High and ultra-high net-worth individuals (HNIs and UHNIs) and other of their ilk have for long been the centre of attention for private banks’ premium banking divisions. In recent years, a sharp rise in the number of these affluent individuals has further intensified banks’ focus on this lucrative segment.

According to property consultant Knight Frank’s wealth report, the number of HNIs in India (worth $10 million and higher) increased by 6 percent year-on-year in 2024 to 85,698. Moreover, the number of billionaires in India increased 12 percent year-on-year to 191.

Not surprisingly, the growth in wealthy individuals in India and evolving customer expectations have been driving the demand for premium banking services, with banks offering tailored programmes, wealth management and customised solutions to this segment. “The wealth boom, coupled with a demand for personalised financial solutions, has fuelled the rise of premium banking,” said Arnika Dixit, president and head, wealth management, cards and payments at Axis Bank.

Uttam Tibrewal, executive director and deputy CEO at AU Small Finance Bank, attributes this trend to more Indians entering higher income brackets, which has resulted in a growing appetite for luxury, convenience and personalised financial solutions.

“The country’s HNI and UHNI segments have seen 13-14 percent CAGR (compound annual growth rate) in average household financial assets in the last five years,” said Sanjiv Roy, head of affluent banking and wealth management at RBL Bank.

Rohit Bhasin, President and Head, Affluent, NRI, Business Banking and Chief Marketing Officer said,” Affluent customers today evaluate banking by how well their bank understands their life, not just their finances. What we consistently hear is that convenience, recognition, and emotional connection matter deeply. When banking feels impersonal or transactional, even high-value customers disengage.” They’re not merely seeking financial products. They’re also looking for validation of their journey. When a customer feels seen, respected, and supported holistically—across family, lifestyle, and aspirations—that’s when banking becomes meaningful, he added.

