The market sharply rebounded 3.5 percent during the week ended February 6, supported by above-average volumes, after recouping losses from the previous two weeks. Much of the credit goes to the US–India trade deal announced by President Donald Trump on Monday night, followed by the interim trade agreement and Trump’s executive order removing the additional 25 percent tariff on Indian goods imposed over Russian oil imports over the weekend.

The Union Budget presented on February 1 did not materially shift market sentiment, while the RBI’s upward revision of GDP forecasts for FY26, combined with a steady inflation outlook, reinforced confidence in the medium-term domestic economic trajectory.

FII inflows also supported the market; however, rising oil prices signalled caution. The technology sector was the biggest loser following Anthropic’s launch of a sophisticated legal-focused AI tool, with the index falling nearly 7 percent, which capped the broader market’s upside.

In the current week starting February 9, the market is expected to first react to the interim trade agreement disclosed by the US and India through a joint statement, along with the removal of additional tariffs on Indian goods. Overall, the trend is likely to remain positive, albeit with possible range-bound trading following the easing of trade deal concerns. The focus will be on the final set of corporate earnings, inflation data from the US, India, and China, and US jobs data, experts said.

The Nifty 50 rallied 868 points (3.5 percent) during the week to close at 25,694, while the BSE Sensex surged 2,857 points (3.54 percent) to 83,580. Meanwhile, the Nifty Midcap 100 and Smallcap 100 indices jumped 4.2 percent and 3.2 percent, respectively.

“Overall, markets may remain range-bound in the near term, with stock-specific action driven by earnings outcomes and lingering global uncertainties,” said Siddhartha Khemka, Head of Research, Wealth Management, at Motilal Oswal Financial Services.

He added that attention will shift to upcoming US economic data and commentary from Federal Reserve officials for further cues on the global macro environment and the interest-rate trajectory.

According to Vinod Nair, Head of Research at Geojit Investments, despite these positives, sentiment in the near term is expected to remain cautious due to Q3 earnings that broadly trailed expectations, as well as rising crude oil prices amid escalating US–Iran tensions.

Here are 10 key factors to watch this week:

India-US Interim Trade Agreement

The market participants are expected to react to the details of the interim trade agreement announced by both countries through the issuance of joint statement on February 7 and passing of executive order by Donald Trump removing additional 25 percent penalty imposed on India for Russian oil imports. After this, the India is having either at par or below tariff rate compared to other Asian and emerging market counterparts.

Several sectors like pharma, gems and diamonds, smartphones, and select agricultural products, tea, coffee, and fruits will have zero reciprocal tariffs in the United States, while the country managed to safeguard agriculture and daily segments though there is a limited access for US agricultural products.

Corporate Earnings

The market will see the final lot of December quarter earnings this week as more than 1,900 companies will release their quarterly earnings during the current week including the Nifty 50 names like Apollo Hospitals Enterprise, Eicher Motors, Grasim Industries, Titan Company, Mahindra & Mahindra, Coal India, Hindustan Unilever, and Oil and Natural Gas Corporation.

Among others, Hindalco Industries, Britannia Industries, Zydus Lifesciences, Aurobindo Pharma , LG Electronics India, Amber Enterprises India, Sun Pharma Advanced Research Company, Escorts Kubota, Jubilant FoodWorks, Karnataka Bank, Oil India, Torrent Power, United Breweries, Wakefit Innovations, Ashok Leyland, CARE Ratings, Divis Laboratories, Bharat Forge, Biocon, Hindustan Aeronautics, Honasa Consumer, Indian Hotels Company, Indian Railway Catering and Tourism Corporation, Lupin, Shadowfax Technologies, Zaggle Prepaid Ocean Services, Brainbees Solutions Firstcry, Ipca Laboratories., IRB Infrastructure Developers. and Torrent Pharmaceuticals will alos announce their quarterly numbers this week.

