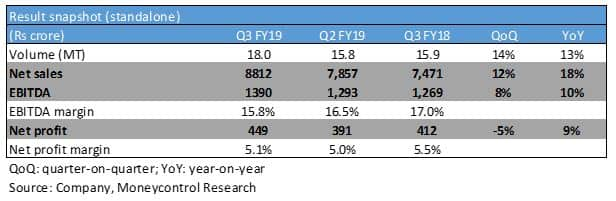

UltraTech Cement, India’s largest cement maker, posted a decent performance in Q3FY19. Standalone revenue grew 18 percent year-on-year (YoY) driven by incremental volumes resulting from the consolidation of cement assets of JP Associates (JPA). Volume growth of 13 percent was driven by strong domestic cement demand.

Earnings before interest, tax, depreciation and amortisation (EBITDA) was Rs 1,390 crores compared to Rs 1,269 crores in the same period last year. EBITDA margins contracted ~120 bps YoY and 70 bps quarter-on-quarter (QoQ) on a rise in input costs.

Realisations were better YoY but subdued sequentially as cement prices weakened in most parts of the country during the quarter. Cost per tonne fell sequentially as prices of key inputs pet coke and crude oil moderated. However, the realisation decline kept the EBITDA per tonne under pressure on a sequential basis.

Large scale infrastructure construction activities aided healthy demand and in turn volume growth. UltraTech expects the demand trend to outpace the GDP growth rate in the near term.

UltraTech (CMP: 3,795; Market cap: 1,04,225 crores) has been consolidating market presence through mergers and acquisitions and has increased cost discipline to bring in operating efficiencies. Although it enjoys a strong market leadership position, the current valuations appear stretched from a medium-term perspective. The market continues to remain volatile and long term investors can look forward to accumulating this stock during corrections.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.