In a volatile market, accumulating cash in a savings account may offer a sense of security but financial advisers warn it can limit wealth accumulation opportunities.

With average savings account interest rates typically around 4 percent annually, the returns are significantly lower than what market investments can give, leading to a real-terms loss of value due to inflation.

Financial advisers recommend investing in liquid or ultra-short duration mutual funds that offer better returns. Those comfortable with moderate risk can consider options arbitrage, hybrid, or equity funds to align their investments with long-term goals, balancing the needs for safety and growth.

Delayed investments, a wealth drain

Many savers fall into the inaction trap. A professional in her late 40s, for instance, built a comfortable buffer through consistent saving but repeatedly delayed deploying it elsewhere.

Over three years, the deposits grew but earned a mere 4 percent interest. In contrast, equity mutual funds averaged at 15 percent compounded annual growth during the period.

A Rs 5-lakh investment in equity-oriented funds at a conservative 15 percent annual return would have grown to Rs 7.5 lakh in three years. The same sum in savings account would have earned just Rs 60,000 in interest at 4 percent annual rate.

Across the country, this pattern plays out on the repeat — hard-earned savings stagnating amid a booming market.

Quantifying the hidden costs

Maintaining liquidity is crucial but beyond essential, it amplifies opportunity lost.

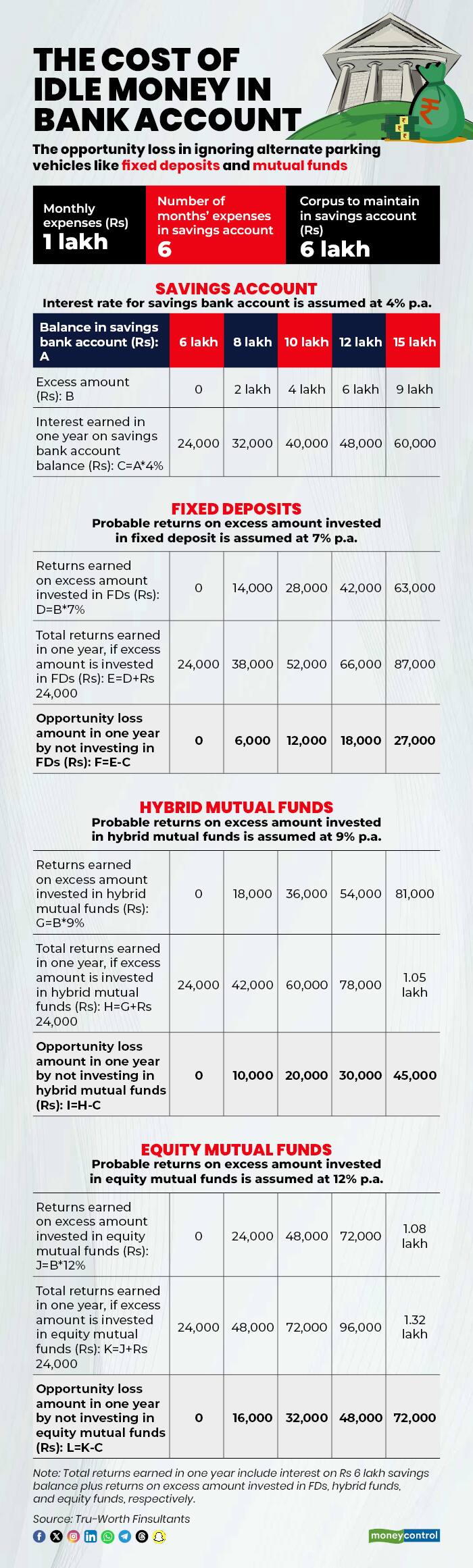

Consider a household with monthly expenses of Rs 1 lakh. A prudent emergency fund covers six months, or Rs 6 lakh, generating Rs 24,000 annually at 4 percent interest. If the balance swells to Rs 10 lakh due to bonuses or windfalls, the extra Rs 4 lakh drags down overall efficiency.

Consider investing the excess Rs 4 lakh in fixed deposits (FDs), you will earn Rs 28,000 as interest income (at 7 percent per annum). If invested in hybrid or equity mutual funds, the probable returns would be Rs 36,000 (assuming 9 percent returns) and Rs 48,000 (at 12 percent), respectively, in a year (see graphic). By investing excess funds, you can maximise returns while without touching the emergency corpus.

"As savings rates lag inflation, idle excess funds don't just miss growth — they diminish purchasing power," said Tivesh Shah, founder of Tru-Worth Finsultants.

How much in savings?

Savings accounts should serve immediate needs not hoard wealth. Beyond routine expenses and ongoing investments, allocate for contingencies such as medical emergencies, job transitions or unforeseen travel.

"Aim for 3-6 months of living costs to ensure liquidity without forgoing higher yields," advised Sanjeev Govila, CEO of Hum Fauji Initiatives, a financial planning firm. Anything surplus belongs in growth-oriented vehicles.

Also read | December 15 advance tax deadline: What you must pay today and cost of delay

Alternative avenues for surplus

Banks provide an easy solution: the auto-sweep facility. Link your savings to short-term FDs, and excess funds (typically above Rs 25,000-50,000) will be automatically swept into higher-yielding FDs, earning up to 7 percent interest while maintaining instant access.

Major banks such as Axis Bank, HDFC Bank, ICICI Bank, IndusInd Bank and Kotak Mahindra Bank offer this service, blending convenience with competitive rates.

"Sweep-in accounts bridge the gap, automating transfers to FDs for hassle-free optimization," Govila said.

For even sharper edges, pivot to liquid or ultra-short funds. These debt mutual funds deliver 6–7.5 percent returns, ideal for parking cash short-term. A diversified low-risk debt mix can further tailor to goals.

There are several tax-savvy options too. Arbitrage funds suit conservative profiles, offering equity-like tax treatment with minimal volatility. Hybrid funds balance debt stability and equity upside for moderate risk-takers, while pure equity funds fuel aggressive growth. Start small, consult an adviser, and scale thoughtfully.

Also read | Declutter your finances: A year-end money detox guide

Watch your steps

Having multiple savings accounts may seem organised but it can lead to unnecessary fees and oversight issues. Keep only what's necessary to avoid penalties and maintain required average balances.

The Deposit Insurance and Credit Guarantee Corporation (DICGC) insures up to Rs 5 lakh per depositor per bank. "Keep balances under this threshold, spreading across accounts if needed," Govila said. This shields against rare bank failures or RBI-imposed withdrawal curbs.

Consolidating accounts simplifies things: fewer statements, lower fees, and easier tracking.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.