")

- Correction in crude prices to impact oil marketing companies - Heavy inventory losses expected in Q3 FY19 - Growth in gross refining margin to be a tad better than global benchmarks - Remain cautious on the performance of OMCs -------------------------------------------------

Despite expectations of a relatively better performance on the gross refining margins (GRMs) front for domestic oil marketing companies, we expect the Q3 FY19 performance to remain dented owing to the burden of heavy inventory losses due to steep correction in global crude prices.

Growth in GRMs to be higher than global benchmark Weak demand, excess supply and seasonality have led to contracting gasoline cracks. This, coupled with growing scepticism around future crude price and volatility in Brent crude, has led to contraction in benchmark Singapore GRMs by $1.7/bbl during Q3 FY19.

With a lag in fuel price revision due to price calculation based on fortnightly prices in domestic markets, we expect growth in GRMs of domestic OMCs to be tad better than that of the global benchmarks.

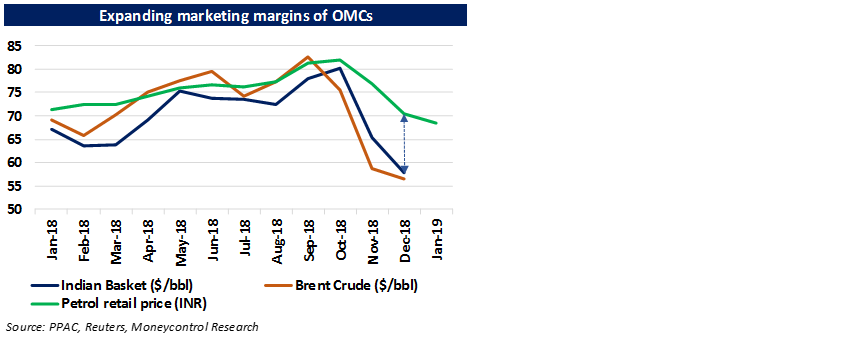

After the Re 1 per litre cut in marketing margin in October last year, global crude prices have seen a steep correction. Though OMCs have stopped reporting gross margins, we believe this correction gave them a cushion to expand their marketing margins, which should have a positive rub off on overall margins for Q3.

The benefit from expanded marketing margin is expected to be the maximum for Hindustan Petroleum Corporation (HPCL), which has almost 61 percent revenue accruing from the marketing business, followed by Bharat Petroleum Corporation (BPCL), with 39 percent marketing revenue, and Indian Oil Corporation (IOCL), with a mere 19 percent marketing revenue.

Inventory losses to eat into profitability While margins are expected to be better than global benchmarks, overall performance is expected to remain sluggish. Crude oil prices have corrected by almost 30 percent since the start of October 2018 to almost $55/barrel towards the end of the quarter. With this steep correction, downstream oil companies are expected to incur heavy losses on account of inventory in the stock. We believe this loss to be quite high during the quarter, which would eat into the quarter’s profitability, though the degree of loss for each company would vary.

Outlook Crude oil prices have been highly volatile in the last quarter and would have an impact on the performance of oil companies.

Appreciation in the rupee during the quarter is expected to bring in some forex gains for OMCs. However, the degree of gains would be something to watch out for. Capacity utilisation and the quantum of inventory loss would be other important parameters which would impact performance.

While companies would enjoy a relief on margins due to the correction in crude oil price, risk arising due to populist measures in the upcoming election period cannot be ruled out. We remain sceptical about the longevity of the current margin expansion in automobile fuels.

Moreover, uptick in crude oil prices owing to the rapidly changing geopolitical landscape and many measures being taken by oil producers to tighten supply could also impact performance.

Reversal of the tax cut in order to provide for the fiscal deficit also remains a concern. We remain cautious on the performance of OMCs given these concerns.

Follow @RuchiagrawalFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.