The market corrected sharply after a week of moderate gains, plunging more than 1.5 percent in the week ended February 27 as risk-off sentiment prevailed amid renewed tariff uncertainty, concerns over AI-led disruption, and caution ahead of US–Iran tensions. Initial support from the US Supreme Court’s ruling against Trump’s reciprocal tariff policy completely faded as the week progressed.

Over the weekend, the situation in Iran turned more serious as the United States and Israel jointly launched a massive attack on Iran, including its capital, Tehran, heightening fears of supply disruptions, a spike in oil prices, rising inflation, and pressure on earnings and growth. The killing of Iran's Supreme Leader, Ayatollah Ali Khamenei, in the attack further intensified Middle East tensions. According to experts, a full-blown war is unlikely, though Iran responded by launching strikes in several cities across the Middle East.

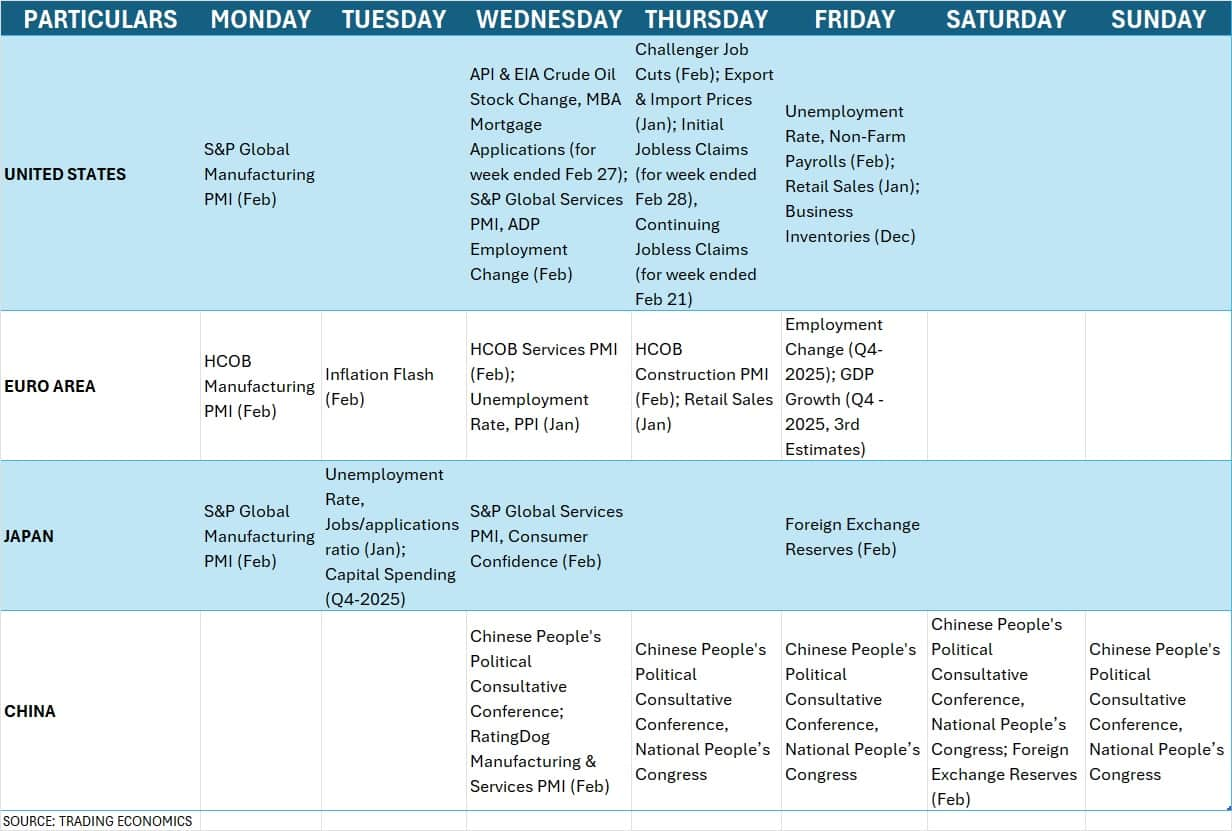

On Monday, the market is expected to see a gap-down opening following the Middle East tensions, while auto stocks will react to the February numbers announced on March 1. In the truncated week ahead, selling pressure may widen only if there are major oil and gas supply concerns, as that would increase trade costs and impact inflation and the fiscal deficit. Until then, there could be consolidation with range-bound trading after the initial reaction in the early part of the week, experts said. They added that the focus will also be on China’s Two Sessions meetings, manufacturing and services PMI data, US jobs numbers, and currency movements.

The Nifty 50 plunged 393 points (1.54 percent) during the week to close at 25,179, and the BSE Sensex slipped 1,528 points (1.84 percent) to 81,287. Meanwhile, the Nifty Midcap 100 and Smallcap 100 indices were down 0.67 percent and 0.43 percent, respectively.

On a monthly basis, the benchmark indices corrected for the third consecutive month, with the BSE Sensex declining 1.2 percent and the Nifty falling 0.56 percent.

“Indian equity markets have already responded with risk-off sentiment. Benchmark indices are expected to open lower, accompanied by heightened volatility as investors reassess geopolitical and commodity-related risks,” said Manoranjan Sharma, Chief Economist at Infomerics Ratings.

According to him, a short-term market correction of approximately 1–1.5 percent is possible, along with broader market reactions such as potential capital outflows and depreciation pressure on the rupee. Sectors such as automobiles, financials, and FMCG may face downward pressure. In contrast, IT companies and select export-oriented businesses may find relative support amid global risk aversion and a strengthening US dollar.

