Anubhav SahuMoneycontrol research

In recent times, health food drinks (HFD) category has been garnering attention owing to F&B companies' push for healthier beverage variants and the Kraft Heinz and GSK exit announcements.

Zydus Wellness acquisition of subsidiary of Kraft Heinz's Indian unit is a follow through on that. Let us look at the deal implications and valuation.

What’s on offer?

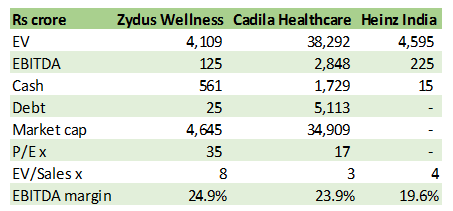

Zydus Wellness, jointly with Cadila Healthcare (72 percent shareholder of Zydus Wellness), will acquire Heinz India at a valuation of Rs 4,595 crore. The transaction is expected to close in Q4 FY19, and brings brands like Complan, Glucon D, Nycil and Sampriti Ghee to the Zydus table.

The acquisition enhances the consumer/health nutrition portfolio for Zydus Wellness (80 percent of the combined entity) and Cadila Healthcare (12 percent from 6 percent). Heinz India brings with it network of 800 distributors and 20,000 wholesalers and hence doubles the Zydus reach (currently 1000+ distributors). Further, few of the products are expected to emerge as brand/product extension like butter (Nutralite/Sampriti Ghee) and skincare (Everyuth/Nycil) categories.

Acquisition Valuation

Given the Heinz India valuation of Rs 4,595 crore, target multiple comes out to be 4x EV/Sales and 20.4x EV/EBITDA. This is lower than other similar deals in consumption space like that of Emami’s acquisition of Keshking (6x EV/Sales) and HUL’s acquisition of Indulekha (8x EV/Sales). Interestingly, this deal transaction is also inexpensive compared to the trading multiple of its nearest peer, post deal, GlaxoSmithKline (GSK) Consumer Healthcare (6x EV/Sales and 30x EV/EBITDA).

Acquisition not margin accretive in near term

Heinz India’s operating margin have been in the vicinity of nearest competitor GSK Consumer Healthcare of about 20 percent. However, this is way below the operating metric for both Zydus Wellness and Cadila Healthcare (24-25 percent).

Cost synergy benefits are not apparent in the near term as there is little overlap in terms of distribution coverage. Initially, Zydus wants to operate the acquired entity as an independent company. However, gradually company expects synergy in terms of raw material, logistics and reach.

Table: Company financials (Rs cr)

Source: Company, Moneycontrol Research

EPS accretive deal depends on structuring

The M&A transaction can be EPS accretive provided there is higher private equity or third party participation. While Zydus Wellness would utilize cash reserve available in the balance sheet, newsflow suggest parent (Cadila Healthcare) would also infuse about Rs 1,000 crore.

Source: Company, Moneycontrol Research

Assuming private equity participation is slightly lower than 50 percent, one of the likely deal structure could be as above. While this structure is EPS accretive, it also leads to debt of Rs 800 crore and implied Debt/Equity ratio for Zydus Wellness would then increase to ~1.15 (from nil). However, this may lead to limited management control posing difficulty for synergy benefits.

Further, our back of the envelope calculation suggest that private equity participation at lower levels, say 25 percent, would be EPS dilutive given the heavy interest burden in that case.

So while this M&A transaction opens an interesting consumption space for Zydus Wellness wherein brands in question have sizeable market share, occupy a perceptible consumer mindshare and offer product extension and reach, apparent stress on the balance sheets of the acquirer doesn’t augur well, in our view.

Additionally, Zydus Wellness has to work on growth challenges in HFD segment which has witnessed slowdown in recent times. Sales of Heinz India, in particular, has slowed in last couple of years. This means new entity has to channelise innovation and reach to catch the running theme of consumer shift towards healthier beverage option.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.