The Pension Fund Regulatory and Development Authority (PFRDA), the pension regulator, has relaxed several NPS (National Pension System) exit rules under the All Citizen Model, giving subscribers greater flexibility in how and when they can withdraw their savings.

The amendments are primarily aimed at the non-government sector and apply uniformly to both the Common Schemes and the Multiple Scheme Framework (MSF) of NPS under the All Citizen Model.

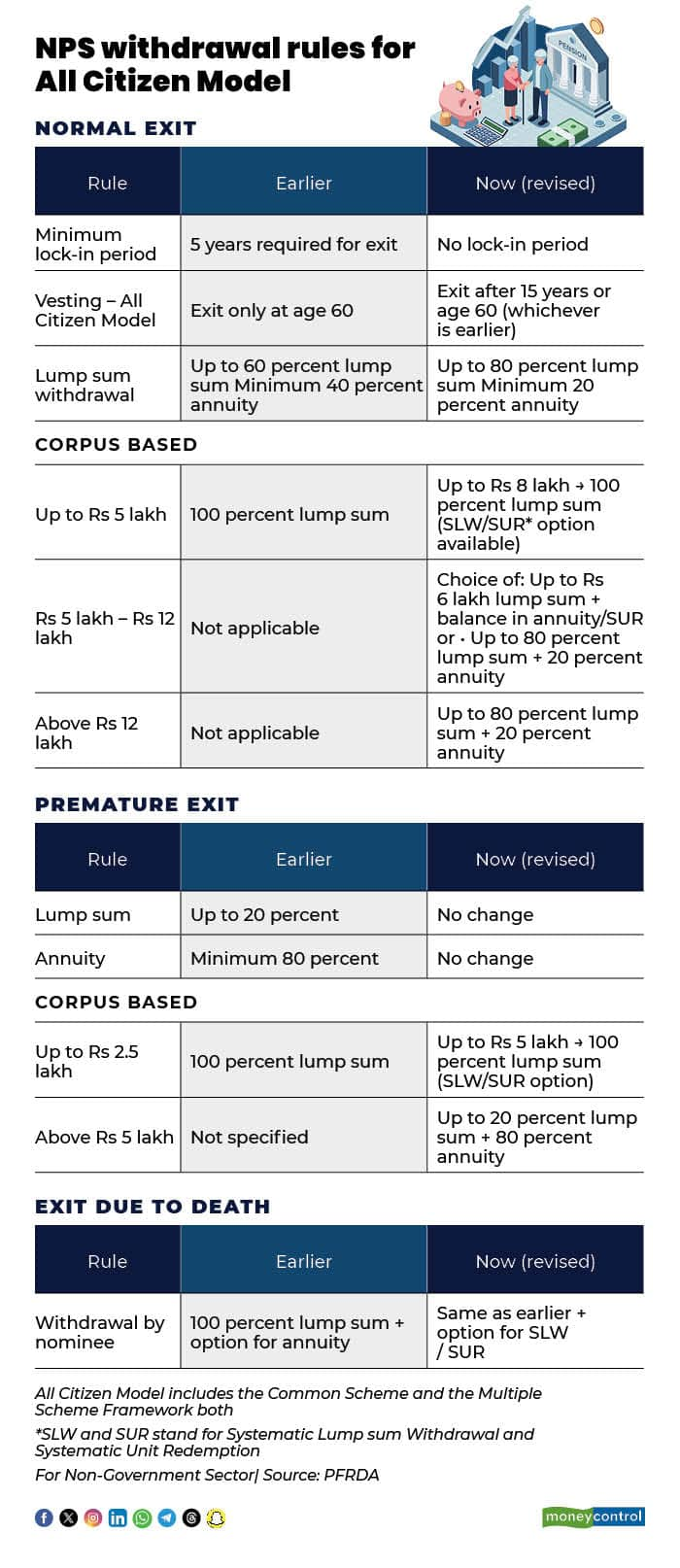

Maturity Exit

The biggest change is the removal of the minimum five-year lock-in period for normal exit under NPS - All Citizen Model. Earlier, subscribers had to stay invested for at least five years to leave the scheme. Now, they can exit without this condition, making the system more flexible for people with changing financial needs.

The vesting period has also been eased. Subscribers will now be allowed to exit after 15 years or at age 60, whichever comes first. Previously, they had to wait until they turned 60.

For corporate-sector subscribers, the vesting period remains unchanged. They will continue to exit at retirement or superannuation age, as before.

The regulator has also increased the lump-sum withdrawal limit for normal exits. Subscribers can now take up to 80 percent of their corpus as a lump sum, compared with the earlier cap of 60 percent. The minimum annuity purchase requirement has been reduced to 20 percent from 40 percent. This move will help retirees have more cash on hand while still ensuring a steady pension income.

“Subscribers can now withdraw up to 80 percent of the corpus as a lump sum. Of this, 60 per cent will be completely tax-free. The balance 20 percent of the corpus must be used to purchase an annuity,” said Pranay Ranjan Dwivedi, MD and CEO of SBI Pension Funds.

Withdrawal rules for small pension wealth have been made more detailed. Instead of a single threshold for full lump sum withdrawal, the new system introduces slabs and offers options such as systematic lump sum withdrawal (SLW), systematic annuity withdrawal (SUR), or a mix of lump sum and annuity. This gives subscribers more choice in managing their retirement money.

Premature Exit

For premature exit, the NPS rules remain largely unchanged. Subscribers can still withdraw up to 20 percent as a lump sum and must use at least 80 percent to buy an annuity. However, the slab-based options and systematic withdrawal facilities will now be available for smaller amounts, adding flexibility.

Upon the subscriber’s death, the entire pension wealth can be taken as a lump sum by the nominee, with the option to purchase an annuity. The new framework also allows nominees to use systematic withdrawal options if they prefer a staggered payout.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.