Energy-intensive industries, including aviation, logistics, paints, and chemicals, are likely to experience margin compression due to rising input costs, while upstream oil producers could benefit from higher crude prices.

“If the conflict persists without swift de-escalation, India’s fiscal outlook may face further strain from higher subsidy commitments, subdued disinvestment valuations, and the possibility of expanded social spending to cushion domestic economic pressures,” Manoranjan said.

Apart from US–Iran tensions, Vinod Nair, Head of Research at Geojit Investments, said ongoing AI-related uncertainty continues to support safe-haven flows. “Domestically, a risk-off tone prevails as the earnings season tapers and global macro factors take precedence. With FII flows remaining cautious and volatility likely to persist, markets are expected to maintain a consolidation range.”

The market will remain shut on March 3 for Holi.

Here are 10 key factors to watch this week:

US-Iran War

The most important global factor to focus on is the ongoing war between the United States and Iran, as markets are worried about oil and gas supply and its impact on prices and inflation, particularly for major importers like India. Concerns about the potential impact on corporate earnings and the fiscal deficit will also be closely monitored, while oil and gas-related stocks may see significant action.

The US and Israel launched a massive attack on Iran, including its capital, Tehran, on February 28, especially after Iran remained reluctant to meet US demands to scale down its nuclear program. If the situation persists for long, it could ultimately impact global growth.

Hundreds of people have reportedly been killed in the attacks so far. Several flights to Middle East destinations, including Dubai, Doha, and Tel Aviv, have been cancelled, leaving many passengers stranded at airports. Fresh evacuation warnings have also been issued by China and the United States Department of State, urging their citizens to leave Iran and Israel, thereby heightening geopolitical risks across global markets. India has also asked its citizens to leave Iran.

Later, Iranian media confirmed that Ayatollah Ali Khamenei, Iran’s Supreme Leader, was killed in the attack, intensifying the possibility of retaliation by Iran.

The biggest concern for energy sector traders is the Strait of Hormuz, the waterway through which around 20 million barrels of oil flow per day.

The strait is the world’s most vital oil export route, connecting major Gulf oil producers such as Saudi Arabia, Iran, Iraq, and the United Arab Emirates with the Gulf of Oman and the Arabian Sea. Several tanker owners, oil majors, and trading houses have suspended shipments of crude oil, fuel, and liquefied natural gas via the Strait of Hormuz after the US and Israel attacked Iran and Tehran announced the closure of navigation, Reuters reported, quoting sources.

