Neha Dave Moneycontrol Research

Sundaram Finance is one of the most stable retail asset financing non-banking financial companies (NBFCs) with a presence across diverse products. Through its various subsidiaries it has a presence across multiple facet of the financial services industry including housing finance, asset management and general insurance.

Asset financing NBFCs are staring at multiple challenges of rising rates, increasing fuel cost and sustainability of asset growth. In such a scenario, Sundaram Finance is a safe bet considering its long demonstrated track record of stable and profitable growth across business and interest rate cycles, delivering mid-teens return on equity (RoE) for the past 10 years.

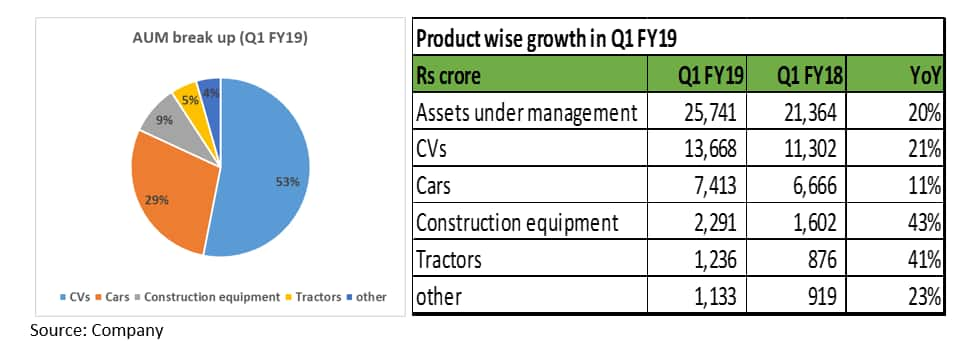

Vehicle financing to drive loan book growth Asset under management (AUM) stood at Rs 25,741 crore as at June-end. It registered a 21 percent year-on-year (YoY) growth, driven by steady 20 percent growth in commercial vehicle (CVs) loans. The asset mix is diverse but CVs financing still constitutes over half the book.

CV financing will continue to remain a growth driver for Sundaram Finance aided by government investments in the roads sector, higher budgetary spends for the rural sector and expected finalisation of the scrappage policy or voluntary vehicle modernisation programme. Impact of axle load norms is likely to be offset by healthy underlying demand. CV sales remained strong in August due to healthy demand across sectors.

We derive a lot of comfort from Sundaram Finance’s over six decade track record in the CV financing business. The company benefits from strong parentage of the group which is present across the value chain in automobile sector as auto manufacturer, original equipment manufacturer (OEM) supplier and financier.

The management’s experience and understanding of target segments has enabled the company to deliver strong return while keeping asset quality under control over multiple business cycles.

The gross and net non-performing asset (NPA) ratios stood at 1.7 percent and 1.1 percent, respectively, as at June-end. Strong customer relationships, with around 60 percent of CV borrowers as repeat customers, provides the company an edge in maintaining portfolio quality over peers, especially in downturns.

Modest growth in the housing finance space Sundaram BNP Home Finance remains a modest player in the housing finance segment, with operations largely restricted to South India, and loan book of Rs 8,532 crore as on June 30. Following three years of decline in business volumes, disbursements grew 43 percent in FY18.

In Q1 FY19, disbursement increased by 29 percent YoY. However, asset quality deteriorated with gross NPA increasing to 4.34 percent from 3.27 percent in Q4 FY18. Asset quality was impacted largely by delinquencies in the non-housing loan segment (31 percent of portfolio as at June-end). We are encouraged by the fact that incrementally the management’s focus is on the housing segment. It has initiated the legal process for recoveries from these NPAs by taking physical possession of properties. As per rating agency ICRA, NBFCs are awaiting the final court order on cases for almost one-fourth of NPAs.

Healthy performance of other subsidiaries Sundaram Asset Management’s average assets under management (AUM) remained almost flat at Rs 34,886 crore as at June-end. However, the asset mix turned favourable with high fee earning equity assets at 60 percent of AUM as at June-end compared to 46 percent a year ago.

Royal Sundaram reported 14 percent YoY increase in gross written premium to Rs 759 crore in Q1 FY19. Combined ratio improved to 109 percent from 112 percent last year.

Consistent profitability and calibrated growth Despite the stiff competition from banks and other NBFCs putting downward pressure on yields, its margin has been resilient. The company’s ability to raise funds at competitive rates from diverse sources supports margin. This along with superior operating efficiency and low credit costs is expected to help the NBFC report stable and comfortable profitability with return on assets (RoA) around 2 percent.

Sundaram Finance calibrates its growth strategy in line with market conditions and has not hesitated to curtail lending in times of heightened stress. While there is scope of widening and deepening of the lending portfolio further, considering the group’s conservative approach, business growth is expected to be more measured over the medium to long term. Capital adequacy moderated after the insurance stake acquisition. However, internal accruals are adequate for mid-teen growth in the loan book. Accordingly, we expect the company to grow its lending book albeit at a gradual and steady pace, improving RoE.

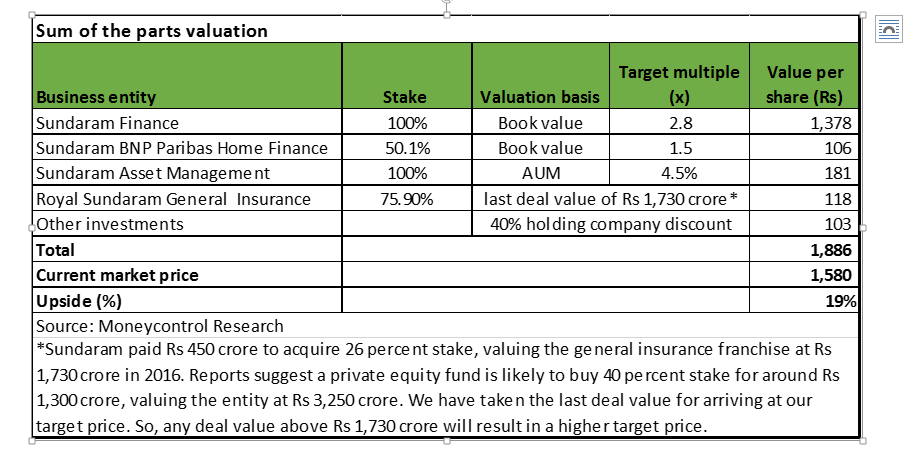

The other financial services business like AMC and general insurance are expected to grow in sync with India’s economic growth. We have valued the stock on a sum of the parts (SoTP) basis and see reasonable upside to the current market price. The stock is trading at 2.2 times FY20e price-to-book, which is reasonable given its consistent performance.

The demonstrated track record of stable and profitable growth across business cycles, established franchise with experienced senior management team and strong overall asset quality makes Sundaram Finance a worthy inclusion in the portfolio. Investors, with a long-term horizon and wanting to participate in a steadily compounding diversified financial services company, should buy into the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.