Planning a career change? Why not pull out savings piled up in your employees’ provident fund (EPF) account? Withdrawing EPF is a relatively simple process of filling out one form with your personal details and handing it to your human resources colleague to execute. After a few weeks, you’ll receive a cheque or the money is credited into your account.

Varsha Ojha, a senior executive with a media house, did exactly this. She changed 6 jobs in 8 years, between 2002 and 2010, and at the end of each she chose to withdraw the accumulated EPF amount. “Back then, it was the only obvious choice. I wasn’t much aware of the transfer process and liked to be planned rather than have money in many places.”

EPF rules prohibit withdrawals during your employment years, barring a few emergencies. However, some do exploit certain exemptions and relaxations allowed. For instance, you can withdraw up to 75 percent of your account balance after being unemployed for a month. If you have been unemployed for over two months, you can make a complete withdrawal. These could be tempting propositions for those pursuing their entrepreneurial aspirations or on sabbaticals.

Withdrawing and utilising the money the way you want does look logical. Also, for those with low take-home salaries, a lumpsum withdrawal sort of looks like a compensation. Or maybe, like Ojha, it is about having control and planning your next moves rather than just leaving the money in.

However, a better way to make more money is to simply not touch your EPF corpus; transfer it to your next organisation when you make that jump and let it grow. There’s a pretty good reason for this.

Also read | The Moneycontrol EPF guide

Compounding: The 8th wonder of the worldYou might need some extra cash for a medical emergency or some unavoidable expense. But you also miss out on higher returns by withdrawing from EPF too early.

Here’s how EPF works: 12 percent of your basic salary goes into your EPF account. Your employer then matches that with another 12 percent contribution. (8.33 percent to the Employees’ Pension Scheme and 3.67 percent to EPF). All this is towards building a corpus for when you retire. Contributions can be made till any age, as long as you are working for a contributing organisation.

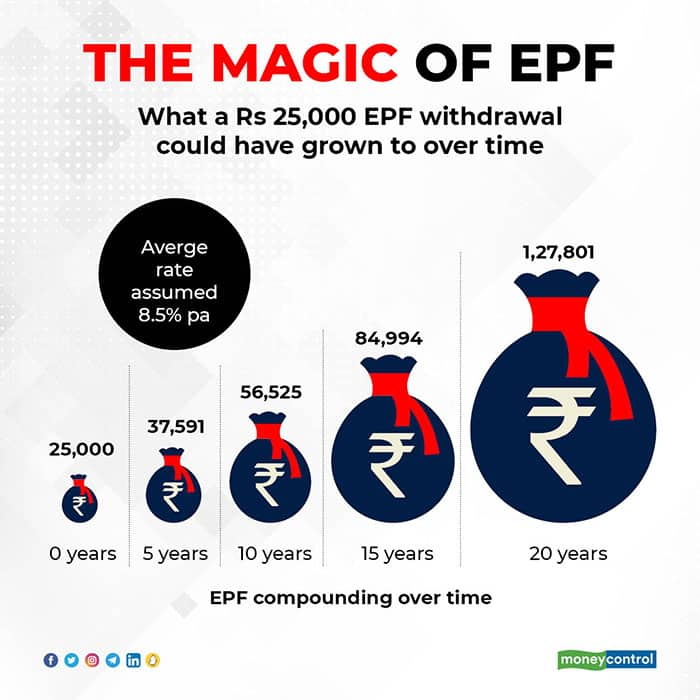

Let’s say the EPF amount accumulated at the end of your first year at your first job was around Rs 25,000. Now you decide to change jobs and Rs 25,000 may not seem like a big enough corpus to bother with a transfer and you simply withdraw it.

You may think that once you receive the cash, you will be in a better position to decide how to invest it, rather than leaving it with the EPFO. Often, withdrawal can be an easy choice, but when the lumpsum comes it may give the false impression of being a bonus to be spent. Ojha, admitted to spending most of her initial withdrawals, she eventually began investing partially from the later ones.

Assuming an average EPF rate of 8.5 percent, that Rs 25,000 would have more than doubled in 10 years, reached a value of Rs 85,000 in 15 years and been more than 5 times the value at Rs 1.28 lakh had it been transferred instead of being withdrawn.

Imagine that you start with Rs 1 lakh (instead of Rs 25,000). After 20 years, you end up with Rs 5 lakh. Add up many such withdrawals and the impact on your future financial security can be substantial. Each time you withdraw, you take away what got added and saved. In seeking immediate access, you can lose out on the benefit of compounding.

According to Deepali Sen, founder Srujan Financial Services LLP, “Some of my clients do withdraw if they are retiring or taking a sabbatical, but most transfer at the time of a job change. Those who withdraw, it’s with the understanding that 90-95% of the corpus will get reinvested according to their requirements.”

Also read | Does the EPF rate cut make voluntary provident fund unattractive?

Withdrawing your EPF balance without an action plan in place can potentially mean it gets spent. If you must withdraw, ensure you are able to put that corpus back to work.

Ojha has now been in the same organisation for over 11 years. As a result, she cannot, due to the stringent EPF rules, withdraw her EPF corpus. The good news is that she can now at least see the impact of compounding on the corpus accumulated over this period. In hindsight, with better awareness, she admits, she would have made a different choice.

“In case of a simple job change, where EPF can be transferred, the choice is always to do that. Even in cases where an individual is entering into an entrepreneurial journey from being an employee, the preference is to not withdraw immediately. You can keep the money in for 36 months with interest being paid on the corpus; it is prudent to leave it in, while you decide the course of things in the next phases” says Vivek Rege, Founder and CEO, VR Wealth Advisors Pvt Ltd.

Let’s assume that the Rs 25,000 EPF amount from your first year at work increases by 10 percent for the next 10 years. But, each time you change jobs you withdraw that amount and spend it. What you can lose out on is potentially Rs 4 lakh worth of contributions, which, if you stayed invested with EPFO, could translate to a corpus 5 times higher in value over 20 years.

What should EPF subscribers do?It’s not just the accumulated savings, rather the long-term compounding at a relatively higher rate of interest that helps in making the sum of those annual contributions a substantial part of one’s overall long-term debt portfolio. Rege added, “Withdrawing EPF before time will also mean you are taking safety capital and re-investing it in market-linked securities, or adding some risk. Keep in mind, once withdrawn, the accumulated corpus cannot be invested back into EPF.”

With a universal account number (UAN) for EPF accounts, investments in equity assets, no age limit for contributions and SMS updates on contributions and corpus, EPF has become an investment at par with other financial investments and one where you cannot ignore the benefit of long-term holding and compounding.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.