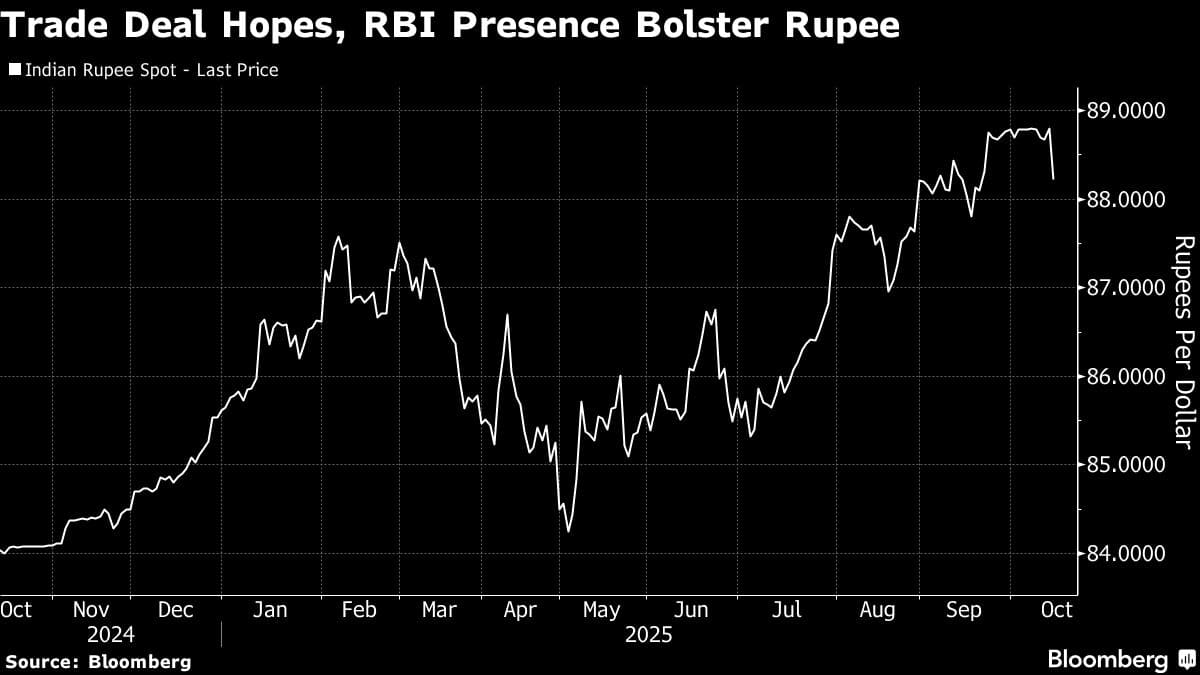

The Indian rupee gained the most in nearly four months, rebounding from near a record low as traders pointed to heavy support from the central bank — a move that brought back memories of a similar intervention in February.

The Reserve Bank of India likely sold dollars both in the offshore and onshore trades on Wednesday, according to people familiar with the matter who asked not to be identified discussing private matters.

The rupee, which had flirted with record lows a day earlier, staged its biggest intraday jump since June 24. The currency rose as much as 0.9% to 87.9987 per dollar before paring some gains, after having weakened to 88.8025 on Tuesday.

“Clearly, the RBI thinks the rupee has underperformed enough and depreciated enough, and from here on the behavior should be neutral with respect to regional FX,” said Abhishek Upadhyay, an economist at ICICI Securities Primary Dealership. “There has been a broad shift in framework.”

The heavy intervention echoed a move in February, when the central bank sold billions of dollars, catching speculators betting against the rupee off-guard. The currency has largely flatlined over the past three weeks, with traders suggesting the central bank has been quietly acting to prevent it from sliding past the 89 to a dollar level. Adding to the currency’s tailwinds, optimism about India fast-tracking trade talks with the US buoyed sentiment.

“The RBI likely sold big amounts in the spot and offshore markets leading to sharp gains in the rupee,” said Anil Kumar Bhansali, head of treasury at Finrex Treasury Advisors. “The hope of a trade deal soon is also helping.”

People familiar with the matter said Tuesday that New Delhi aims to wrap up trade negotiations by next month — a prospect that, coupled with a softer dollar on bets of US Federal Reserve rate cuts, gave the rupee an extra boost alongside other Asian peers.

The RBI didn’t respond to an email and a phone call seeking comment.

The central bank’s recent interventions at the 88.80 level also suggest that in the near-term the RBI doesn’t want rupee to weaken “too much too fast,” said Michael Wan, senior currency analyst at MUFG Bank.

“The combination of some hopes of a trade deal, continued pushback by the RBI and also the broader weaker dollar environment have helped,” said Wan. If the rupee gains past the 88.10 per dollar mark sustainably, it could head toward the 87 mark, he said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.