In a matter of few months two of the topmost brands in the Indian health food drinks (HFD) market have switched owners. Almost sequentially, Complan has been lapped up by Zydus Wellness and now Horlicks has found a new owner – HUL.

Broadly speaking there is a bit of flux in the Indian FMCG space as far repositioning, acquiring or testing beverage space is concerned. Impressions of that can be seen hot beverage segment (Coca Cola – Costa), non-carbonated space (Varun Beverages manufacturing Tropicana) and milk (Tata Sons rejecting M&A proposal for Prabhat Dairy).

As far as Indian health food drinks market is concerned, stagnancy in category growth might now change with HUL pushing for product innovation and premiumisation, advertisement push and strengthening the distribution reach.

What’s the deal?In an all-equity deal, 4.39 shares of HUL are being swapped for every share in GlaxoSmithKline Consumer Healthcare India (GSKCH) bringing the equity valuation at Rs 31,700 crore in line with the current market cap of GSCH. Taking account of cash in the balance sheet, enterprise value is about Rs 28,000 crore and brings the EV/EBITDA at 32x and EV/Sales at 6.5x which is at a premium to Zydus – Heinz deal (4x EV/Sales and 20.4x EV/EBITDA) but broadly inline with other key deals in the Indian FMCG space like Emami’s acquisition of Keshking (6x EV/Sales) and HUL’s acquisition of Indulekha (8x EV/Sales).

Deal transaction is EPS accretive even before accounting for synergy benefits.

The deal brings in the full portfolio of health food drinks - Horlicks, Boost, Viva and Maltova and expected to close by Dec 2019.

Deal also includes a consignment selling contract to distribute OTC products like Sensodyne, Eno, Crocin, and Otrivin for a period of five years.

Post-merger Unilever’s ownership would fall to 61.9 percent (from 67.2 percent) and GSK Plc would hold about 5.7 percent of the merged entity. Unilever doesn’t retain any call option to buy out GSK’s stake in the merged entity.

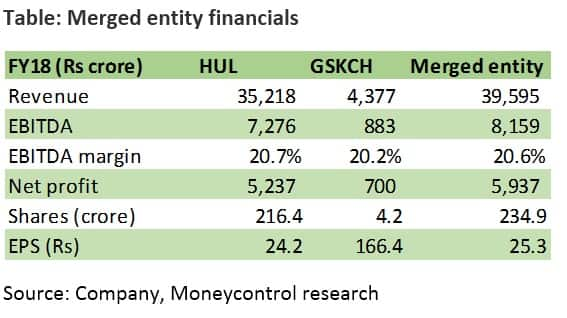

Increases the presence in Foods & Refreshment spaceHUL’s Foods & Refreshment (F&R) division constitutes 19 percent of the net sales and with this merger it scales up to more than Rs 11,000 crore business (28 percent of sales, post-merger).

The segmental margin at present for F&R Indian division is 15 percent which is lower than other divisions - beauty and personal care (26 percent) and home care (18 percent). However, with this merger segmental margins in F&R improve and inch closer to the group level.

Growth in the categoryThough the HFD category and particularly malt-based drinks segment have had a slower growth in last few years, HUL is hopeful of 9 percent CAGR growth (CY17-22e) on account of various levers. Large youth population (37 percent below 19 years), high disposable income and persistent nutritional needs present strong structural demand drivers. Further lower penetration of 22 percent (rural: 14 percent) and specific health needs provides an opportunity for market development.

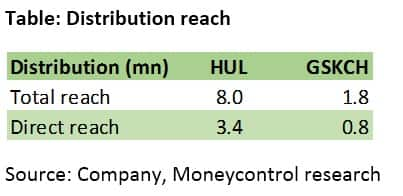

HUL is hopeful of growth acceleration based on wider distribution reach and category’s potential in north and west regions. HUL’s direct reach is more than 4 times than that of GSKCH. Further, GSKCH’s revenue from the north and south region was a mere 6 percent and 5 percent respectively which can change with the company’s innovation and channel placement.

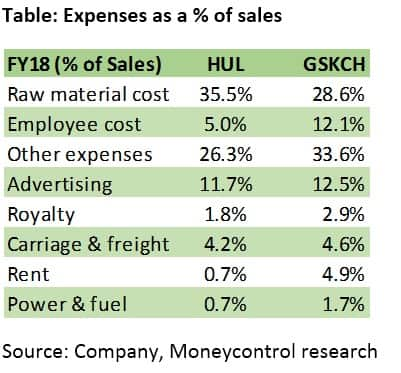

HUL emphasizes full synergy benefits of 800-1,000 bps to the margins on account of cost efficiencies and premiumisation. Innovations thereby competing with the likes of Pediasure (Abbot) and Protinex (Danone) can be expected. Further, there seems to be a lot of scope for cost rationalisation particularly for heads like employee cost, rent, and utilities. Scale benefits are expected to kick in with regards to advertising and promotional cost and raw material sourcing. Similarly overlap in distribution and logistics can be reduced.

However, HUL has to continue paying royalty on Horlicks which is about 2.9 percent of GSKCH sales and to that extent other expenses would remain higher.

HUL is likely to have tax benefit on account of goodwill treatment. This transaction would help HUL record goodwill on the books which can be amortised. For GSK, share swap structure helps in lowering of taxation burden compared to outright cash deal which would have been subjected to huge LTCG tax.

Overall, we find this deal transaction earning accretive and believe that synergy benefits are worth watching out for. However, a lot comes on HUL’s shoulder not only in terms of bringing synergy benefits but also in terms of category innovation. And therefore there is an element of execution risk.

With this transaction, HUL’s urban exposure has increased for the time being. Taking account of synergy benefit of 300 bps on the margins for the HFD category in the FY21, the stock is currently trading at 47.6x the FY21e earnings.

For more research articles, visit our Moneycontrol Research page.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.