Amidst the focus on COVID-19 and the related costs and insurance premiums, it’s important to ensure that we are covered for other diseases too. Usually, our base health insurance policy is enough when it comes with a decent sum assured amount.

But did you know how much the treatment for critical and chronic illnesses such as cancer, cardiac ailments, renal failure and liver transplant can cost you? It’s not just hospitalisation costs. For example, myocardial infraction claims could cost you anywhere between Rs 6 lakh and 7.5 lakh, while a stroke could leave a family poorer by Rs 10 lakh, as per claims data released by Bajaj Allianz General Insurance. A kidney failure could set you back by Rs 8.5-10 lakh, besides regular dialysis that could stretch for years. The post-hospitalisation care is expensive too. And if this leads to a job loss, because you might need time to recover, it results in a loss of income.

Also read: Super top-up: A cost-effective way to bolster your health insurance cover

This is why you must buy a critical illnesses policy, over and above your base (normal) health insurance cover.

I have my basic health insurance cover. Do I still need a critical illness policy?

Yes, you do. A simple health insurance policy pays for your actual hospitalisation bills. It either settles the bill directly with your hospital through the cashless route or reimburses you after you submit your bills.

But what happens if your illness entails a longer recovery period or is chronic? Or, the treatment could be on-going, for which you need to take time off from work. Here’s where a critical illness policy helps. Such plans are typically benefit-based policies. That is, they pay you a pre-decided lump-sum amount once you are diagnosed with a critical illness listed in the policy, irrespective of the actual treatment expenses incurred. Such policies cover life-threatening illnesses such as cancer, stroke, renal failure, organ transplant and heart attacks.

Also listen: Simply Save podcast – Why it is important to buy an adequate health insurance cover

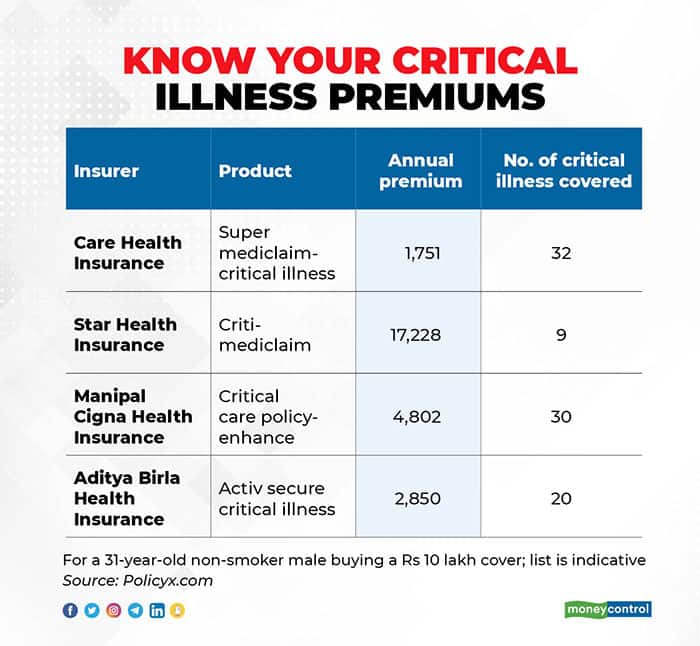

The policies, which are offered by both general and life insurers, cover a fixed number of critical illnesses, ranging from two to even 60. You can either buy them as standalone policies or as riders along with your life insurance plans.

“We have observed that critical illnesses such as cancer, kidney problems and cardiac conditions are affecting the younger generation in the age group of 30 to 40 years also and the incidence is on the rise. A critical illness policy is a must-have cover, specifically in the current situation of the pandemic. COVID-19 has further increased the risk for younger as well as people in older age groups,” says TA Ramalingam, Chief Technical Officer, Bajaj Allianz General Insurance.

How much critical illness cover should you buy?

Critical illness plans can complement your regular health policies. These will pay out the claim even after your regular policy has already settled the hospitalisation bills. You need not submit the original bills either – photocopies will suffice for claim payout under benefit-based critical illness policies.

If your basic health cover is Rs 5 lakh, you can look at buying a critical care policy of Rs 20-25 lakh. “You can use the claim amount for other expenses which are over and above hospitalisation expenses,” says Mayank Bathwal, CEO, Aditya Birla Health Insurance. For example, you might need prolonged physiotherapy sessions after, say, a stroke or modifications to lifestyle after an organ transplant. It will help you meet your recuperation expenses after surgery, chemotherapy or radiation – be they expensive medication, regular calcium or vitamin supplements, purchase of walking aids and so on. While regular policies do pay for follow-ups, diagnostic tests and pharmacy bills as part of post-hospitalisation cover, this coverage typically stops after 60-90 days.

Moreover, the lump-sum will also come in handy for those who may have had to let go of their jobs due to the illness and lengthy treatment process.

If I got COVID-19 earlier, will I get a critical illness policy?

If you have recently recovered from COVID-19, you could face some hurdles. “It is assumed that COVID survivors carry greater amount of risks to their lives. The waiting period for any insurance policy is extended from 1-3 months from the date an applicant turns COVID negative, and the tests required have increased too,” says Naval Goel, CEO, Policyx.com.

Also read | Covid-19 hospital bills: Your health insurance policy will not pay these charges

The underwriting approach – evaluating the applicant’s health risk, deciding whether the policy can be issued or not and determining premiums – will vary as per the insurer.

“The usual underwriting process is followed, wherein we request customers to share declarations of present health conditions and possibly undergo some health tests for medical underwriting due to any age or lifestyle-related health complication. A medical check-up in a COVID-19-related case will depend on the extent of the hospital treatment or severity of the infection,” explains Ramalingam.

Which critical illness policy should you buy?

All critical illness plans do not cover all serious illnesses.

Look at the terms of coverage. It is best to go with a plan that covers a broad range of ailments than one that covers just one or two dreaded diseases.

Keep an eye out for the fine-print. The insurer will pay the claim only if the policyholder survives for at least 30 days post-diagnosis. In case of some cancer-specific policies, only 25-50 per cent of the sum insured will be paid in the case of initial-stage cancer, for instance. Also, typically, critical illness policies cease to exist once the sum insured is paid out.

The last one year has underlined the importance of having adequate health insurance cover, and has also exposed the limitations of regular health policies. COVID-19 claimants have been receiving only half of the claimed amount, which means that they have had to pay the balance from their pockets despite having health covers in place.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.