Exclusivity the USP

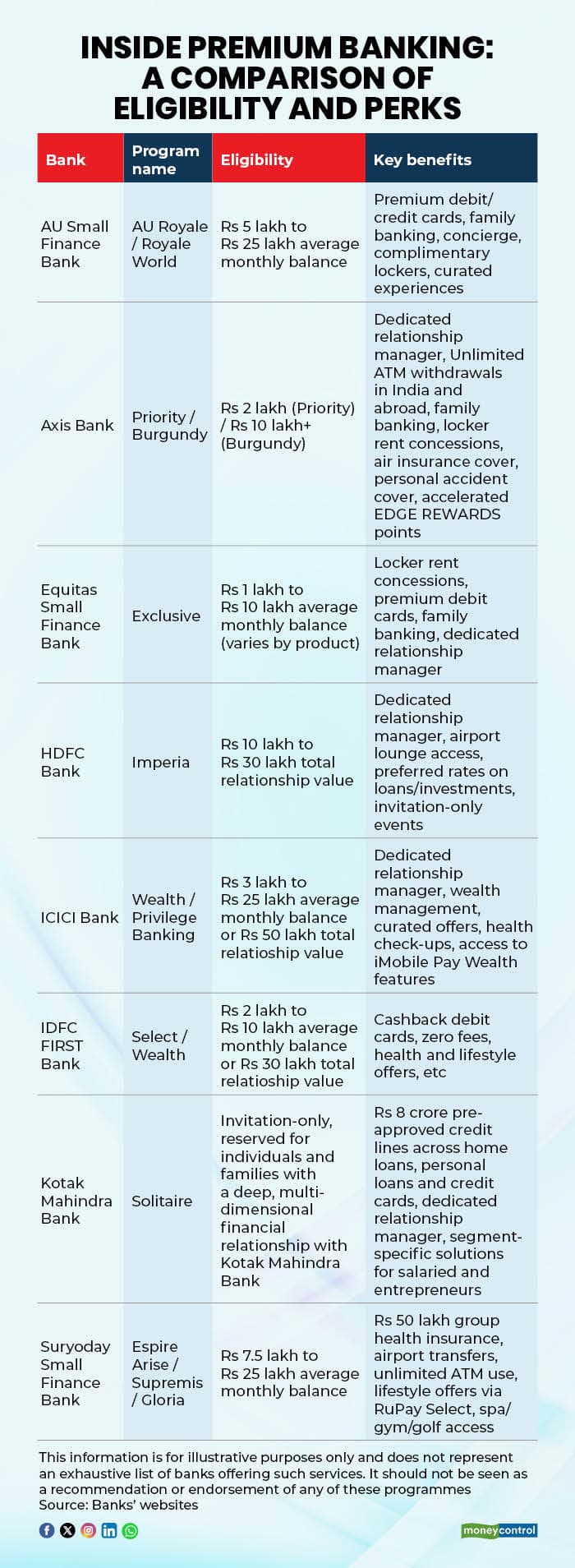

Banks are responding to this demand with tailored programmes and offerings, often positioned as exclusive benefits for select customers. For instance, AU Small Finance Bank offers high-value savings accounts, business accounts, corporate salary accounts, family banking solutions and credit cards, with eligibility based on balances ranging from Rs 10 lakh to Rs 25 lakh or a total relationship value (TRV) of Rs 30 lakh to Rs 2 crore.

Axis Bank provides two distinct programmes: Burgundy Private, requiring a TRV of Rs 5 crore or a net monthly salary credit of Rs 10 lakh, and Burgundy, with a TRV of Rs 30 lakh or a net monthly salary credit of Rs 3 lakh.

Similarly, RBL Bank’s Insignia Preferred Banking requires a TRV of Rs 30 lakh, while its Signature Banking programme starts at Rs 15 lakh. Kotak Mahindra Bank’s recently launched Solitaire programme for affluent customers, an “invitation only” proposition, based on a family’s engagement across deposits, investments, loans, insurance and demat holdings. The programme offers Rs 8 crore in pre-approved credit lines, across home loans, personal loans and credit cards.

Target customer segments

While premium banking teams target affluent customers, the profiles could vary across banks. For example, AU Small Finance Bank focuses on HNIs, corporate professionals like CXOs and directors, and tech-savvy millennials who prioritise digital-first banking. Axis Bank caters to high-value salaried professionals, entrepreneurs, promoters, founders and non-resident Indians.

Banks are offering mutual fund services, portfolio management services (PMS), alternative investment funds (AIFs), GIFT City-based international investments and private equity opportunities. They also advise and facilitate investments in equity, fixed income and alternative products, backed by in-house research and risk management.

Also read | Falling interest rates: Is now the time to lock into annuity plans for higher payouts?

No standard fee structure

The fees charged vary across banks and are linked to the balance in accounts and TRV.

Tibrewal said that AU Small Finance Bank’s top-tier programme has “no service charges”, with other offerings featuring discounted charges. For instance, for an AU Royale savings account, you can deposit cash up to seven times or Rs 5 lakh free per month, whichever limit is crossed first. After exceeding this limit, you'll be charged Rs 5 per Rs 1,000 with a minimum fee of Rs 100, and a fee for cancellation of demand draft of Rs 100 per instrument. Then, in case an electronic clearing service or National Automated Clearing House transaction is returned due to insufficient funds, the bank charges Rs 500 per instance. There is also a cross-currency mark-up fee of 1.5 percent while using a debit card for international transactions.

RBL Bank’s Roy explained that premium banking customers benefit from waived or discounted fees, and that there is no charge for not maintaining the requisite balance in the account for Insignia and Signature customers. Insignia customers also get access to rent-free locker facilities. Signature customers get to use lockers at no rent for the first year and then at a discounted 50 percent rent from the second year.

Sumanta Mandal, founder of TechnoFino, pointed out that banks generally do not charge extra for premium banking but require high account balances, which may yield lower returns compared to alternative investments.

Also read | Trump tariffs, MPC status quo: Align debt investments to your goals not events, say financial advisers

Privilege or mere hype?

Gaurav Goel, an entrepreneur and Securities and Exchange Board of India-registered investment advisor, said a personal relationship manager and prioritised service add value, but challenges emerge when the relationship manager changes, which happens quite often. “This creates service gaps, and many times they end up pushing or mis-selling products which have high inbuilt commissions for the bank. If a customer does not subscribe to these products, she may not be given satisfactory service at times,” said Goel.

Mandal, however, sees little difference between premium and regular banking, arguing that maintaining high balances for minimal benefits is not cost-effective. He advises against relying on relationship managers for investment advice. “They do not have the required product expertise, but are driven by commissions,” he explained. The products recommended may not align with your goals, he added.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.