Retirement income planning is fundamentally different from retirement saving. The question is no longer "How much can I accumulate? But how do I convert this into predictable cash flows without taking undue risk?".

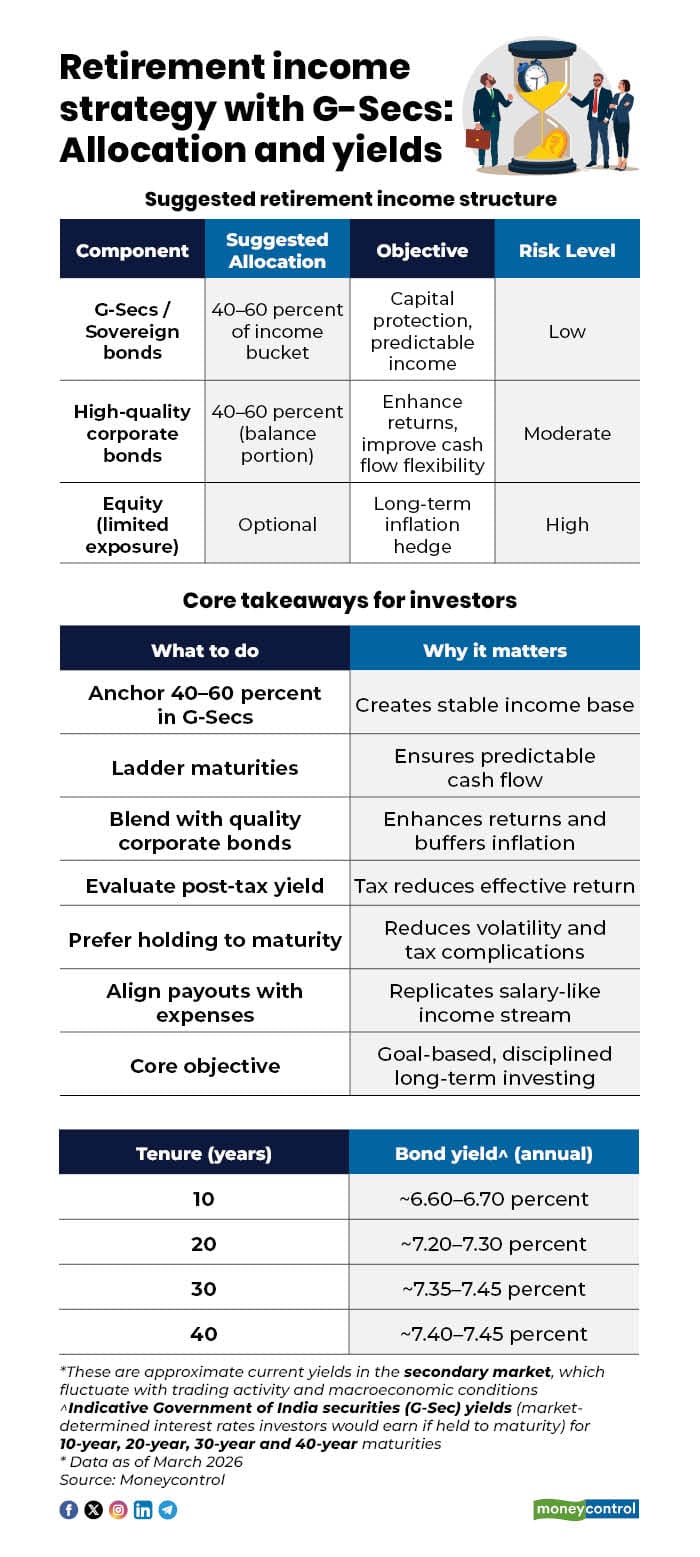

This is where Government Securities can become relevant, not as a token allocation, but as the stabilising core of a retirement income portfolio. Laddering maturities can help create predictable cash flows, especially for retirement planning.

Laddering maturities is an investment approach that involves buying multiple fixed-income securities with different maturity dates, creating a ladder of cash flows. By staggering maturities, investors ensure steady liquidity, lower reinvestment risk, and achieve reliable income, making it ideal for retirement planning to balance risk and returns.

