Investing has become more accessible than ever, with options ranging from fixed deposits (FDs) and mutual funds to stocks and government schemes like the Public Provident Fund (PPF). However, navigating the world of personal finance requires some foundational principles to make informed decisions.

Here are six key investing rules that can help you grow your wealth, manage risks, and plan for the future.

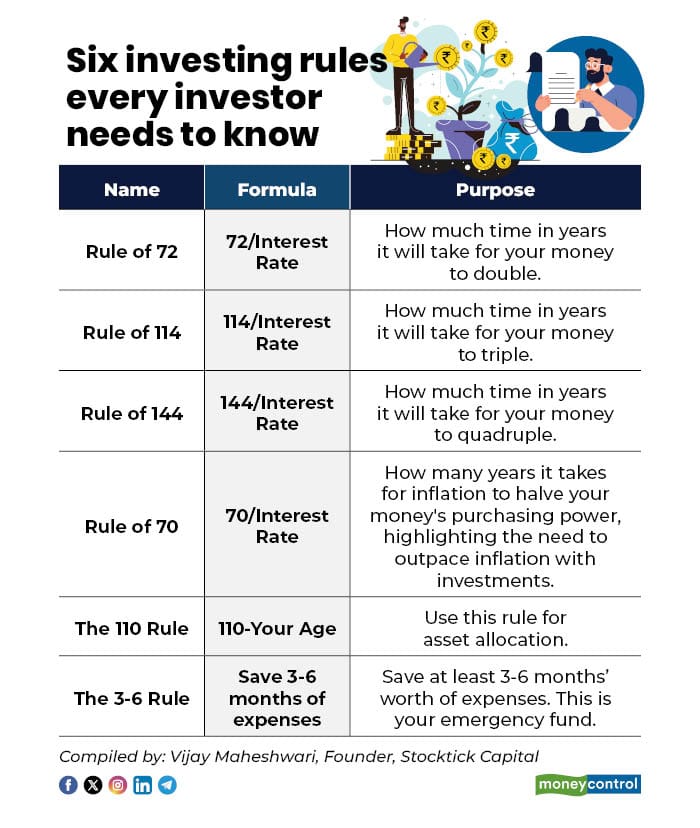

Rule of 72: Time to double your investment

Formula: 72 / Interest rate (or expected return rate)

Purpose: This rule estimates how many years it will take for your investment to double in value through compound interest, assuming the rate remains constant.

The Rule of 72 is a mental math tool to gauge the power of compounding. It's particularly useful for comparing investment options like FDs, mutual funds, or stocks.

Example: If you invest Rs 1 lakh in an IDFC First Bank FD at 7 percent interest per annum, it'll approximately double to Rs 2 lakh in about 10 years, using the Rule of 72 (72 / 7 = 10.3 years).

For a higher-return option, consider an equity mutual fund tracking the Nifty 50, which has historically delivered around 12 percent annualized returns. Here: 72 / 12 = 6 years. If a young professional invests Rs 5 lakh from her salary in such an equity fund, it could double to Rs 10 lakh in six years, helping build a corpus for goals like children’s education.

Rule of 114: Time to triple your investment

Formula: 114 / Interest rate (or expected return rate)

Purpose: Similar to the rule of 72, this calculates the years needed for your money to triple, aiding in long-term planning like retirement funds.

This rule builds on the doubling concept but for tripling, which is ideal for aggressive growth strategies.

Example: Using the same 7 percent FD rate: 114 / 7 = 16.3 years. If you invest in a corporate FD at this rate, it will grow to Rs 6 lakh in about 16 years.

For equities at 12 percent: 114 / 12 = 9.5 years. By investing Rs 3 lakh in diversified equity funds, you could see it triple to Rs 9 lakh in under 10 years.

Rule of 144: Time to quadruple your investment

Formula: 144 / Interest rate (or expected return rate)

Purpose: This estimates the time for your investment to grow fourfold, useful for ambitious goals like wealth multiplication over decades. It's an extension for even longer horizons.

Example: At 7 percent FD rate: 144 / 7 = 20.6 years. An investor investing Rs 50,000 could see it quadruple to Rs 2 lakh in about 21 years, providing a safety net for retirement amid rising healthcare costs.

At 12 percent equity returns: 144 / 12 = 12 years. By investing Rs 4 lakh through an SIP in mutual funds, this could grow to Rs 16 lakh in 12 years, helping fund a down payment on a flat in a market where average home loans are around Rs 50 lakh.

Also read | NPS Vatsalya Scheme update: PFRDA makes partial withdrawal, exit rules more attractive; check details

Rule of 70: Time taken for buying power to erode

Formula: 70 / inflation rate

Purpose: This rule approximates how many years it takes for inflation to halve your money's purchasing power, highlighting the need to outpace inflation with investments.

Inflation erodes value over time, so this rule reminds investors to aim for returns higher than inflation. India's inflation averages 4–6 percent, so let’s consider 5 percent for a realistic scenario.

Example: At 5 percent inflation: 70 / 5 = 14 years. If you have Rs 10 lakh in cash today, its buying power could halve to the equivalent of Rs 5 lakh in 14 years. To counter this, invest in inflation-beating assets like equities or gold.

The 110 Rule: Asset allocation guideline

Formula: 110 minus (less) Your age

Purpose: This suggests the percentage of your portfolio to allocate to equities (stocks or equity funds), with the rest in safer debt instruments like FDs or bonds. It's a rule for balancing risk and growth based on age.

This is a more aggressive version of the common "100 minus (less) age" rule, suitable for young demographic aiming for higher returns.

Example: For a 30-year-old IT professional: 110 - 30 = 80 percent. So, allocate 80 percent to direct equity or diversified equity mutual fund schemes and 20 percent to debt (like FDs or debt funds). If her portfolio is Rs 10 lakh, Rs 8 lakh in stocks could leverage India's booming market, while Rs 2 lakh in FDs provides stability amid job market volatility.

For a 50-year-old professional: 110 - 50 = 60 percent. With Rs 20 lakh saved, Rs 12 lakh in equities and Rs 8 lakh in debt helps preserve capital for retirement.

Also read | GIFT City explained: A new gateway to global stocks, mutual funds and insurance

The 3-6 Rule: Building an emergency fund

Formula: Save three to six months of expenses

Purpose: This creates a liquid safety net for unexpected events like job loss or medical emergencies, kept in easily accessible accounts like savings or liquid funds.

In an uncertain economy, with events like pandemics or layoffs in sectors like IT, this rule ensures financial resilience without dipping into investments.

Example: For a middle-class family of four in an urban city with monthly expenses of Rs 1 lakh (covering rent, groceries, education, and transport), aim for Rs 3–6 lakh in an emergency fund. Store it in a high-interest savings account (4–5 percent rates) or liquid mutual funds (6–7 percent returns).

Conclusion

These six rules provide a straightforward framework for investors to plan effectively.

Remember, they're approximations and don't account for long-term capital gains (LTCG) taxes, market volatility, or personal risk tolerance.

Start small, stay consistent, and leverage India's growth story for financial freedom. Applying these can turn your savings into substantial wealth.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.