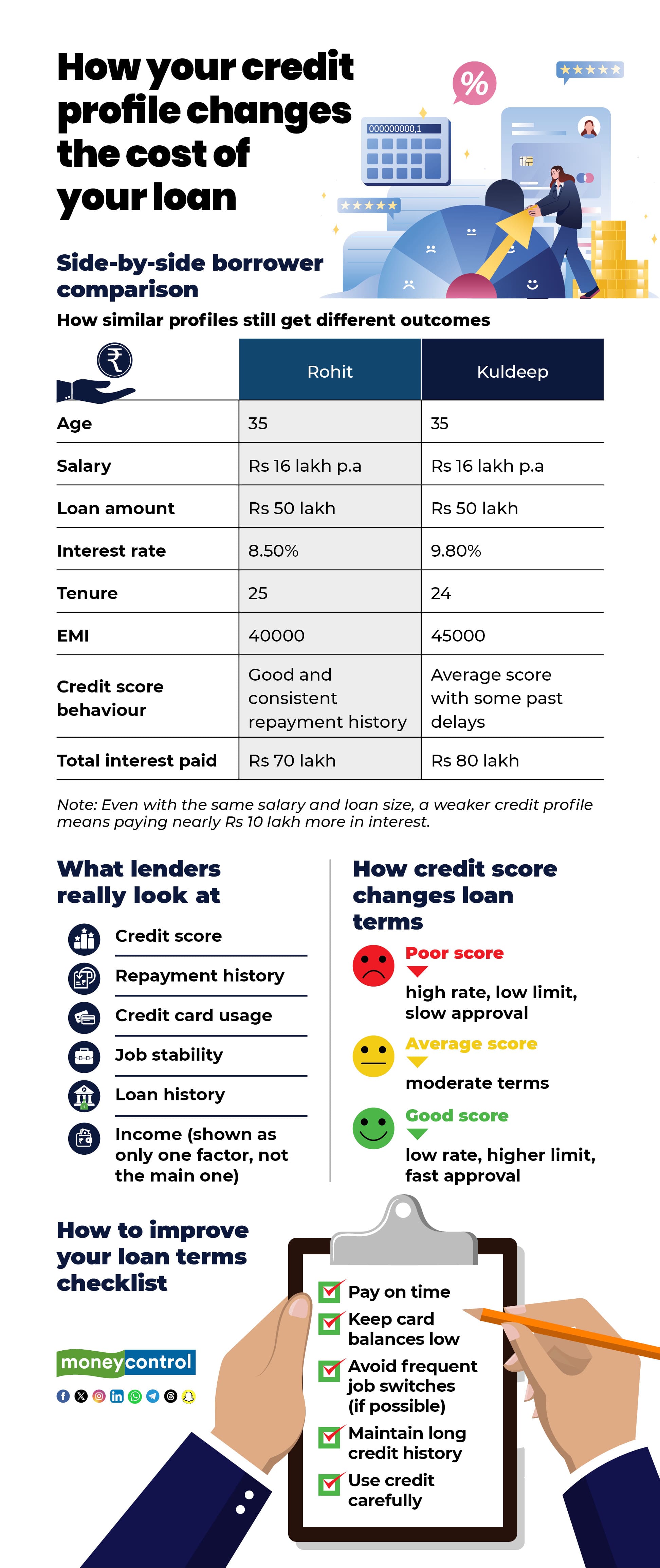

At first glance, Rohit Yadav and Kuldeep Sharma had identical borrower profiles. Both were 35, earned Rs 16 lakh a year, and applied for a Rs 50-lakh home loan from the same bank in the same month.

But the offers they received couldn't have been more different.

Yadav was offered an interest rate of 8.5 percent with a 25-year repayment period. The same bank quoted 9.8 percent rate to Sharma with a repayment period of 24 years, which meant he would have to pay more.

The reason had little to do with salary.

"Two borrowers with similar incomes can face very different outcomes if one has a history of timely payments and prudent credit use while the other has frequent delays or higher credit utilisation. In a market where access to credit is essential for attaining goals and growth, the ability to interpret and improve an individual’s credit score is not just helpful but transformative," said Anand Agrawal, Co-founder & CPTO, Credgenics.

When lenders prioritise credit behaviour, borrowers gain a clearer picture of what actually matters. How consistently you meet obligations, how responsibly you use available credit and how promptly you address delinquencies or incorrect entries with bureaus. For many, the path to better credit starts with understanding the specifics behind the score and the factors influencing it, the accuracy of reported data, and the practical actions that move the needle.

"For borrowers, the practical starting point is to understand what’s pulling their credit score down, such as missed dues, high utilisation, excessive enquiries, or reporting errors and then work systematically to correct and rebuild their score. That’s where credit-health support and advisory tools can help people translate bureau data into clear actions," said Agrawal.

There are many platforms that assist individuals in understanding their credit reports, spotting discrepancies, and adopting credit behavioural habits that steadily improve outcomes

BankBazaar.com CEO Adhil Shetty explained the reason. "RBI data shows retail credit growing at over 15 percent CAGR in recent years, driven by algorithm-led underwriting where repayment history, credit utilisation and account vintage often matter more than stated income. This explains why borrowers with similar salaries can receive very different loan terms," he said.

"A strong credit profile can lower interest rates by 300 to 600 basis points, improve approval timelines and unlock higher limits. As lending becomes more behaviour-led, with credit activity tracked across cards, BNPL and digital loans, maintaining discipline is no longer optional. It directly shapes long-term financial mobility."

Yadav maintained a good credit score, with no missed payments. He cleared an earlier car loan on time and used his credit card carefully. Sharma had two delayed payments on record from three years earlier and carried a higher credit card balance, which he didn't clear on time.

While the debt level created a gap, their job profiles also mattered. Yadav worked at an IT firm for nine years straight. Sharma, a journalist, changed jobs four times in 10 years.

While an individual's income indicates their potential to earn, a credit score indicates the individual's behaviour with money by way of how regularly the individual has handled their financial commitments over time.

Loan provider Olyv CPO Vinay Singh said , "Borrowers with good credit scores will typically access better loan options such as improved interest rates, larger credit limits, faster approvals and more attractive financial products. In contrast, borrowers with poor credit scores may face significantly higher rates when borrowing or may get denied loans altogether, even though the borrower may have a stable or rising income."

"With increasing dependence on data-centric underwriting by lenders, behaviours relative to repayment of debt, the way in which the borrower utilises their credit and other behavioural characteristics related to keeping their accounts in good standing are becoming more heavily monitored."

This is significant because it underscores the need to treat credit as a long-term financial asset rather than a short-term convenience. Regular repayments, using only as much of their credit as needed and maintaining a favourable ratio of available credit to actual credit used helps provide the consumer with more financial flexibility.

Managing credit profile is no longer an option but a must to secure good deals when borrowing from lenders.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.