For unit-linked insurance policyholders whose plans are set to mature soon, the Corona Virus (COVID-19)-driven market crash could not have come at a worse time. After waiting for a long period – 10-15 years – to create wealth for their long-term goals like retirement and children’s education, they have to face the prospect of a severe erosion in their maturity proceeds. Being market-linked products, ULIP funds’ net asset value (NAV) as on the date of maturity will determine your total corpus. But the COVID-19-induced market mayhem is likely to have left this fund value battered and bruised.

However, the Insurance Regulatory and Development Authority of India (IRDAI) has stepped in to offer some relief to such policyholders. It has asked life insurers to allow a staggered settlement option across all ULIPS – even for products that do not offer this facility – maturing up to May 31, 2020.

The rationaleThis option allows policyholders to get their maturity proceeds in instalments, over a period of up to five years.

“The rationale is that ULIP fund values would have seen depletion in the current volatile market conditions. So, if policyholders want to continue and wait for the markets to improve from present levels, they can opt for a partial settlement option on their ULIP payout,” says Anil PM, Head-Legal and Compliance, Bajaj Allianz Life Insurance.

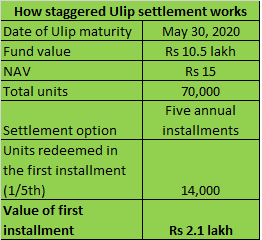

You can receive your maturity proceeds in monthly, quarterly, half-yearly or yearly instalments rather than at one go. For example, let’s say you opt to receive your maturity proceeds in five annual instalments. The value of your first instalment will be one-fifth of the number of units to your credit on the date of maturity multiplied by the NAV as on that date. Likewise, the second instalment will be one-fourth the remaining units multiplied by the NAV as on the second anniversary of maturity.

In 2013, the IRDAI had issued regulations permitting staggered payout of maturity proceeds over five instalments. Since it was an option, not all ULIPs have this feature currently. IRDAI’s latest move will ensure that the option is available across all ULIPs. Remember, however, that once you choose the staggered settlement option, you cannot make any further partial withdrawals or switch funds during the settlement period. If you feel the need for these funds in future, you will have to make a full withdrawal. In case of the policyholder’s death during the staggered payout period, the nominee will get the balance units at the NAV prevailing on the date of intimation of death.

Lump-sum or staggered payouts?If you decide to use this option, you should bear in mind that market-linked products such as ULIPs do not offer any guarantee. “If the markets recover later, you may get a higher NAV and hence a higher payout. But there's a risk associated with this too – if the markets go down further, then the policyholder will get a lower payout. However, given the extreme conditions currently, things must improve for the better from here on,” says Vivek Jain, Head, Investments, Policybazaar.com

Financial planners believe spread-out withdrawals are a better bet than lump-sum payouts at the moment and policyholders should make use of the option. “Instead of booking a huge loss and receiving your ULIP proceeds at a time when equity markets are reeling under the COVID-19 blow, you can defer the withdrawal,” says Suresh Sadagopan, Founder, Ladder7 Financial Services. You can consider following this strategy if you do not have an urgent need for the funds right now. On the other hand, if you are facing cashflow challenges, it is best to liquidate your investments, even if diminished in value, instead of taking loans, particularly unsecured debt such as personal loans or credit cards.

ULIPs vs Mutual fundsGiven that the BSE Sensex has shed over 26 per cent since the all-time high of 42,273 recorded on January 20, 2020, experts suggest that the valuations look attractive at the moment. It is time for retail investors to increase their exposure and stay invested for the longer haul. So, should you consider sticking to your original ULIP lump-sum payout option, and invest the proceeds in inexpensive direct equity mutual fund schemes?

Insurers can only levy a fund management charge (maximum of 1.35 per cent) during the settlement period. “Direct plans could be further cheaper with an expense ratio of around 1 per cent. But I believe this is too marginal a difference to go through the process of taking lump-sum ULIP proceeds, choosing the right mutual fund and reinvesting,” says Sadagopan. Once the maturity proceeds hit your savings account, you might find it difficult to redeploy them, given the increased need for liquidity these days. “In the process, you will lose out on the opportunity to let it grow,” he adds.

However, if you are convinced that you should get hold of ULIP proceeds and invest them in direct plans of equity mutual funds, you need to do your homework well. “You can consider taking this route if you are proficient in money management. But going direct isn’t as simple. In the past, retail investors have flocked to small and mid-cap schemes on the back of spurt in their returns, but have burnt their fingers when the tide turned,” says Amol Joshi, Founder, PlanRupee Investment Services. Choose this option only if you have the time and patience to analyse the schemes before investing, monitor their performance regularly and take a timely call on exiting if required.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.