14 February, 2025 | 11:00 IST

Access to personal loans and credit cards has significantly increased in recent years with the emergence of tech-driven digital lending platforms. With the availability of a wide range of credit facilities across categories to meet the needs of customers from all income groups, availing a loan or credit card is no longer difficult. While the consumption of credit products is rising, borrowers should assess their repayment capacity regularly to avoid any default situations. Most digital lending platforms finalise loan applications based on two important factors— credit score and the income of the borrower. A good credit score helps people get loans more easily with lower interest rates. With the rising awareness about credit instruments and financial products, it’s important to be careful to maintain a high credit score.

Table of Contents

According to a report by TransUnion CIBIL, the awareness about credit score has significantly increased among users with nearly 51% year-on-year growth in FY24. Notably, 81% of the consumers from non-metro cities starting monitoring their credit score within 6 months of getting their first credit product.

The report also reveals that users who monitor their score have an average credit score of 729 while those who don't have their average at 712. Moreover, 46% of those who self-monitored their scores improved their credit score in six months, compared to 41% of users who didn't.

Overall, the findings underscore the rising credit score awareness in India and its positive impact on financial behavior.

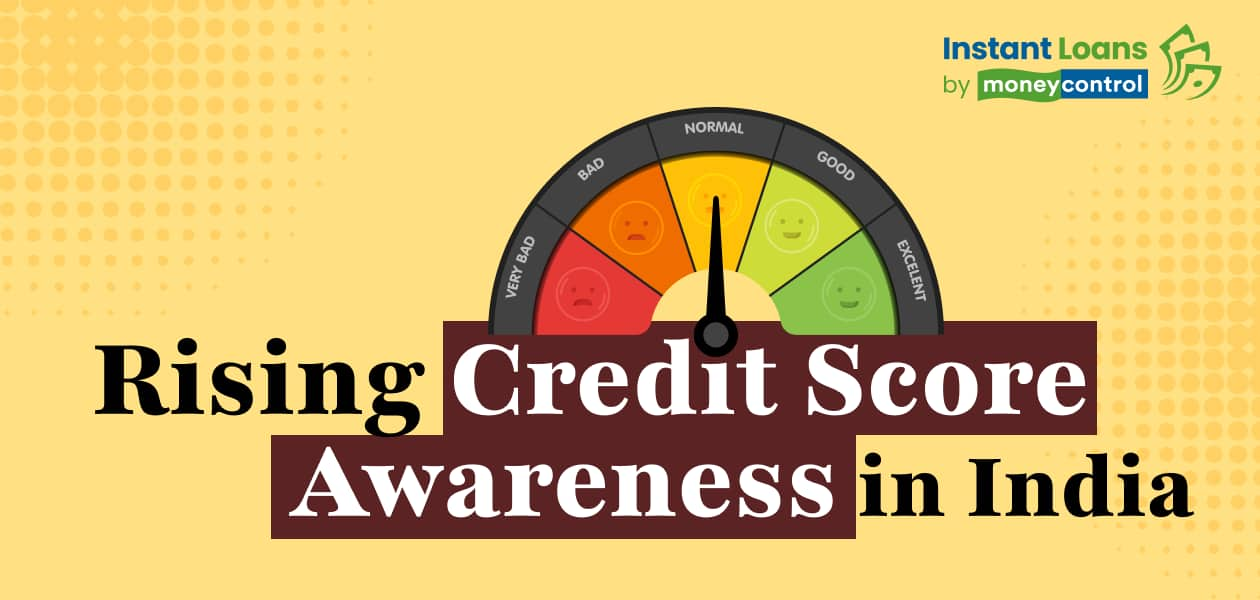

What is a Credit Score?

A credit score is a three-digit numerical representation of an individual's creditworthiness. This helps financial institutions assess the likelihood of a potential borrower’s loan repayment capacity. Ranging from 300 to 900, a higher credit score indicates a better credit history, making it easier to get loans and credit cards with favourable terms.

Credit Score Categories:

However, these credit score ranges and classifications may differ depending on the criteria of the credit bureaus. In general, a credit score of 700 or above is always preferred by lenders.

You can check your credit score for free via the Moneycontrol app and website. Moneycontrol also offers loans up to Rs 50 Lakhs in partnership with eight lenders. The loans can be availed at an interest rate starting at 10.5% per annum in a completely digital process.

ALSO READ: Credit Report: A step-by-step guide to read credit score report in detail

Your credit score plays a crucial role in determining your eligibility and the terms of a personal loan. Lenders use credit scores to assess your creditworthiness, which helps them decide whether you're a low or high-risk borrower. Here's how your credit score affects your personal loan eligibility:

To sum up, the rising awareness about credit facilities and financial services could be helpful in better management of personal finances. However, it’s advisable to keep a constant watch on your credit score and take simple steps to maintain a healthy credit profile.

If you are looking forward to checking your credit score for free, the Moneycontrol app could be a suitable option. Here you can check your credit score through CRIF Highmark, a leading credit bureau in India. Moneycontrol also offers personal loans up to Rs 50 Lakhs per annum in a 100% paperless process with interest rates starting at as low as 10.5% per annum. You can avail loans from eight lenders on a single platform through the Moneycontrol app.

Share it in your circle

Table of Contents

Explore Top Lenders for Instant Loan upto

Get Instant Loan up to ₹50 Lakhs with Zero Paperwork from Top Lenders

100% Digital

100% Digital Quick Disbursal

Quick Disbursal Low Interest Rates

Low Interest Rates