With the Reserve Bank of India holding the repo rate at 5.25 percent early this month, home loan rates seem to have entered a steady phase.

The long-running debate over fixed versus floating rates is no longer about predicting the RBI’s next move. Instead, it is increasingly shaped by a borrower’s finances, including income stability, loan tenure, repayment plans and tolerance for monthly EMI changes.

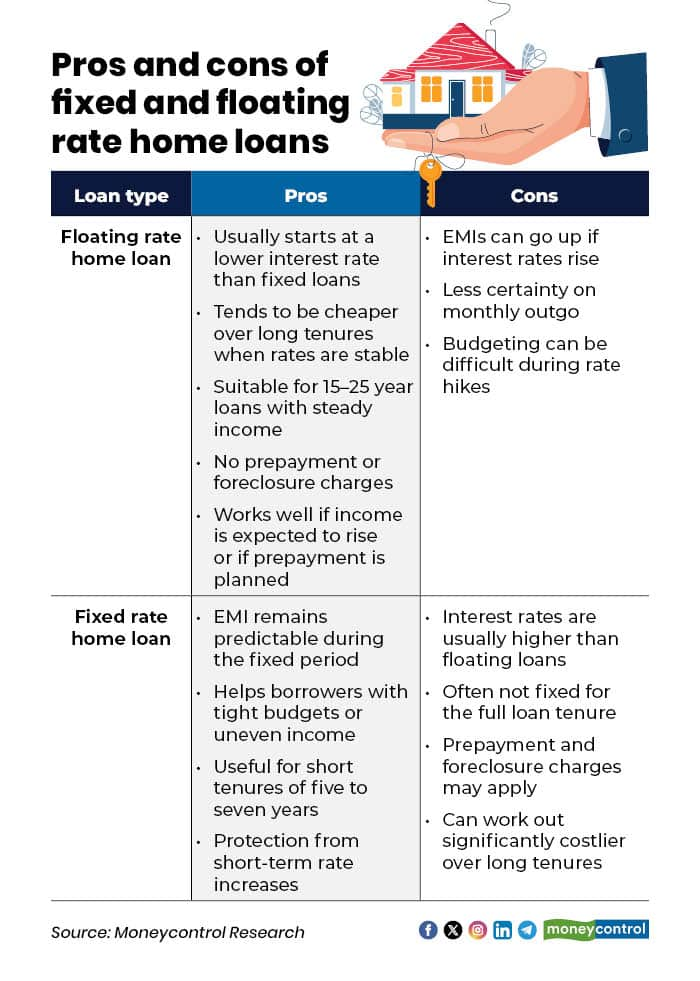

Experts say interest rates are cyclical and there may be multiple changes in the rate regime over a home loan tenure, which is typically long. It is also difficult to forecast the duration or the peaks/bottoms of rising and falling rate regimes. In this scenario, it is difficult to derive any real benefit from opting for a fixed-rate home loan based on the interest rate cycle.

"For borrowers with long loan tenures of 15 to 25 years and steady incomes, floating rates continue to make sense. They usually start lower and tend to work out cheaper over time when rates are stable," BankBazaar.com CEO Adhil Shetty said. Take a Rs 50 lakh loan over 25 years. At a floating rate of 7.1 percent, the EMI is about Rs 35,600 and the total interest comes to roughly Rs 57 lakh. At a fixed rate of 8 percent, the EMI rises to around Rs 38,600, pushing total interest closer to Rs 66 lakh. That is a gap of nearly Rs 9 lakh over the loan tenure, he said.

Not many lenders offer home loans on fixed rate for the entire tenure. And the ones that do are likely to charge significantly higher interest rates than floating-rate loans, as fixed-rate home loans carry higher credit risk for lenders.

Floating rates also work well for borrowers who expect income growth or plan to prepay, since lower starting rates magnify long-term savings.

"Some lenders may offer a mixed or hybrid rate home loan. The interest rates here remain fixed during the initial years of the tenure, but after the completion of the pre-determined fixed rate period, the interest rates become floating rates. Here too, the interest rates set for the fixed rate part of the loan tenure are usually higher than the prevalent floating rates," said Ratan Chaudhary, Head of home loans at PaisaBazaar.

Another major disadvantage of fixed-rate home loans is the levy of prepayment charges. "Lenders are free to charge prepayment/foreclosure fees on fixed-rate home loan borrowers, unlike floating-rate home loans, where no prepayment can be charged by the lenders," Chaudhary said.

Fixed rates, too, have their place. "Borrowers with shorter tenures of five to seven years, tight monthly budgets, or uneven income streams may prefer the certainty of a fixed EMI. Even small rate-linked EMI changes can strain household finances, and paying a bit extra for predictability can be a sensible trade-off," Shetty said.

There is no one-size-fits-all answer. With interest rates largely stable, the choice between fixed and floating home loans is best guided by personal financial comfort rather than market timing, say experts. Borrowers need to weigh income stability, loan tenure and flexibility needs carefully, as the right decision is less about where rates are headed and more about what fits household budget over the long term.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.