Vaibhav Agrawal

Why should you invest in equity linked savings schemes (ELSS)? Broadly, there are four reasons for investing in ELSS. Firstly, it offers you tax benefits under Section 80C of the Income Tax Act, up to a maximum limit of Rs 1.50 lakh. This is part of an overall umbrella limit that the ELSS shares with other tax saving options and outlays.

Secondly, ELSS funds have a lock-in period of just three years, which is lower than other tax saving instruments like PPF, long-term deposits, ULIPs, etc., which have a minimum lock-in of five years. Thirdly, ELSS is also a tool of wealth creation as it is invested in equities and the lock-in ensures a long term approach to investing. Lastly, the three-year lock-in makes it a good way to start off your equity market journey.

Is there an upper limit for investing in ELSS?

There is no upper limit to how much you can invest in ELSS. Of course, your overall limit under Section 80C will be limited to just Rs 1,50,000 per annum. But you can invest any amount in ELSS, even after you have crossed the limit prescribed by Section 80C. In fact, for first-time investors who have just started paying tax, ELSS is a powerful tool that combines tax saving and wealth creation.

There is one more interesting aspect about investing in ELSS. Since there is a mandatory lock-in period of three years for these funds, fund managers have the leeway to take a long-term approach to the portfolio. That is because liquidity requirements are not as high as for other kinds of equity funds. This helps align the goals of the fund manager with those of the investors.

Is it wise to invest in ELSS after exhausting the Section 80C limit?

Let us suppose that you have surplus funds of Rs 2.25 lakh that you could invest. Of the total, you invest Rs 1.50 lakh in ELSS to get the full benefit under Section 80C. But do you invest the rest in ELSS as well? The argument is that since ELSS come with a lock-in period of three years, they will outperform the index, considering that fund managers will also take a long-term view and hold less cash. Here is how you can decide:

Unlike a diversified equity fund, an ELSS has a mandatory lock-in period of three years. It does not matter whether you are getting Section 80C benefits or not. The lock-in period of three years will still be applicable. The million dollar question is whether you should be locking in funds without any special tax benefit. Or would you be better off investing in diversified equity funds and maintaining the discipline of long-term investment?

You should never make an ELSS allocation decision in isolation. It should be part of your overall financial plan. Remember that ELSS will qualify as equity exposure in your overall financial plan. You need to take this decision based on the total exposure to equities that your plan allows. If the ELSS is going to overexpose you to equities, you need to be careful because you are locked in for a period of three years at the very least.

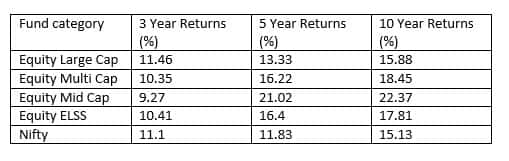

Finally, ask yourself a pertinent question -- What is the return advantage that ELSS provides over diversified equity funds? Consider the table below. If you look at it over a 5-10 year period, there is no great advantage that ELSS has over a multi-cap fund. Of course, mid-caps have done a lot better than ELSS but they belong to a different risk profile and hence, are not entirely comparable. Apart from the tax benefit, there isn't much else that makes ELSS a better form of investment.

The crux of the matter is that investing in ELSS beyond the Section 80C limit does offer an investor much value. That is because the incremental benefits of an ELSS over a diversified fund in terms of risk-return trade-off are quite negligible if the tax exemption factor is set aside. On the contrary, it exposes you to liquidity risk without commensurate returns. As an investor you are better off just sticking to diversified equity funds once your Section 80C limits are exhausted. At least, when it comes to rebalancing your portfolio, you will not be stuck to your assets because of a lock-in!

(The writer is Head of Research and ARQ at Angel Broking. Views expressed are personal)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.