Goa Carbon, the second largest manufacturer of calcined petroleum coke (CPC) in India, posted another weak quarter due to lack of access to imported raw materials.

Key negatives

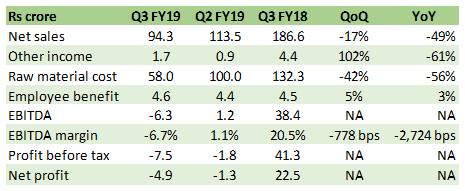

Source: Company

Sales contracted 17 percent sequentially as limited raw material availability led to plant shutdowns (Goa plant - 55 days, Bilaspur plant - 66 days and Paradeep plant - 61 days). Weak operating performance was much anticipated due to impact of interim ban on petcoke import by Supreme Court (SC), leading to lower capacity utilisation (35 percent in Q3). Further, negative operating leverage had an adverse impact on profitability.

Gestation period in import resumption: While the SC ban on petcoke import was enforced from July 26 to October 9, 2018, new import licenses could get functional after a significant delay. The company could import raw material under the new licensing set-up only in the last days of December.

Key positiveQ4 quarter to see almost full utilisation: After the recent raw material mobilisation, operations are in full swing. It is sitting on a sale order of 50,000 tonne and hopeful of capacity utilisation of 96 percent in Q4. End-market demand, particularly in the aluminium industry (80 percent of sales) remains intact.

Key observation However, recent price correction in aluminium (about 10 percent in the last quarter) doesn’t augur well for CPC prices. Price negotiations with smelters suggest some correction in the negotiated CPC prices. At the same time, input cost (raw petcoke) has not declined as much. On account of this, margin pressure are expected to remain in the near term.

Outlook The management is hopeful of clocking Rs 500 crore revenue in FY19, which implies a similar quarterly run-rate in performance for Q4 FY19, as was seen H2 FY18. Goa Carbon’s Q3 result has mixed implications for Rain Industries. The latter is not expected to post encouraging December quarter results, particularly in the CPC business. However, we expect volume recovery for it in coming quarters.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.