and NPS are separate, and NPS does not affect EPF contributions")

The National Pension System (NPS) is often offered by employers as a long-term retirement benefit, promising tax savings and disciplined investing. However, with changing tax rules, lock-in conditions, lower tax home salaries, and other investment options available, the key question is whether investing in NPS through your employer still makes sense for you or if there are better ways to plan for retirement today.

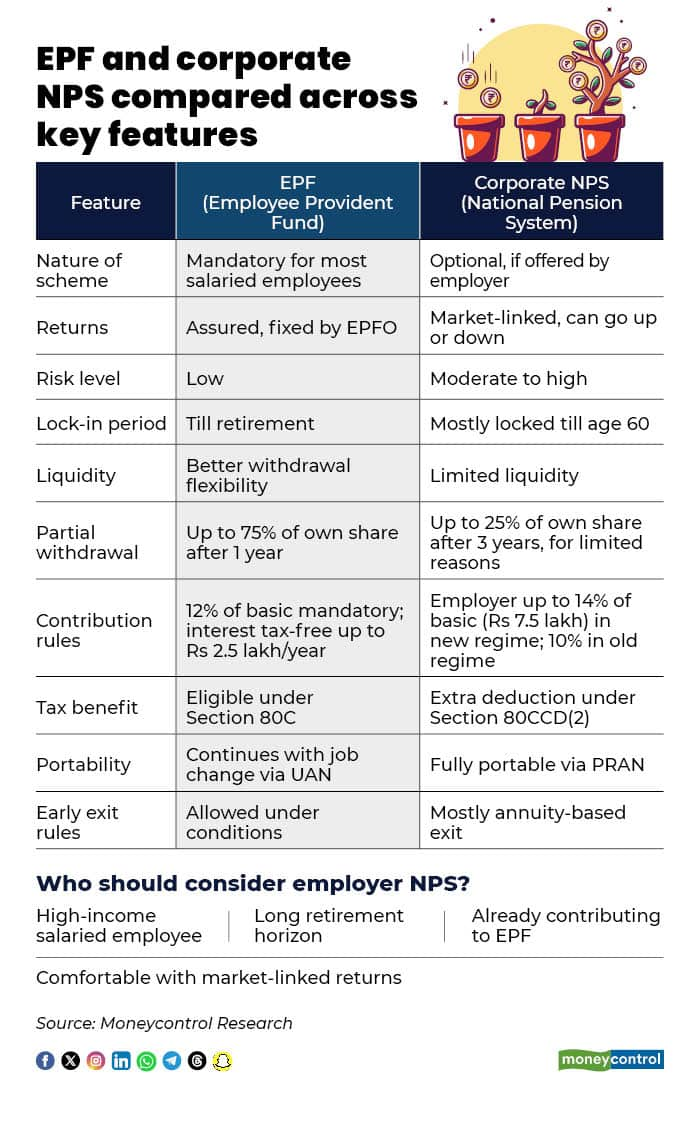

First, note that NPS is optional and depends on personal preference. It mainly helps with tax efficiency. Employer contribution to NPS qualifies for an extra deduction under Section 80CCD(2) over and above 80C limits, even under the new tax regime. It is useful for higher-income employees with long retirement horizons. Also, NPS has a lock-in till retirement and offers limited liquidity.

Ranbheer Singh Dhariwal, Group Head - Social Security and Welfare at Protean eGov Technologies, said that it makes sense to invest in NPS via your employer because corporate NPS is among the most efficient retirement savings avenues available to salaried professionals.

Singh said employers make contributions of up to 14 percent of basic salary (up to Rs 7.5 lakh a year) under the new tax regime and 10 percent under the old regime, and are eligible for deduction under Section 80CCD(2). This makes it the only meaningful tax-saving lever available in the new regime. This is a structural advantage. It allows employees to build a significantly larger retirement corpus.

“With recent policy clarity and increasing employer adoption, corporate NPS is fast emerging as a core pillar of long-term financial planning rather than a peripheral benefit,” said Singh.

Is EPF deduction also mandatory?

Employee Provident Fund (EPF) and NPS are separate, and NPS does not affect EPF contributions. Choosing NPS does not automatically stop EPF. Kunal Kabra, Founder, Kustodian.life, says, “For most employees already enrolled, EPF cannot be opted out of later. Only first-time employees above the wage threshold may decline EPF upon joining.”

Additionally, if both EPF and NPS contributions are structured under CTC, your take-home pay may be reduced, which can be partly offset by tax savings.

Sudhakar Sethuraman, Partner, Deloitte India, said, "EPF deduction is mandated at present, and there are conditions to coming out of EPF in total. However, NPS contribution has no impact on EPF, though both are schemes for retirement benefits. Since the contribution to NPS comes out of the salary of the individual, take-home would be reduced, even after considering tax benefits for such contributions."

This means corporate NPS operates alongside EPF as an additional employer-provided retirement benefit. Under labour law, the minimum monthly EPF contribution is Rs 1,250, and as salary increases, the EPF deduction increases accordingly. If your corporation allows you to continue with the minimum EPF contribution, the employee can transfer the surplus EPF amount to NPS and avail its benefits, which will also support their long-term financial planning.

What happens to NPS if you change jobs early

NPS is fully portable and is linked to a Permanent Retirement Account Number (PRAN) that remains with the individual across job changes, sectors, or even self-employment. However, funds are largely locked till age 60. Early exit is allowed, but most of the corpus must go into an annuity, with limited lump-sum withdrawal.

Sethuraman says, "A minimum contribution of Rs 1,000 is required to keep the NPS tier 1 amount active. An individual needs to wait until the end of year 3 to opt for partial withdrawal."

As noted above, the system provides some liquidity while maintaining its long-term retirement focus.

"Partial withdrawals of up to 25% of the subscriber’s own contributions are permitted for specific purposes, subject to defined timelines. In addition, there can be a premature exit from NPS if the total corpus is less than 5 lakhs. As per the latest updates in the schemes or under NPS, a full exit is allowed after 15 years of participation," said Singh

Moreover, even if an individual leave the corporate setup, the NPS account continues uninterrupted and can be converted to a retail account, ensuring continuity of retirement corpus accumulation.

Should you opt for NPS above EPF?

Unlike the EPF, NPS returns are market-linked and not guaranteed. Both these schemes are unique and have their own benefits, so the smart strategy can be to use both in tandem rather than choosing just one.

Singh said, "EPF provides a stable, risk-free foundation with assured returns and tax efficiency. NPS, on the other hand, brings growth, flexibility, and choice with equity exposure. Together, they create a well-balanced retirement strategy, combining capital protection with inflation-beating growth."

In today’s context of longer life expectancy and rising post-retirement costs, relying on a single instrument is no longer sufficient. One can use a blended EPF–NPS strategy.

Additionally, Kabra said, "EPF should be the base; it offers stable returns and better withdrawal flexibility. NPS works well as a tax-efficient add-on for long-term retirement growth. For most salaried employees, using both, not choosing one over the other, is the practical approach."

However, Sethuraman says the decision entirely depends on the individual. "This is based on individual’s appetite for risk (whether their retirement corpus needs to be earn interest at assured rates of EPFO or be subject to market performance, which could make the value of the corpus grow or decline) and other factors."

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.