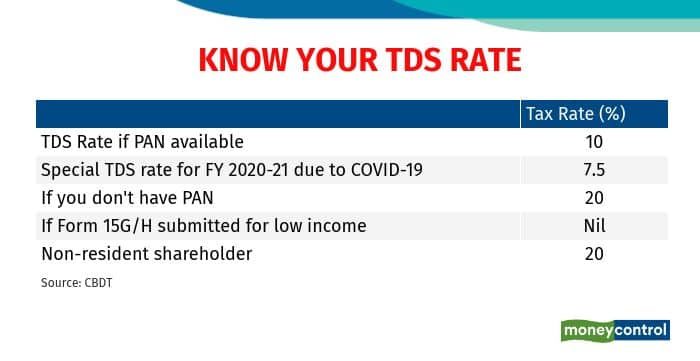

Many taxpayers have complained of late that their dividends below Rs 5,000 have been subjected to Tax Deduction at Source (TDS). As per income-tax rules, companies deduct a 10 percent TDS for dividends of more than Rs 5,000 in a financial year. The entire dividend amount is taxable at your slab rate. Due to COVID-19, the TDS has been relaxed to 7.5 percent for the current financial year. If you don’t have a Permanent Account Number (PAN), then the TDS rate is steeper, at 20 percent.

Also read: Majesco’s mega dividend announcement: What should investors do?

Abhay Joshi (name changed), who owns 500 shares of Sun Pharmaceutical Industries, recently saw a notification in his email stating that Rs 38 had been deducted as TDS for his Rs 500 dividend. The company hasn’t declared any other dividend so far this financial year. He is not the only one facing the wrongful TDS deduction. Mumbai-based chartered accountant, Mehul Sheth, says, “People who have received a dividend of Rs 300-400 too have been subjected to TDS.”

Why TDS is deducted

Earlier, companies deducted dividend distribution tax and handed over the funds to the shareholders. Budget 2020 tweaked the tax law this financial year and made dividends taxable in the hands of investors. However, companies were asked to deduct TDS. To give relief to small taxpayers, only dividends above Rs 5,000 were subjected to TDS.

So, why is TDS being deducted on smaller dividends?

Sheth says “Whether the Rs 5,000 limit pertains to all the dividends an individual gets in a year or the total dividend per shareholder that a company pays out in a year, is left to interpretation and hence registrars and share transfer agents (RTA) are not taking any chances.”

All that the Income Tax Amendment has said is that the TDS would be levied if the aggregate amount of dividend paid during the financial year to a shareholder exceeds Rs 5,000.

Also read: Why you need to file returns even if your employer deducts full taxes

Non-taxable income

What happens if you don’t fall in any tax bracket in the first place?

If your annual income is less than Rs 2.5 lakh and yet have been subjected to TDS for the dividends, file a Form 15G (all individual tax assesses) or 15H (individual above 60 years of age) to inform the company or the share registrar and transfer agent (RTA) about the non-taxability of your income.

The company’s registrar and transfer agent (RTA) or your demat account itself may have the details. Check if the latter offers a common form for your entire portfolio. Alternatively, you can find Form 15G/H online on your company’s or RTA’s website. Fill in the basic details: company’s name, if shares are held physically or through a depository participant (DP), your DP ID or Client ID and folio number.

“There is a need for a common procedure at the demat level through the depository participant,” suggests Paras Savla, Partner at KPB & Associates.

The last date for submission of Forms 15G/H to certain companies has already passed. For instance, Hindalco Industries had asked investors to email documents by September 4. Larsen & Toubro, mentioned November 4. In such cases, you would have to file a tax return by July 31, 2021 and claim a tax refund if your income is not taxable.

No TDS credit

Another issue that shareholders are grappling with is that the TDS collected from their dividend payment is not reflecting in the Annual Tax Statement or Form 26AS. This is crucial, as only when your company pays the TDS to the government – and this gets reflected in your Form 26AS – would you be eligible for a tax refund.

In the case of TCS for instance, which has doled out dividends twice during this financial year – July 31 and November 3 – some of its shareholders have written to Moneycontrol stating that TDS is not yet reflected in their Form 26AS.

“The tax credit in Form 26 AS would reflect after the company files the TDS return for that quarter,” says Ameet Patel, partner at Manohar Chowdhury & Associates. In simple words, if TDS is deducted in June, then the company has to pay the tax deducted to the government in the next quarter (July-September). “However, due to COVID-19, companies have got a leeway to file TDS receipts with the government till March 31, 2021. TDS credits in shareholders’ names would, therefore, appear after the companies pay the TDS to the government,” says Sheth. That means, you get your TDS refund as late as in June 2021.

What should investors do?

Check if your PAN is updated in your demat account. If your PAN is not registered with your demat account, you are subjected to a higher 20 percent TDS. Also, check for any emails or letters that your companies may have sent you, for any links or references to Form 15G/H, if you are eligible for a refund.

Also read: Receiving dividends from MFs? Submit these forms to avoid TDS if you have no tax liability

Else, contact your company’s RTA. If you don’t know who your RTA is, then check your company’s website for its RTA’s details. You might need to do that for as many companies that have paid you dividends on which you are eligible for a TDS refund.

Once you get the TDS certificates, ensure that your Form 26AS reflects it, by April 2021. Remember: the TDS on dividends deducted in financial year 2020-21 is 7.5 percent, but the actual tax would depend on the bracket you fall under, based on other income that you have.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.