For most investors, the conversation around investing begins and ends with returns.

But here’s an uncomfortable truth most investors discover late: You don’t control returns. You do control how much you invest.

Over long investment horizons, how much you invest and how regularly you increase that amount often matters more than chasing higher returns.

Surprised? Here is a simple SIP comparison that highlights this reality.

Two SIPs, One Starting Point

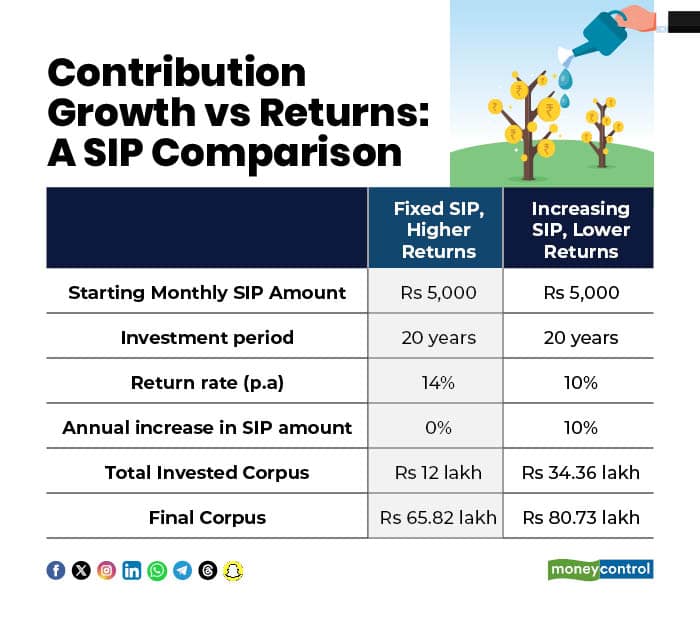

Consider two investors, both starting a systematic investment plan (SIP) of Rs 5,000 per month and staying invested for 20 years.

In the first case, the investor keeps the SIP amount constant throughout the period and earns an annual return of 14 percent.

In the second case, the investor earns a lower annual return of 10 percent but increases the SIP amount by 10 percent every year.

Now let’s look at what actually happens.

SIP Comparison

SIP Comparison

At first glance, the higher-return option appears superior. However, despite earning 4% lower returns, the second SIP ends up with a larger corpus that is nearly Rs 15 lakh higher.

That’s not a typo. This result often surprises investors, but it follows a straightforward principle: wealth creation depends as much on contribution growth as it does on investment returns.

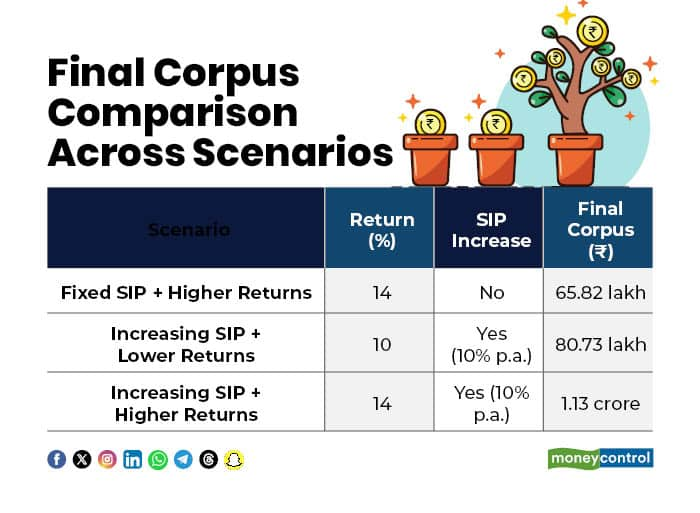

Now consider a third, and often ignored, scenario.

If the investor not only increased the SIP amount by 10 percent every year but also managed to earn a 14 percent annual return, the final outcome changes dramatically. Under this combination, higher contributions and higher returns, the accumulated corpus would rise to Rs 1.13 crore over the same 20-year period.

SIP scenarios

SIP scenarios

This highlights an important insight. While returns amplify wealth, contribution growth lays the foundation for it. Returns work best when they are applied to a steadily rising investment base.

‘Invested More’ Is the Point

At this point, the usual response that shows up is as the second corpus is larger the investment amount is higher. And that’s exactly the insight most people miss.

Returns are uncertain and largely outside an investor’s control. Markets fluctuate, cycles change, and even the best-performing funds struggle to stay on top consistently.

What investors can control is how much they save and invest. Increasing the SIP amount is a deliberate, repeatable action. Over long periods, this has a far more predictable impact on wealth than trying to extract marginally higher returns.

Why increasing your SIP works so well

There are several reasons why gradually increasing SIP contributions works so well in practice.

1. It aligns investing with real life

Your expenses don’t stay constant for 20 years, and neither does your income. Incremental SIP hikes mirror how careers actually progress.

2. It reduces pressure to ‘earn more returns’

When contribution growth does the heavy lifting, you don’t need unrealistic return assumptions to make your goals work.

3. It makes compounding smoother, not heroic

You’re not trying to double money magically. You’re feeding the system more fuel every year.

And a 10 percent annual increase sounds big on paper but in reality, it’s often just a few hundred rupees extra each month.

Shifting the Investment Mindset

The fixation on returns often distracts investors from more impactful decisions.

You need consistency, discipline, and a willingness to increase your investments as your capacity grows.

The Bottom Line

Long-term wealth creation is less about maximising returns and more about maximising participation.

Instead of asking how much your investments can earn, ask how much more you can invest.

A small, regular increase in your SIP may not feel dramatic, but over time, it can make the decisive difference between an adequate corpus and a meaningful one.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.