If there is any major disruption in the Strait of Hormuz route, considering the quantum of daily flow, oil prices may spike further. In fact, trade costs for oil and gas may increase for countries like India, which is among the largest oil importers. Experts, however, have ruled out a full-blown war-like situation.

Oil Prices

Brent crude futures, the international oil benchmark, rallied 1.55 percent during the week to $72.87 per barrel, the highest level since July 2025, amid rising US-Iran tensions. Prices have increased by around $12–13 per barrel since the start of this year. They have already surpassed the 20-, 50-, and 100-week EMAs and are moving closer to the 200-week EMA, with short- and medium-term moving averages trending upward, signaling rising bullish momentum.

“Although the prospect of a prolonged, full-scale war remains uncertain, the situation is currently marked by fragile ceasefire efforts amid persistent strategic tensions,” Manoranjan Sharma, Chief Economist at Infomerics Ratings, said.

Oil prices when markets open on March 2 will also reflect the outcome of the OPEC+ discussions held on March 1. According to Bloomberg, quoting delegates, OPEC+ agreed in principle to a slightly larger increase in oil production next month. Key members led by Saudi Arabia and Russia — which had paused a series of hikes during the first quarter — will add 206,000 barrels per day.

“Geopolitics will remain the dominant theme, as tensions that had been simmering for months escalated over the weekend following US–Israel strikes across Iran. Tehran has previously vowed a ‘decisive’ response if military options are pursued, raising the risk of a wider regional conflict,” Kaynat Chainwala of Kotak Securities said.

Global Economic Data

Apart from US-Iran tensions, the market participants will also focus on speeches from Federal Reserve officials, final PMI readings from major economies, US jobless claims, retail sales, and, most importantly, the official US employment report.

"Hotter inflation data have added to headwinds that could delay the Fed’s easing cycle. If labour market conditions remain robust, expectations for a June rate cut may fade further. Conversely, a weaker jobs report could prompt markets to recalibrate rate expectations," Kaynat said.

China's Two Sessions

Markets will also keep an eye on the China’s annual “Two Sessions” meetings from March 4–11, where the 15th Five-Year Plan (2026–2030) is expected to be unveiled. The plan is likely to set a lower growth target in the 4.5–5 percent range for 2026, compared with around 5 percent last year, alongside a moderately expansionary fiscal stance with the deficit ratio seen steady at 4 percent of GDP.

Domestic Economic Data

Back home, the market participants will focus on HSBC Manufacturing PMI numbers for February, and industrial production for January releasing on March 2, followed by HSBC Services PMI due on March 4.

According to the preliminary estimates, manufacturing PMI increased to 57.5 in February from 55.4 in the previous month, signalling healthy factory activity expansion, while the services PMI dropped moderately to 58.4 from 58.5, but is still a strong expansion in services activity in the same period.

Bank and deposit loan growth for the fortnight ended February 20, and foreign exchange reserves for the week ended February 27 will also be watched this week, due on March 6.

The focus will also be on the Foreign Institutional Investors (FIIs) activity as the flow has improved in the current month, given the improving earnings growth and healthy GDP numbers but the global concerns, including geopolitical tensions between the US and Iran, may force them to reassess the call on emerging markets or wait and watch before getting signals of stability in the war.

FIIs have net sold more than Rs 4,600 crore in equities but were fully absorbed by Domestic Institutional Investors (DIIs) who picked up shares worth over Rs 24,300 crore in the week passing by. The data was also very similar in February, as the net selling by FIIs for the month was over Rs 6,600 crore, which, however, fully compensated by DIIs who net bought more than Rs 38,000 crore worth shares.

Meanwhile, the market participants will also watch the impact of Middle East concerns on the currency. The Indian rupee depreciated 0.38 percent to 91.03 against the US dollar amid high volumes, extending for another week.

The US dollar index held above 97.5 for the second consecutive week as resilient data reinforced expectations that interest rates will stay higher for longer. Overall, it remained below all moving averages since the mid of January 2026.

