Sun Pharmaceutical Industries is expected to deliver a largely steady Q3FY26 performance, with brokerages pencilling in mid-single-digit revenue growth, stable margins and a muted earnings trajectory, as incremental gains from the domestic and specialty businesses are partially offset by a flattish US generics outlook. While there are no major positive surprises expected this quarter, analysts remain watchful of specialty traction, US pricing behaviour and the trajectory of R&D spends as the company heads into FY27.

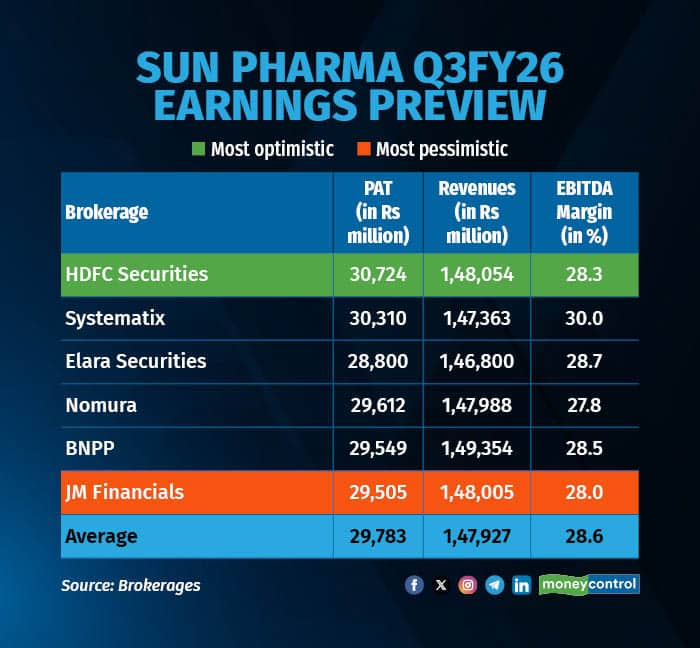

A Moneycontrol analysis of brokerage previews, estimates for Q3FY26 point to revenues in a narrow band of Rs 146,800 to 149,400 million, underscoring the absence of sharp growth triggers in the quarter. EBITDA margins are expected to hold within the 28 to 30% range, supported by cost discipline and India mix, but capped by ongoing investments in specialty and R&D.

Adjusted net profit is seen clustering around Rs 29,000 to 30,700 million, suggesting earnings growth will largely mirror operating performance rather than benefit from one-off factors.

Sun Pharma Q3FY26 Earnings Preview

Sun Pharma Q3FY26 Earnings Preview

The tight convergence across estimates indicates broad agreement on the quarter’s underlying stability, with limited upside or downside risk priced in.

India business remains the key support

Most brokerages continue to flag India formulations as the most consistent growth driver, aided by price increases, chronic therapy traction and steady prescription momentum. The domestic business is expected to deliver low-double-digit year-on-year growth, helping cushion softer trends in overseas markets and anchoring margins.

US generics: steady volumes, pricing still a headwind

In the US, analysts expect largely stable revenues sequentially, with new launches and volume traction offset by persistent pricing pressure. While competitive intensity has eased compared to previous years, brokerages see limited scope for near-term pricing recovery, keeping the US business from becoming a meaningful growth catalyst in the quarter.

Specialty portfolio: progress, but near-term drag persists

Sun Pharma’s specialty portfolio remains a key medium-term focus, but brokerages are cautious on its immediate earnings impact. While sales traction is improving gradually, higher spending on marketing and R&D continues to weigh on profitability, limiting margin expansion in the near term. Analysts will watch for signs of operating leverage and clearer timelines for specialty profitability.

Margins likely to stay range-bound

EBITDA margins are expected to remain broadly flat at 28 to 30%, supported by domestic mix and operational efficiencies. However, the lack of strong US pricing tailwinds and continued specialty investments mean material margin expansion is unlikely in Q3.

What to watch for

Beyond the numbers, investors are likely to track management’s outlook on:

Valuation comfort, but limited near-term triggers

Brokerages continue to ascribe a premium valuation to Sun Pharma, reflecting its scale, balance sheet strength and long-term specialty optionality. However, with earnings growth expected to remain measured in the near term, analysts see limited scope for re-rating without sharper specialty upside or a US pricing inflection.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.