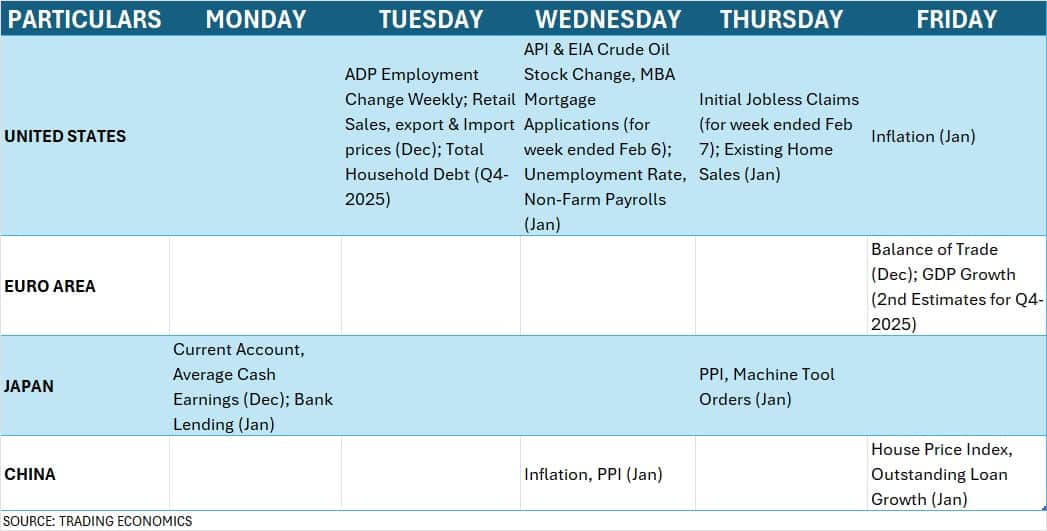

Domestic Economic Data

The focus will be on the inflation numbers for the month of January 2026, which is one of the crucial factors for the RBI before taking interest rate decision. The consumer price inflation climbed to 1.33 percent in December last year, from 0.71 percent in previous month. Most economists see some further uptick in the numbers.

Apart from inflation, bank loan and deposit growth for fortnight ended January 23, and the foreign exchange reserves for week ended February 6 will also be released this week on February 13.

US Inflation, Unemployment Rate

Globally, investors will keep an eye on the US inflation numbers, unemployment rate, and non-farm payrolls for January. Most economists expect the inflation to fall in January, from 2.7 percent in December, while the unemployment rate is expected to be steady at 4.4 percent.

"Following a string of labour market reports that largely surprised to the downside, attention now turns to the official non-farm payrolls report due February 11 as significant downward revisions could strengthen the case for future rate cuts," Kaynat Chainwala of Kotak Securities said. Retail sales data, and speeches from several Fed officials will also be closely monitored.

Global Economic Data

China will also announce its inflation and PPI data for January, while the Europe will release its second estimates for GDP growth of Q4CY25 this week.

Back home, the mood of FIIs (foreign institutional investors) will be watched as they finally turned net buyers in Indian equities after a long time, thanks to the Donald Trump who agreed to reduce tariff on Indian goods to 18 percent from 50 percent, and appreciation of rupee against US dollar. "Rupee is expected to stabilise and gradually appreciate to below 90 to the dollar by end March 2026. This has the potential to trigger more FII inflows into India. However, a lot will depend on how the AI trade pans out," VK Vijayakumar, Chief Investment Strategist at Geojit Investments said.

FIIs have net bought Rs 3,234 crore worth shares during the week and Rs 2,645.5 crore for current month, while DIIs (domestic institutional investors) picked up shares amounting to Rs 2,892 crore in February so far.

Meanwhile, the Indian rupee appreciated by 1.19 percent during the week to 90.56 against the US dollar and seems to have formed Evening Star kind of candlestick pattern on the weekly charts which needs to be confirmed in the followed week, signalling potential positive trend reversal.

Investors will see three new public issues worth Rs 3,871-crore this week with Fractal Analytics, and Aye Finance being the first opening for subscription on February 9 with price band of Rs 857-900 per share, and Rs 122-129 apiece, respectively.

Pure AI company Fractal Analytics is raising Rs 2,834 crore at the upper price, band, while Alphabet, and LGT Capital-backed NBFC Aye Finance aims to mop up its Rs 1,010-crore via initial share sale.

Marushika Technology will be last IPO amongst them, which is from the SME segment. The IT and telecom infrastructure solutions provider intends to raise Rs 26.97 crore via public issue of 23.05 lakh shares at the upper price band of Rs 111-117 per share. Further, Biopol Chemicals, and PAN HR Solutions will close their public issues on February 10.

Four companies are scheduled for market debut this week - Brandman Retail, Grover Jewells, Biopol Chemicals, and PAN HR Solutions.

Technical View

Technically, the trend remains favourable for bulls with the Nifty 50 trading above all key moving averages, and consistently holding the long bullish gap (of February 3) on closing basis with supportive momentum indicators. Hence, the 25,800-26,000 is expected to be crucial resistance for the Nifty 50 as decisive move above it drive the index toward 26,200-26,400 levels, however, the crucial support is placed at the 25,500.

