The National Pension System (NPS) is designed as a long-term retirement savings scheme. In most cases, subscribers are required to use a significant portion of their accumulated corpus to purchase an annuity upon exit. However, there are some situations in which subscribers can withdraw all of their NPS corpus. These rules are laid out by the Pension Fund Regulatory and Development Authority (PFRDA).

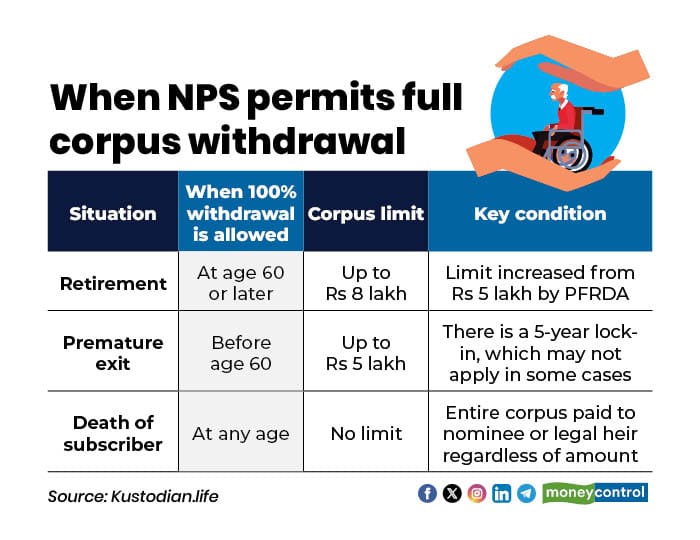

Kunal Kabra, Founder, Kustodian.life said, "NPS subscribers can withdraw their entire corpus only in specific situations prescribed by PFRDA. At retirement (age 60 or later), full withdrawal is permitted if the total NPS corpus does not exceed Rs 8 lakh, following PFRDA’s enhancement of the earlier Rs 5 lakh threshold."

In case of premature exit, before the age of 60, 100 percent withdrawal is allowed only if the subscriber has completed at least five years in NPS and the corpus is up to Rs 5 lakh, according to the revised exit norms. On the death of the subscriber, the entire corpus is payable to the nominee or legal heir, irrespective of the amount.

When NPS permits full corpus withdrawal

When NPS permits full corpus withdrawal

The first situation is retirement. When an NPS subscriber reaches the age of 60 or exits after that age, full withdrawal of the corpus is permitted only if the total accumulated amount does not exceed Rs 8 lakh.

However, if the corpus is more than Rs 8 lakh, the annuitisation requirements differ based on the subscriber category. “For non-government subscribers with a corpus exceeding Rs 12 lakh, at least 20 percent must be used to purchase an annuity, while up to 80 percent can be withdrawn as a lump sum (though only 60 percent is tax-exempt). For government employees with corpus above Rs 12 lakh, at least 40 percent must be used for annuity purchase while up to 60 percent can be withdrawn,” Kabra said.

Voluntary exit

The second case relates to premature (voluntary) exit, which refers to leaving the NPS before attaining the age of 60. According to Rule 4(1)(b) of the PFRDA Exit Regulations, a subscriber is eligible for voluntary premature exit only after completing a minimum of five years of subscription. A subscriber may withdraw the whole corpus only if the total amount does not exceed Rs 5 lakh. If the corpus exceeds Rs 5 lakh, at least 80 percent of the accumulated amount must be utilised for the purchase of an annuity, with only the remaining portion permitted to be withdrawn as a lump sum.

In case of a subscriber's death, the entire corpus is paid to the nominee or legal heir. There is no upper limit on the amount and there is no requirement to purchase an annuity. The nominee or legal heir may withdraw 100 percent of the accumulated corpus in a single payment.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.