At current yield levels, sovereign and quasi-sovereign issuances are offering competitive returns. For instance, recent issuances such as Bank of Maharashtra bonds have been available at 10-year bond yields around 6.9 percent. For a retiree prioritising capital protection and visibility of income, that can be meaningful, especially in a volatile equity environment.

Now consider a retiree with a Rs 1 crore retirement corpus and essential monthly expenses of Rs 50,000, or Rs 6 lakh annually. If Rs 60 lakh is allocated to G-Secs or sovereign-linked bonds yielding 6.9 percent, this would generate approximately Rs 4.14 lakh annually. This creates a predictable income base that covers a significant portion of essential expenses through relatively low-risk instruments.

However, retirement today can span 25 to 30 years, and inflation cannot be ignored. "Relying only on ultra-safe instruments may preserve capital but not purchasing power. This is where a blended fixed-income strategy becomes critical," said Saurabh Jain, Co-founder & CEO, Stable Money.

So this way, the remaining Rs 40 lakh could be allocated to carefully selected high-quality corporate bonds offering yields closer to 9 percent. At 9 percent, Rs 40 lakh can generate Rs 3.6 lakh annually.

In this scenario, the combined annual income from the portfolio would be roughly Rs 7.74 lakh, comfortably covering the Rs 6 lakh annual expense requirement while creating a buffer for contingencies or reinvestment.

"Many corporate bonds also offer structured monthly payout options, allowing retirees to align inflows with monthly expenses and effectively replicate a salary-like income stream," said Jain.

Experts say, "In practice, anchoring 40 to 60 percent of the income bucket in G-Secs for safety, while selectively adding higher-yield corporate bonds to enhance returns and cash flow flexibility, allows retirees to protect capital, generate predictable income, and better manage inflation risk without overexposing themselves to equity volatility."

However, one should also know that while corporate bonds offer higher yields than government securities, they primarily carry credit risk (default on interest/principal payments), interest rate risk (price drop when rates rise), and liquidity risk (difficulty selling before maturity). But they are less volatile than stocks and are subject to company-specific financial distress.

Taxation rules

Taxation depends on how returns are earned.

Coupon income from G-Secs is taxed as per the investor’s applicable income tax slab under “Income from Other Sources.” There is no concessional rate, so post-tax yield should be carefully evaluated.

If held until maturity, there is no capital gain since the principal is repaid at face value. However, if sold before maturity:

Gains after 12 months are taxed as long-term capital gains at 12.5 percent without indexation.

Gains within 12 months are taxed as per the applicable income tax slab.

According to experts, "For retirees and income-focused investors, holding to maturity enhances predictability and reduces tax and price volatility considerations. Evaluating returns on a post-tax basis remains critical when integrating G-Secs into a broader income strategy.

How to invest

Retail investors can invest in G-Secs directly through the Reserve Bank of India Retail Direct platform, either by participating in auctions or by buying in the secondary market.

NSE has also collaborated with RBI, enabling retail investors to start investing in Government Securities, mainly long-dated G-Sec bonds and treasury bills (T-bills).

They can also access G-Secs via online platforms, Demat accounts, and banks' websites, which provide curated options with clear visibility on yields and maturities.

"Withdrawal depends on market liquidity and secondary-market buyer availability. Since bonds are tradable instruments, an investor’s ability to exit before maturity is influenced by demand at that point in time," said Jain.

What the investor must know

Investors should understand that Government Securities are best used as the stable foundation of a retirement income plan, not as a token holding. By allocating around 40 to 60 percent of the income portion to G-Secs and laddering maturities, retirees can create predictable cash flows that cover essential expenses with relatively low risk.

However, they must also account for inflation, taxation and liquidity. Coupon income is taxed at the individual’s slab rate, and selling before maturity can trigger capital gains tax, so post-tax returns matter. Corporate bonds can enhance income but carry credit and liquidity risks. The key is to blend safety with selective higher yields, hold high-quality bonds to maturity where possible, and align payouts with monthly cash flow needs.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.