fully adjusted BVPS. Maintain Buy.

Brokerage: SMC Global Securities

Power Grid Corporation: Buy | Target - Rs 241| Return - 18%

Power Grid is a state-run electric power transmission utility company. Now, with the improvement in the capitalisation-to-capex ratio, steady regulated Return on Equity (ROE), SMC Global Securities is of the view that Power Grid fundamentals would continue to remain strong.

IT is also on track to achieve huge capex plan going forward as total work in hand is Rs1.2 lakh crore, including on-going projects, new projects, and Tariff Based Competitive Bidding projects worth Rs 1.02 lakh crore.

Mahindra & Mahindra: Buy | Target - Rs 1,005 | Return - 25%

Mahindra & Mahindra Ltd (M&M), through its subsidiaries, engage in the manufacture, distribution, and sale of passenger cars, tractors, multi-utility vehicles, light commercial vehicles, and three wheelers.

Company’s volume growth is on an uptrend led by strong demand in the tractor and a cyclical recovery in light commercial vehicles. A pick up in the rural economy is likely and should benefit M&M. It is expected that the company would see strong growth going forward. The price target of Rs1005 is based on one-year average P/E of 25.56x and FY19 (E) earnings of Rs39.31.

ICICI Prudential Life Insurance Company: Buy | Target - Rs 505 | Return - 32%

ICICI Prudential is the largest private sector life insurer in India. It is a joint venture between ICICI Bank and Prudential Corporation Holdings, a part of Prudential Group. According to the management, the company is focusing on improving protection business, persistence, and costs which would help ICICI Pru to get good growth in coming years.

The company expects strong growth opportunities for the life insurance sector and expects it to grow in-line with the nominal GDP growth.

Aurobindo Pharma: Buy | Target - Rs 792| Return - 30%

Aurobindo Pharma manufactures generic pharmaceuticals and active pharmaceuticals ingredients. The company continues to invest in enhancing specialty and complex generic pipeline for a sustainable growth. A diversified portfolio with limited product concentration risk is expected to help the company deal with price erosion challenges in the US.

All the key market continues to do well and has shown a healthy growth trend. It is expected that the stock will see a target price of Rs792 in 8-10 months timeframe on a one-year average P/E of 16.77x and FY19 (E) earnings of Rs47.20.

NHPC: Buy | Target - Rs 37| Return - 37%

NHPC is India’s premier hydrocarbon company, with 15 percent share of the installed hydro-electric capacity in India. The company has taken some effective steps for its capacity additions to meet the annual demand for power and growth.

It has developed new technologies in the areas of Electrical and Civil Engineering for improvement in planning and investigation which will reduce the delays in construction and problems situation.

The Ramco Cements: Buy | Target - Rs 1,037 | Return - 25%

The Ramco Cements Ltd, formely known as Madras Cements manufactures cement, ready-mix concrete and dry mortar products. The company has a strong balance sheet, low debt, and optimize operating capacity and management focus is to increase market share which would give a strong growth in the company.

Moreover, govt policies are expected to give a big push to the development of roads, highways, flyovers and bridges, Railway Projects, development of smart cities etc.

Manappuram Finance: Buy | Target - Rs 151 | Return - 25%

Manappuram is the only leading gold loan non-banking finance company. The consolidated asset under management (AUM) has increased 7 percent on a QoQ basis to Rs14650 crore for the quarter ended December 2017.

The company is witnessing a healthy growth across all business segments. Diversification efforts paid off as growth in the overall business is well supported by the robust growth witnessed in the new business.

Cyient: Buy | Target - Rs 793 | Return - 23%

Cyient Limited, formerly Infotech Enterprises Limited, is engaged in providing software-enabled engineering and geographic information system (GIS) services. The company is optimistic about the future and would continue to invest in digitization, including IoT, digital manufacturing, engineering analytics and mobility.

Kalpataru Power Transmission: Buy | Target - Rs 549| Return - 14%

Kalpataru Power Transmission is primarily engaged in the business of Engineering, Procurement and Construction (EPC) relating to infrastructure comprising power transmission and distribution etc.

The company continues to focus on improving profitability, order visibility and return ratios as a result of improved margins and unlocking of capital from non-core assets. Its diversification focus has led to success in securing significant orders in the non-T&D business with healthy margins.

Swaraj Engines: Buy | Target - Rs 2,440 | Return - 19%

Swaraj Engines is engaged in manufacturing engines for fitment in to Swaraj Tractors which is manufactured by M&M at its Swaraj Division. The management of the company expects good growth for demand of domestic tractor due to government's continued thrust ion agri and rural sector, which would help the company to increase market share and financial growth of the company.

The central government has time and again reiterated its aim to double farm income by 2022 which has envisaged to be attained through better productivity and enhanced farm realisations. Swaraj is a leading supplier of engines for the tractors to market leader M&M. The company is one of the key players to benefit from this transition.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.