The insurance regulator IRDAI has recently asked general insurance companies to strengthen awareness efforts around motor insurance, pointing out that over 50% of vehicles on Indian roads do not have insurance coverage.

While third-party motor insurance is mandatory under the Motor Vehicles Act, 1988, many vehicle owners tend to view it purely as a legal formality. In practice, however, it plays a clear role in handling the financial and legal liabilities that can arise from road accidents.

Why should you get third-party insurance?

Third-party motor insurance is the most basic and compulsory insurance cover required under the Motor Vehicles Act, 1988. It protects vehicle owners against legal and financial liabilities arising from injury, death, or property damage caused to a third party in an accident involving the insured vehicle.

The “third party” here refers to anyone other than the vehicle owner or driver, such as pedestrians, occupants of another car or two-wheeler, or passengers of another vehicle.

Niharika Singh, Executive Director, Marketing, IFFCO-TOKIO General Insurance says, “This policy does not cover damage to the insured vehicle itself. Its sole purpose is to compensate the affected third party”.

In practical terms, third-party insurance covers:

In the absence of third-party insurance, the vehicle owner becomes personally liable for compensation. These costs can run into several lakhs or even crores in serious cases. “Given India’s high accident rates, this cover plays a crucial role in ensuring that accident victims receive financial support, while shielding vehicle owners from crippling liabilities,” says Singh.

How third-party insurance helps at the time of an accident

At the time of an accident involving injury, death or damage to another person’s property, third-party insurance acts as a financial and legal shield for the vehicle owner.

Instead of handling compensation claims personally, the insurer steps in and manages the process as per legal provisions.

“In essence, third-party insurance ensures that an unfortunate accident does not turn into a long-term financial and legal crisis for the vehicle owner, while also ensuring justice and support for accident victims,” Singh says.

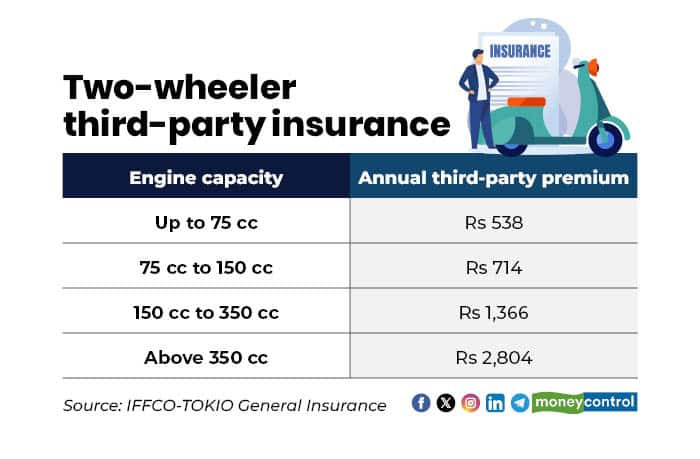

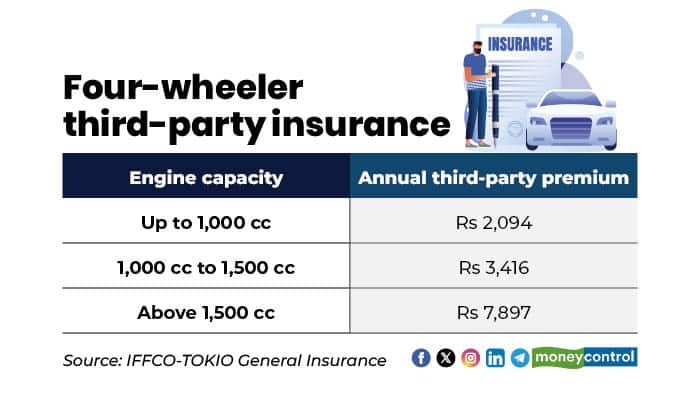

How much does third-party insurance cost?

One of the biggest misconceptions around motor insurance is cost. Third-party premiums are regulated and standardised. The premiums are fixed under the Motor Third Party Insurance Rules and are uniform across insurers for basic cover.

The annual premium of two-wheeler third-party insurance generally ranges between Rs 500 to Rs 3,000, whereas for four-wheeler private cars the annual premium ranges between Rs 2,000 to Rs 8,000.

“These premiums provide unlimited liability cover for third-party injury or death, as decided by courts. The contrast is stark: a few thousand rupees a year can protect against liabilities running into crores,” explains Singh.

What about long-term third-party policies?

For new vehicles, insurers also offer long-term third-party policies, which are typically three years for cars and five years for two-wheelers. These are often bundled with comprehensive cover at the time of purchase but can also be taken separately.

Singh adds, “These long-term covers provide regulatory compliance and cost stability over multiple years, often at a cumulative rate that is lower than renewing annual policies each year.”

Having said that, vehicle owners should still read the fine print to understand what is included and remember that third-party cover does not replace own-damage insurance.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.