Major financial institutions such as State Bank of India (SBI), Bank of Baroda (BoB) and Bank of India have reduced their marginal cost of funds-based lending rates (MCLR). But borrowers who took home loans after October 1, 2019 may not benefit at the moment. Such loans are linked to an external benchmark, which in the case of most banks is the Reserve Bank of India’s (RBI) repo rate.

These banks’ move follows the banking regulator’s decision to take certain out-of-the-ordinary steps to lower cost of funds. These include allowing banks to exempt incremental retail loans in auto, residential housing and micro, small and medium enterprises (MSMEs) segments while calculating the cash reserve ratio (CRR) requirement.

It is the cash amount that banks have to mandatorily park with the RBI, but fetches them no interest. Easing the CRR maintenance requirement for these segments would, therefore, free up resources for banks.

Lowering the cost of fundsThe exemption will bring down the cost of funds and encourage banks to lend more to these segments. The idea is that the benefit of lower cost of funds will get passed on to customers. The central bank made the announcement as a part of its monetary policy review on February 6 and specified the details on Monday.

On cue, the SBI reduced its marginal cost of funds-based lending rate (MCLR) by five basis points (a basis point is 0.01 percentage point). Bank of Baroda and Bank of India, too, have lowered their MCLR by up to 10 bps.

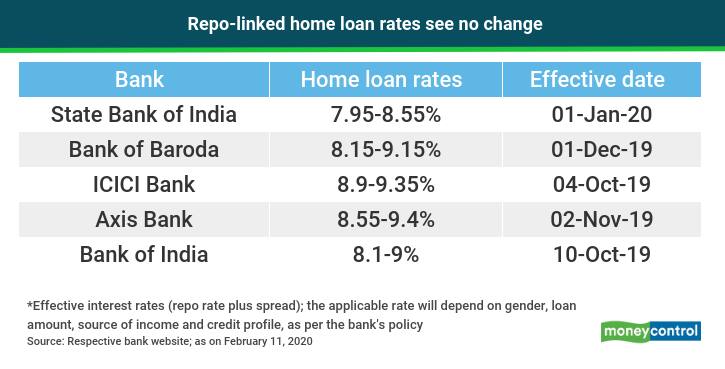

However, these banks have left their repo-linked lending rates (RLLR), to which new retail loans are pegged, unchanged so far. So, if you have taken a home loan or opted for a balance transfer after this date, you might not see a rate revision yet.

No rate relief yetFrom October 1, 2019, all banks have had to mandatorily link their new floating-rate retail loans to an external benchmark – RBI’s repo rate, three/six month treasury bill yields or any other benchmark prescribed by Financial Benchmark India Private Ltd (FBIL). Most banks have chosen the repo rate as their benchmark. For such retail borrowers, the effective interest rate is the repo rate plus a spread specified by the bank, which includes operating cost and credit risk premium.

While the repo rate is at the RBI’s discretion and credit risk premium can change in line with the borrower’s credit profile during the life of the loan, the other components, including operating cost, can be altered once in three years, as per the central bank’s circular mandating an external benchmark last year. “If your home loan is linked to the repo rate, one of the external benchmarks prescribed, you may not see a rate reduction due to the RBI’s latest move. On the other hand, if it is linked to treasury bill yields, banks’ lower cost of funds will reflect in these rates and your interest rate could go down, subject to the reset period of three months,” explains Madan Sabnavis, Chief Economist, CARE Ratings.

Since there is no repo rate cut, most new home loan borrowers will have to wait longer to gain from lower interest rates in the system. “Had there been a repo rate cut, the path of transmission would have been clear. My sense is that the CRR exemption will merely add to the bottomline of banks as the operational cost element cannot be changed now,” says Vipul Patel, Founder, MortgageWorld, a loan consultancy firm.

If your loan was sanctioned before October 1, 2019 and was linked to the MCLR, you will get the benefit of lower interest rates. Most banks’ pre-October home loans are linked to the one-year MCLR.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.