F&O Cues

The weekly options data suggested that the Nifty 50 is expected to the 25,500-26,000 range in the short term as convincing trade either of the side can give firm direction to the index. The maximum Call open interest was seen at the 26,000 strike, followed by the 25,800 and 26,500 strikes. with the maximum Call writing at the 25,600, 25,950 and 26,300 strikes.

On the Put side, the 25,500 strike holds the maximum Put open interest, followed by the 25,000 and 25,600 strikes with the maximum Put writing placed at the 25,500, 25,600 and 25,550 strikes.

Meanwhile, the India VIX, which measures expected market volatility, plunged 20.9 percent during the last week to finish at 11.94, giving comfort for bulls and signalling low uncertainty in the market.

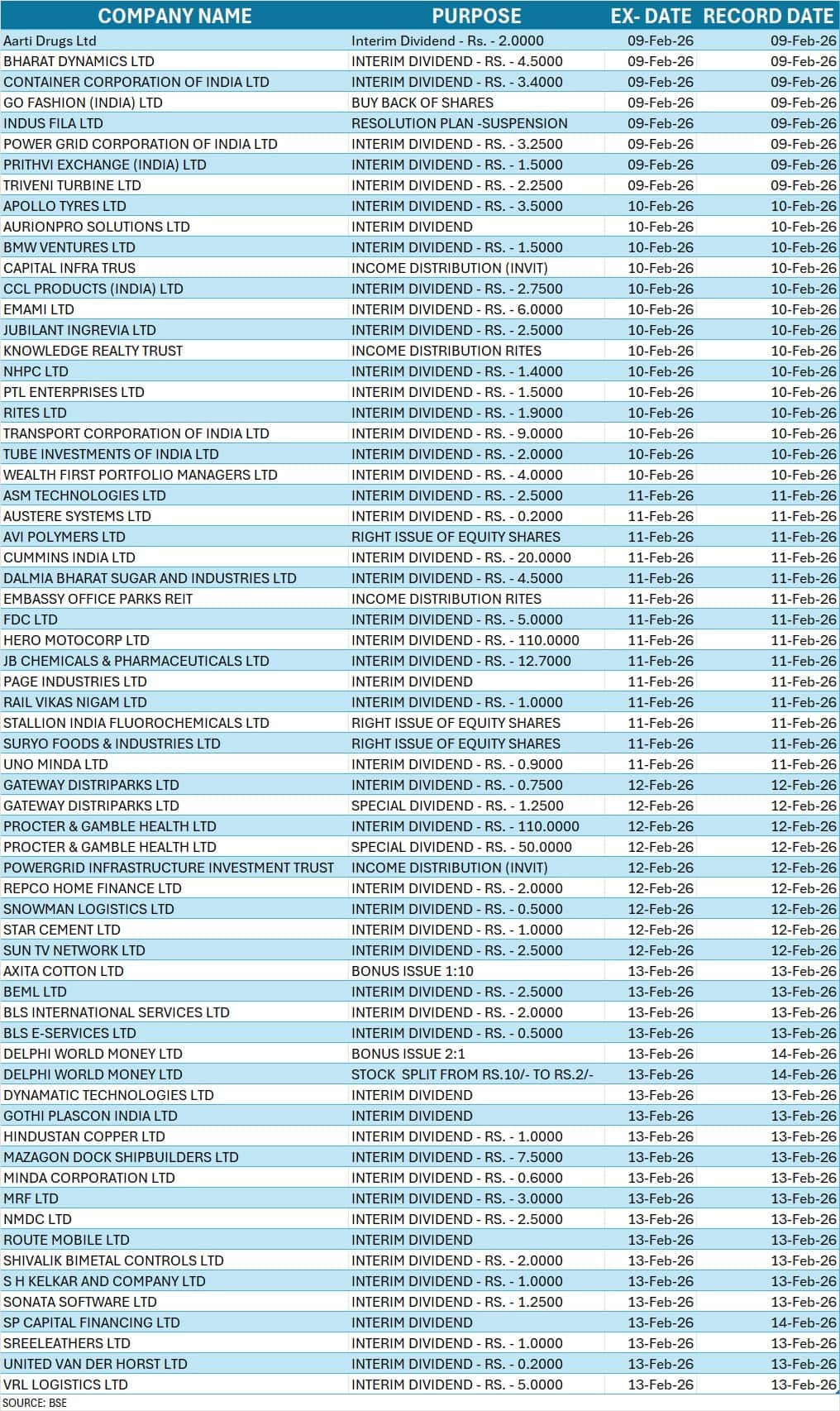

Corporate Action

Here are key corporate actions taking place in the current week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.