With 85 percent of respondents forced to allocate over 40 percent of their monthly income to equated monthly instalments (EMIs), products like buy now, pay later schemes, instant loan apps, and personal loans are fueling widespread distress.

A recent survey by the Expert Panel, a debt and resolution firm, conducted from June to December 2025 among 10,000 financially distressed borrowers across India, uncovers a dire credit crisis.

The findings display systemic flaws in the lending ecosystem, from unsustainable debt loads to aggressive recovery tactics, calling for immediate reforms to prevent further economic fallout.

The overwhelming debt burden

Most borrowers, primarily from private sector jobs (61 percent), business owners (23 percent), and the unemployed (15 percent), struggle with unsustainable EMI-to-income ratios.

Most earn between Rs 35,000 and Rs 65,000 monthly, yet their average EMI obligations range from Rs 28,000 to Rs 52,000. This leaves little for essentials, pushing 85 percent into stressed categories where EMIs exceed 40 percent of earnings—well above the recommended 30 percent threshold.

Borrowing patterns show portfolios of 4 to 6 active loans from banks (45 percent), NBFCs (40 percent), and digital apps (15 percent). Credit card debt affects 65 percent, with averages of Rs 2 to 4 lakh and multiple cards held by 58 percent.

Job-related issues like job loss, salary cuts, delayed payments, or maternity leave trigger 28 percent of debt struggles. Then, medical emergencies (24 percent), business failures (22 percent), family expenses (18 percent), and investment losses (8 percent).

It starts with a legit need, but then you're borrowing more just to keep up with EMIs, and before you know it, you're stuck in a debt cycle.

Also read | Silver overtakes Nvidia to become the second-most valued asset in the world

Coping strategies and their toll

To manage repayments, borrowers employ desperate measures. Credit card rotation and new loans top the list at 40 percent, followed by family support (22 percent), salary advances (16 percent), and asset sales (15 percent), including gold (8 percent), stocks (5 percent), and property (2 percent). Alarmingly, 65 percent cut essential spending, such as food budgets, medical care, education, and insurance.

These tactics offer short-term respite of 2-6 months but exacerbate long-term woes through mounting interest and eroded assets.

Also read | Found errors in your EPS contributions? Here’s how to fix them

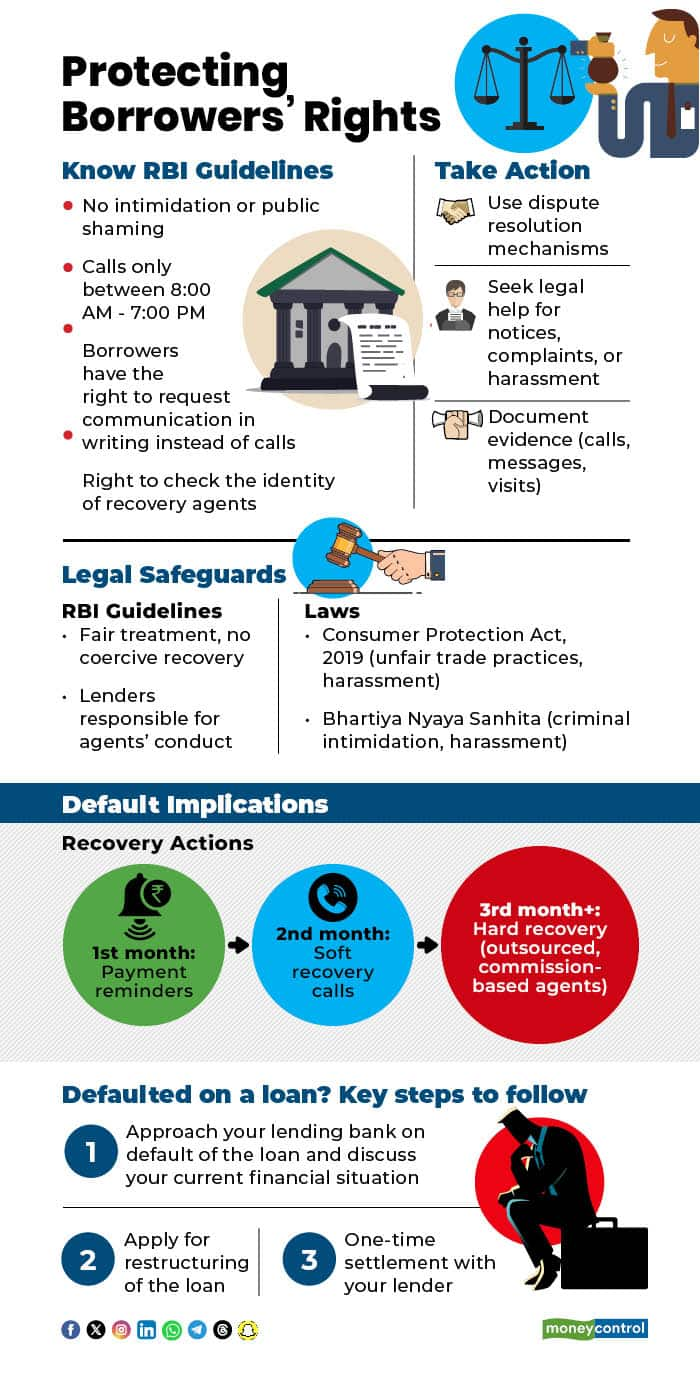

72 percent of borrowers face abuse from recovery agents

Recovery agencies intensify the crisis, with 72 percent of borrowers reporting harassment. Frequent abusive calls plague 67 percent, averaging 50-100 monthly, often outside RBI-permitted hours like early mornings or late evenings. Multiple daily calls from the same lender affect 39 percent, while 70 percent receive threatening SMS or WhatsApp messages.

Physical intrusions include home visits (11 percent), family threats (18 percent), contacting references (22 percent), and workplace involvement (12 percent). Borrowers face humiliation, with some getting abusive calls to relatives and midnight threats to managers.

Such tactics violate RBI guidelines on fair practices, yet limited awareness of redressal options like the Banking Ombudsman leaves victims vulnerable.

The survey highlights illegal practices—abusive language, unauthorized disclosures, and unannounced visits—underscoring the need for borrower education on rights.

Pathways to reform

Anurag Mehra, Director at Expert Panel, notes that harassment is counterproductive and often illegal, yet borrowers lack knowledge of protections. Recommendations include establishing debt relief procedures, licensing recovery agencies with penalties for violations, and mandatory financial literacy programs in schools and workplaces.

Further steps involve capping interest rates on high-risk loans, especially digital ones, creating settlement frameworks for negotiations, and tightening oversight of app-based lenders.

These measures aim to address root vulnerabilities, promote sustainable lending, and enable recovery within 12-36 months for most borrowers, who retain employment potential.

Conclusion

India's credit boom has turned into a distress epidemic, fueled by external shocks and destructive lending, not borrower mistakes.

With 85 percent overburdened by EMIs, the survey urges systemic reforms to foster dignity and hope. Implementing structured interventions could avert a larger financial crisis, empowering borrowers to rebuild amid economic volatility.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.