Jitendra Kumar Gupta Moneycontrol Research

When JSW Energy first announced its intention to get into the electric vehicles business entailing a huge investment, it was completely against market expectations. Particularly so, since the Sajjan Jindal Group had demonstrated good capital allocation decisions in the past.

The market was critical about the foray into electric vehicles which was not its core and not yet fully understood even by the biggest players in this space. The highly technical nature of electric vehicles business and risks of a continued threat of disruptive technologies making it, so far, largely a forte of the developed world.

Prudence over excitement

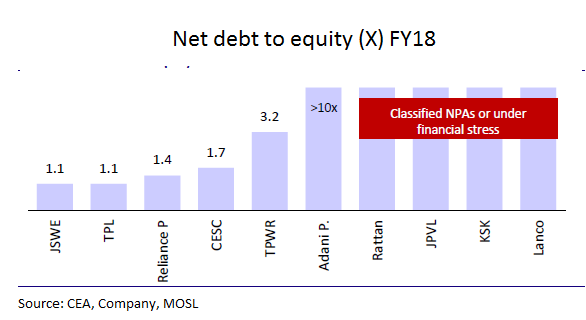

Thankfully, JSW Energy has abandoned this plan. JSW Energy is probably the only company in the sector sitting on cash of about Rs 3,000 crore and a debt-equity ratio of less than one time. It has huge resources at its disposal. Apart from the existing cash in the books which can move up further as a result of expected Rs 5,000 crore of free cash flow from the operation over the next two years, it can raise further debt.

JSW Energy had envisaged an investment of Rs 6,500 crore in the electric vehicle (EV) business. This was a huge investment or close to 30 percent of the capital employed in the business in fiscal 2018. Had this investment gone into EV business, the return on capital, which is already depressed at 3.3 percent in fiscal 2018, would have further plunged because of the long gestation in the new venture.

The company was not only risking the balance sheet, but it was also risking its huge power asset portfolio or core business of power, which it required to strengthen.

Back to core

Particularly in the light of stress in the power sector, this could be the best time to build a formidable business both in terms of scale through the acquisition of stressed assets and securing raw material assets of coal to strengthen its most fragile side of the business.

JSW Energy procures thermal coal of close to about 50% of its requirement from the spot market mainly through imported coal for its thermal power generation capacity of 4500 MW. In the past, spot coal prices have created havocs and impaired profits. Now capital can be used for securing integration, which will make them cost effective in the market particularly when the bulk of company’s sales comes from the merchant power, where the most efficient player make the highest profit.

Second, JSW Energy has built a huge power portfolio through the inorganic route. It was in the process of acquiring Monnet Power, which has 1050 MW of operational capacity supplying power to Monnet Ispat- a company acquired by JSW Steel earlier. Besides, there are many other assets up for sale in the stressed power sector. If the company can successfully grab some of these deals at an IRR of say 18-22 percent (expected IRR in the stressed assets), that would be twice more remunerative than keeping these surplus funds or cash in the banks or treasury.

Impact on valuation

These initiatives will not only ease investors’ concerns about the misallocation of capital but will also show some tangible benefits, which would be critical for its valuation.

As the capital moves into more remunerative activities, the return ratios would shore up, which will entice investors. A day before the announcement to abandon to the EV venture, its stock was trading at Rs 69 share and later spiked to Rs 76.2 a share. Even on April 3, it was trading at about one time its estimated book of about Rs 75 a share in FY20, which is quite cheap.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.