In this edition of tactical pick, we have selected Tata Global Beverages (TGB), which has been strategically repositioned for a wider FMCG platform after the recent Tata group consolidation of the consumer facing businesses.

Redux consumption offerings First, consolidation of the consumer businesses from Tata Chemicals with TGB extends the latter’s portfolio from beverages (coffee, tea and water) to food ingredients and helps it in de-risking the portfolio from vagaries of the individual beverage business cycle.

Secondly, consolidation opens up the company to newer categories, which are more complimentary to its existing portfolio such as macro snacks (Britannia), other beverages such as juices (Dabur) or other staples products (ITC’s portfolio). Going forward, following areas are under the radar -- dairy business, entry into high growth/high margin home and personal care categories and mix of organic and inorganic expansion.

Thirdly, while the transaction is margin accretive, there is insignificant assets or liabilities been taken over by TGB. This implies improving RoCE (Return on Capital Employed) profile, which had been sub-optimal in recent past. A ballpark estimate suggest around 400 basis points (100 bps=1 percentage point) improvement in RoCE.

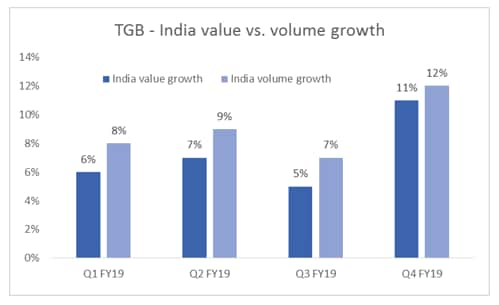

Incremental confidence comes from Q4 result The recent Q4 FY19 result highlight that pricing power is improving in the domestic tea business. Price hikes implemented in recent times have been useful in reducing the gap between value and volume growth in the domestic business (49 percent of TGB’s sales).

Domestic tea value, volume growth

Consolidation in a fragmented tea industry TGB is acquiring branded tea business of Dhunseri Tea, which helps it to extend its limited presence in Rajasthan. We think more such acquisitions like this are possible in the domestic market.

Other tailwinds TGB’s key subsidiary (57 percent stake) -- Tata Coffee (13 percent of consolidated profit) -- is witnessing improving trends in the branded coffee portfolio. Also key joint-ventures -- Tata Starbucks and NourishCo -- are close to break-even.

Key risk: Long gestation period for new FMCG categories to fructify.

Valuation gap to reduce: Repositioning of TGB in the FMCG universe can help it bridge the valuation gap to some extent. At present, TGB trades at 22 times FY20 estimated price-to-earnings, which is about 50 percent discount to the trading multiples of frontline FMCG stocks.

For more research articles, visit our Moneycontrol Research pageDisclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.