When Mumbai-based marketing executive Ronak Kothari, 38, took out a home loan from a large state-owned bank to fund the purchase of a new house, he was in for a bit of a surprise. He had applied for ― and was sanctioned ― a home loan of Rs 1 crore. However, the bank disbursed only Rs 80 lakh. Now, as he had used only Rs 80 lakh, he expected to be charged interest on this amount. Instead, Kothari says, the bank charged him interest on the entire Rs 1 crore. In short, he was asked to pay Equated Monthly Instalments (EMIs) on the sanctioned amount, not just the disbursed amount.

Upon complaining, the bank did reverse its stand, recalculated his EMIs, and started to charge him on the disbursed amount.

In reality, while some banks and financial institutions charge interest on the sanctioned amount, others charge interest on the disbursed amount. Why? Read on to understand.

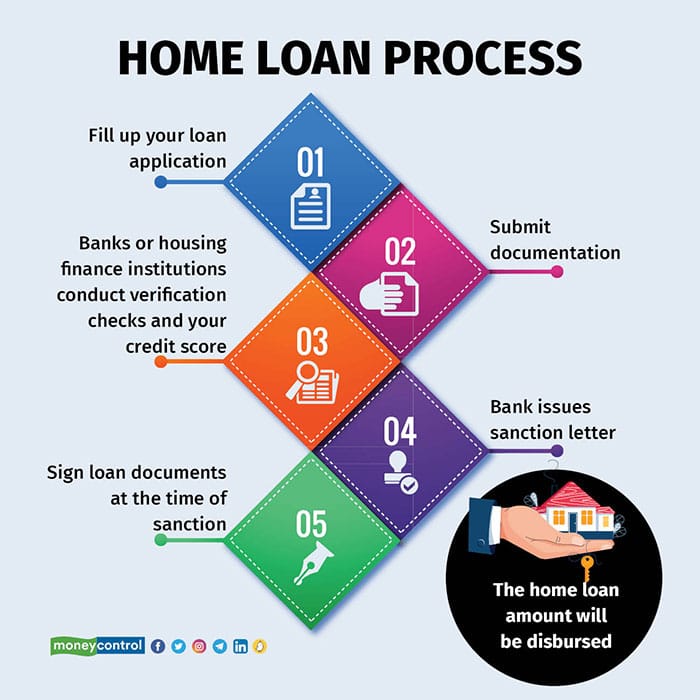

What is a home loan sanction letter?This is an official document that the bank issues to the borrowers intimating him/her of the loan approval, sanctioned amount, terms of the loan, and so on.

“We issue a sanction letter after studying the borrower’s credit history, income source, verifying the property to purchase, and so on,” says Gaurav Mohta, Chief Marketing Officer, Home First Finance Company. Some lenders take just up to 48 hours after application to issue the letter. Typically, it takes a week.

Federal Bank, for instance, takes between three and 14 days to sanction a home loan. “It depends on various internal processes, verifications and document checks, etc,” says Chitrabhanu K G, Senior Vice President and Country Head – Retail Assets and Cards, Federal Bank. Similarly, at HDFC Ltd, the entire process from the day of application till approval takes five to seven days.

The home loan sanction letter issued by the bank has limited validity because you cannot apply for a loan today and then use the money, say, after two years. However, the validity period varies from institution to institution. HDFC Ltd’s sanction letter is valid for three months from the date of issuance. “A lapsed sanction letter can be reopened, and it remains valid for a further three months,” says Hemant Panicker, Regional Manager – Mumbai & Vidharbha Region, HDFC Ltd.

Similarly, at the Federal bank, the sanction letter remains valid for 30 days.

Also read: Four ways to shorten your home loan approval time

I have got a home loan sanction for Rs 1 crore. Can I avail a loan for less than the sanction amount?Yes, you can.

Whenever a home loan is sanctioned for a particular amount, the lending bank or institution expects that the borrower will avail it fully. “If a borrower opts to take lesser than the sanctioned amount, the borrower can communicate the same to the bank prior to the disbursement so the banks can make the required amendments in the sanction order, documentation, and loan account which is opened at the bank,” says Chitrabhanu.

On the other hand, Ambuj Chandna, President – Consumer Assets, Kotak Mahindra Bank, points out that loans once sanctioned can also be cancelled. “If the conditions, on the basis of which the loan is sanctioned, are not met (property checks, documentation, good profiles of the borrower and builder), the loan can be cancelled,” he says.

Once the loan is sanctioned, the financial institution disburses the amount to the seller’s account or to the builder’s account directly. “In some specific cases where the customer has already made payment to the builder or a retail seller, the bank may consider reimbursing the same to the borrower’s account as long as the borrower provides necessary proof of having paid to the builder or retail seller,” says Chitrabhanu.

“If a buyer purchases a property which is under construction, then the bank or financial institution will disburse the loan amount either in stages or in full, depending on the stage of construction,” says Panicker.

I am applying for a home loan of less than the sanctioned amount. Here, will the financial institution calculate the EMI on the sanctioned amount or the disbursed amount?Generally, banks and financial firms such as HDFC, Kotak Mahindra Bank, and Home First Finance, among others, calculate the EMI on the total disbursed value irrespective of the sanctioned loan amount.

However, there are some banks which calculate the EMI on the sanctioned amount. For instance, at Federal Bank, if a borrower has taken a disbursement of 80 percent, the EMI is to be paid on the full sanctioned amount. “We calculate the interest only on the disbursed portion and adjust the additional amount paid to the principal portion of the loan,” says Chitrabhanu.

Also read: Buying your dream house? Be ready to pay five additional taxes and charges

There appears to be some miscalculation in the way my bank has calculated the EMI. What can I do?Talk to your bank. Register a complaint.

In case your bank branch is unable to resolve the issue, escalate it to a designated Grievance Redressal Officer.

For grievances against housing finance companies, Mohta says that it’s best to approach the National Housing Bank (NHB), the apex regulatory body for regulation and licensing of housing finance companies in India, to get the issue resolved.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.