They might not be as well-known as mortgaging property to raise funds, but loans against cars can allow owners to access additional funds without having to sell their cars, providing a lifeline in times of financial emergencies.

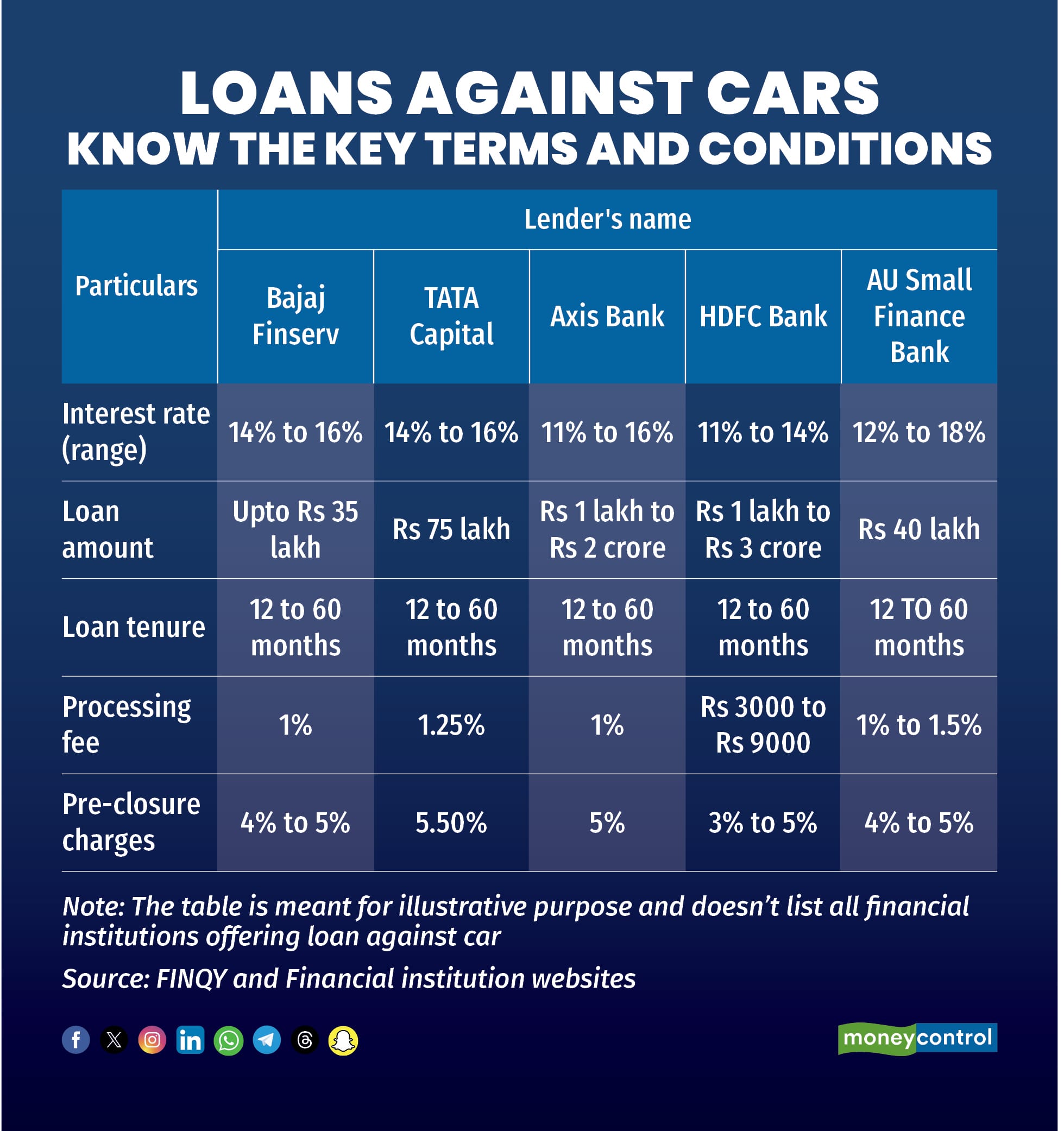

Banks and non-banking financial companies (NBFCs) like Axis Bank, IDFC First Bank, HDFC Bank, ICICI Bank, AU Small Finance Bank, Bajaj Finserv and so on offer car loans against vehicles up to 10-12 years old, with funding up to 200 percent of the car's deemed value. For instance, with a car valued at Rs 10 lakh, you could potentially borrow up to Rs 20 lakh from the bank.

