NOCIL's Q3 performance reflects the slowdown witnessed in end market – auto sector - on the chemicals supply chain.

Table: Q3 financials

Also Read: Trade war a growth opportunity for rubber chemical major

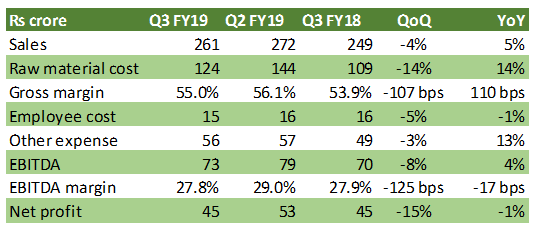

Key concernsSequentially, there was a 4 percent decline in sales as the Auto industry (both domestic and China industry) is witnessing a subdued demand slowdown.

Three factors have contributed to deferred buying. One is US-China trade war has led to uncertainty in terms of demand, secondly in an unusual phase of sharp decline in Oil derivatives (Benzene etc) customers have resorted to cautious approach towards buying. Customers have a bias for Just in time (JIT) purchase rather than a regular contracted supply. Thirdly, end market demand has dropped. In the current quarter itself, various tyre manufacturers and OEMs have resorted to plant shutdowns.

Gross margins contraction was attributed to high cost inventory.

Key positivesHowever, adjusting for high inventory cost margins are broadly stable. Company reports that for majority of the products price adjustments commensurate with the input cost changes helping it to defend margins. In the near term, H2 FY19, management guides for flattish production volume growth. This means FY19 volume growth is expected to be ~5 percent YoY.

Margins are also expected to be flat, unless additional cost cut measures are taken. This implies 27-29 percent margin profile to continue till anti-dumping duty is enforce.

Secondly, US-China trade partially helps in US export opportunity. Towards the end of last quarter company has started supply quantum of 500 tonnes per annum for the US market.

Key observationsOn a medium-term, the company remains positive on global and domestic opportunity on the back of committed expansion plans from global and domestic tyre industry have of the order of $ 10 billion and ~Rs 18000 crore respectively. Secondly, due to declining supply from the China due to environmental compliance, NOCIL has emerged as one of the secured source of rubber chemical supply for the tyre manufacturers.

Now, company's legacy manufacturing capacity of 55,000 tonnes is operating at an optimum level. And hence to meet the incremental demand the company is undergoing multi-phase capacity expansion program (Rs 425 crore) which is expected to double its capacity. The phase 1 (Rs 170 crore) of the expansion is complete which includes two locations – In the Navi Mumbai plant, commercial production started in Q1 FY19 while in Dahej expansion, trial productions started in the quarter gone by.

In the next phase (Rs 255 crore), the company is also focusing on intermediates used for making rubber chemicals. This phase is expected to commission by Oct 2019. Overall capex announced are expected to have asset turnover of 2x i.e. a peak sales potential of ~Rs 850 crore.

OutlookNOCIL is expected to maintain its dominant presence in Indian market on account of its technological leadership and client relationship. It needs to be noted that lengthy process for the product approval (~ 2 years) and the indispensable characteristic imparted by the rubber chemicals ensures a certain level client stickiness.

Further, revenue share contribution from the exports can increase due to focus on specialty products and ongoing trade disruptions.

However, on account of moderation in volume growth in the near term and decline in product prices, we expect a downward adjustment in sales estimates which translates to 18 percent sales CAGR (FY18-21e). We shall revisit this estimates as the demand outlook in auto sector improves. Here it is noteworthy that management expects auto sector slowdown to be short lived – not more than six months.

Operating margins are expected to moderate if the anti-dumping duty is not extended. Taking that into consideration EBITDA margins can contract by 100 bps in FY20e and can possibly settle at around 25-26 percent in the medium term (from 28 percent currently).

Stock is currently trading at around 7.9x FY21e earnings and 4.1x EV/EBITDA for FY21e which seems reasonable. In our view, the stock has already priced in a significant moderation in auto demand outlook. With global and domestic auto demand expected to improve after a couple of quarters, the company looks well positioned to capitalise on that opportunity.

Follow @anubhavsays(Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here.)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.