The activity at the primary market is set to slow down in the coming week as only three IPOs will hit Dalal Street, including only one - SEDEMAC Mechatronics - from the mainboard segment. The Pune-based technology company that makes control-intensive products for the automotive and genset segments will open its Rs 1,087-crore initial public offering (IPO) for subscription on March 4 and 6, with price band of Rs 1,287-1,352 per share.

In the SME segment, Elfin Agro India will open its Rs 25-crore IPO on March 5, followed by Srinibas Pradhan Constructions' Rs 20-crore public issue scheduled on March 6, while Striders Impex will close its Rs 36-crore offer on March 2, and Acetech E-Commerce issue on March 4.

Meanwhile, there will be nine companies making their market debut this week. Of which, five firms - Clean Max Enviro Energy Solutions, Shree Ram Twistex, Kiaasa Retail, Mobilise App Lab, and Accord Transformer & Switchgear - will be available for trading on the bourses on March 2. This follows PNGS Reva Diamond Jewellery scheduled for listing on March 4. Further, the trading in Omnitech Engineering and Yaap Digital shares will commence on March 5, while Striders Impex will debut on March 6.

Technical View

Technically, not only the psychological 25,000 zone but also the upward sloping support trendline (24,850) may be at the risk this week, as falling below which levels can add more strength to bears who can drive the Nifty 50 down to Union Budget day's low of 24,571. On the daily charts, the index has already fallen below all key moving averages as well as rising support trendline, while the momentum indicators signalled sell call on the daily as well as weekly timeframes. In case of rebound during the coming week, the 25,350-25,500 are the levels to watch as sustaining above it can open door for 25,600-25,700, the crucial hurdles for sharp upmove thereafter.

F&O Cues, India VIX

The weekly options data also indicated that the 25,000 is expected to be immediate crucial support for the Nifty 50, however, the 25,300-25,500 are the immediate resistance zones to watch.

The maximum Put open interest was placed at the 25,000 strike, followed by the 24,500 and 25,200 strikes, with the maximum Put writing at the 25,100, 25,150, and 24,500 strikes. On the Call side, the 25,500 strike holds the maximum open interest, followed by the 25,400 and 25,600 strikes, with the maximum Call writing at the 25,400, 25,300 and 25,350 strikes.

Meanwhile, the India VIX, also known as fear gauge, remained at the elevated levels despite 4.6 percent correction during the last week, closing at 13.7, signalling the risk for bulls. It decisively needs to fall below 12 zone for the bulls to get into comfort zone.

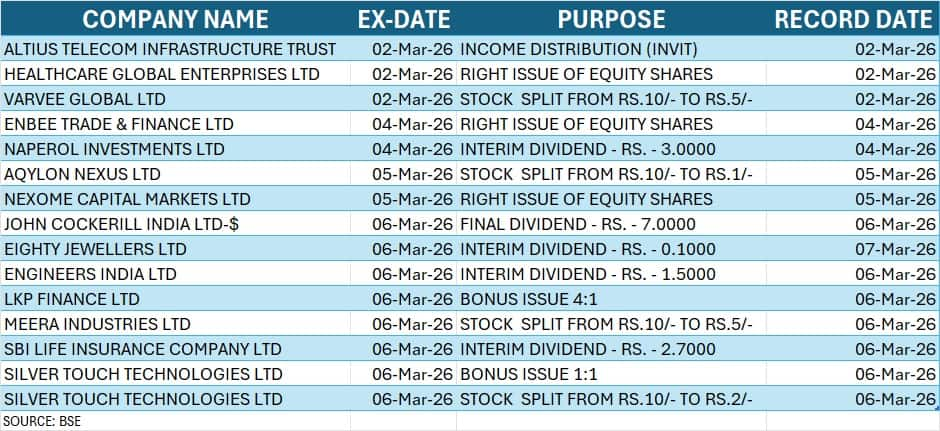

Corporate Action

Here are key corporate actions taking place in the coming week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.