What’s on offer

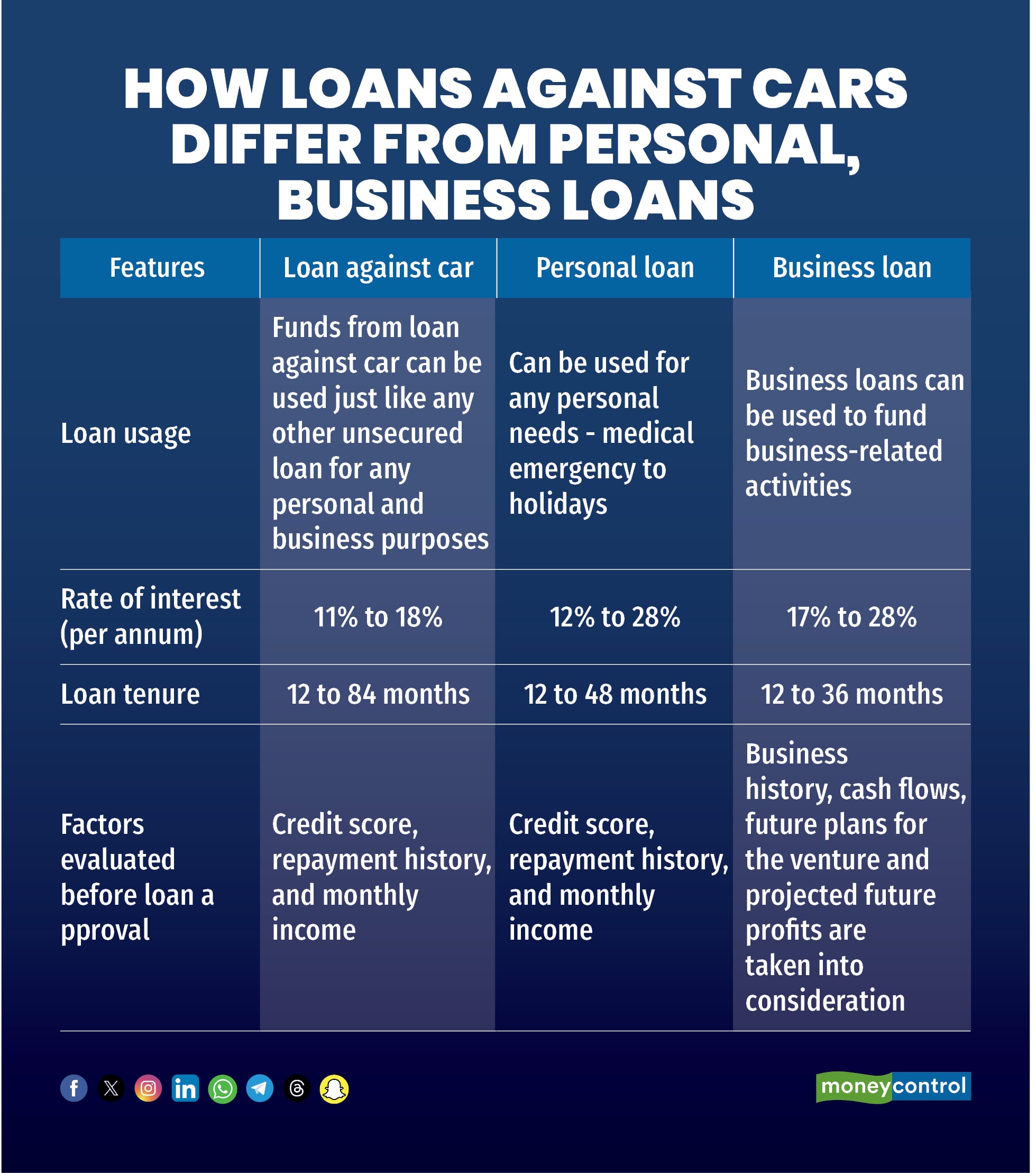

Unlike loans against gold or jewellery, where the asset is surrendered to the lender, a loan against a car offers the flexibility of being able to use the vehicle throughout the loan tenure.

Reserve Bank of India (RBI) guidelines and individual bank criteria govern the loan approval process. “Banks evaluate loan applications based on factors such as personal document verification, credit profile assessment, risk evaluation, internal bank policies and car valuation assessment to determine the customer's eligibility,” said Sunil Talreja, business head, auto loans, FINQY, a fintech platform offering loans, credit cards and insurance.

You will be eligible for such loans even if you have not paid off the money borrowed to buy the car. You need to have a minimum of 12 months' clear payment record on your existing loan, Talreja added.

Evaluate the costs

Interest rates for loans against vehicles range from 11 percent to 18 percent. A lower credit score and an older car may lead lenders to consider the loan a higher risk, potentially resulting in higher interest rates.

Harshil Morjaria, a certified financial planner at ValueCurve Financial Services, noted that interest rates for this kind of borrowing are lower than unsecured loans because of the vehicle collateral, which reduces lender risk. However, as in the case of all advances, timely repayment is crucial to avoid a negative impact on credit scores and future borrowing prospects.

Processing fees for loans against vehicles vary depending on the lender. For instance, Bajaj Finserv and Axis Bank charge 1 percent, while Tata Capital charges 1.25 percent. HDFC Bank has a fixed processing fee ranging from Rs 3,000 to Rs 9,000. AU Small Finance Bank charges between 1 percent and 1.5 percent of the loan amount.

Prepayment of such loans entails a penalty. This ranges from 3 percent to 6 percent of the outstanding principal amount. For instance, Tata Capital charges 5.5 percent, while HDFC Bank charges between 3 percent and 5 percent. “However, some banks offer relaxations after 12 months of the loan, with some even waiving prepayment charges entirely after 12-24 months of the loan tenure,” said Talreja.

Also read | Beyond tech giants: Three investment themes reshaping US markets

Understand the key clauses

When taking a loan against your car, it's essential to be aware of key terms and conditions. Financial terms that deserve thorough evaluation include the rate of interest, processing fees, prepayment charges, and EMI amount and due date. Additionally, you won't be able to sell the car until the loan is fully repaid, and you'll be required to maintain comprehensive insurance coverage, renewing it annually throughout the loan tenure.

Also read: Major financial changes in July: Revision of bank charges, new PAN rules, & ITR deadline extension

Default can prove to be costly

If a borrower fails to meet repayment obligations, his or her creditworthiness and credit score will suffer, making future borrowings more expensive due to higher interest rates. Banks, following RBI guidelines, have their own policies for handling defaults, which include tracking payment delays at 30-, 60- and 90-day intervals. “If the default persists beyond 60-90 days, the bank may initiate legal recovery procedures, and in extreme cases, repossess the vehicle from the borrower,” Talreja cautioned.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.