The market wiped out all its previous week's gains and closed 2.45 percent down for the week ended January 9, as global headwinds, including the Venezuela-US standoff, concerns over Russian oil imports, China’s restrictions on rare earth exports, and continued FII outflows dampened sentiment, though there was support from strong GST collections, healthy bank credit growth and subdued oil prices.

In the current week starting from January 12, the market is expected to consolidate with a focus on corporate earnings (as index heavyweights are releasing their numbers), India and US inflation, FIIs' mood, Trump tariffs, and expectations from the Union Budget 2026.

The Nifty 50 plunged 645 points (2.45 percent) during the week to close at 25,683, and the BSE Sensex tanked 2,186 points (2.55 percent) to 83,576, while the broader markets also saw severe selling pressure with the Nifty Midcap and Smallcap 100 indices falling 2.6 percent and 3.08 percent, respectively.

Overall, "markets are expected to stay range-bound with a mixed bias, looking forth a balance between external risks and domestic fundamentals," Vinod Nair, Head of Research at Geojit Investments, said, adding that clarity on global trade dynamics and Q3 earnings will shape market direction.

According to him, volatility is likely to persist in the near term, particularly in US-exposed companies and sectors such as metals and oil & gas. However, strong domestic fundamentals, resilient GDP growth, and robust credit trends could underpin selective buying where earnings prospects remain favourable, he said.

Siddhartha Khemka - Head of Research, Wealth Management at Motilal Oswal Financial Services, also said the Q3 result season and expectations around the Union Budget 2026 would be the key market drivers this week.

Here are 10 key factors to watch this week:

The much-awaited December quarter earnings season (Q3FY26) will be in full swing this week, with top IT companies (Tata Consultancy Services, Infosys, HCL Technologies, Tech Mahindra, Wipro), leading private banks (HDFC Bank and ICICI Bank), index heavyweight Reliance Industries, and other Nifty 50 names like HDFC Life Insurance Company and Jio Financial Services, among 120 companies releasing their quarterly scorecard.

Among others, HDFC Asset Management Company, HDB Financial Services, ICICI Lombard General Insurance Company, ICICI Prudential Life Insurance Company, ICICI Prudential Asset Management Company, Billionbrains Garage Ventures (Groww), Anand Rathi Wealth, Bank of Maharashtra, Tata Elxsi, Union Bank of India, Angel One, Emmvee Photovoltaic Power, L&T Technology Services, Federal Bank, JSW Infrastructure, L&T Finance, Polycab India, Poonawalla Fincorp, Tata Technologies, and Yes Bank will also announce their numbers this week.

Experts expect the continuation of earnings recovery in Q3FY26.

India Inflation

On the domestic economic data front, the market participants will focus on inflation numbers for December, scheduled on January 12, followed by WPI inflation on January 14, and balance of trade and unemployment rate on January 15, while foreign exchange reserves for the week ended January 9 will be released on Friday.

According to most economists, the CPI inflation is expected to climb close to 1.5 percent for December 2025 against 0.71 percent seen in November.

US Inflation

Globally, the focus will be on the US inflation numbers, which is one of the crucial factors for the US Federal Reserve to take its interest rate decision. Most economists see inflation rising to around 2.7 percent for December against 2.6 percent in November 2025.

Further, weekly jobs data, monthly new home sales, retail sales, and PPI numbers will also be watched.

Global Economic Data

Apart from the US, several data points, monthly industrial production and balance of trade data from Europe, PPI numbers from Japan, and vehicle sales and balance of trade for December from China will also be watched this week.

The market participants will also check the FII activity as they remained net sellers for the last week amid geopolitical tensions and renewed tariff concerns, though DIIs consistently compensated FIIs' outflow.

Foreign Institutional Investors (FIIs) have net sold Rs 8,808 crore worth shares in the week ended January 9; however, Domestic Institutional Investors (DIIs) have net bought shares worth Rs 15,700 crore in the week.

Meanwhile, the Indian rupee continued to weaken for the fourth consecutive week, depreciating 0.02 percent for the last week to 90.23 levels, while the US dollar index fell 0.2 percent to 98.94 but sustained above short-term moving averages.

A total of six companies are set to launch their IPOs worth more than Rs 2,000 crore this week, with five firms making market debut in the same period. Out of the six names, Bengaluru-based SaaS company Amagi Media Labs will be the only IPO from the mainboard segment, while others are from the SME segment.

Amagi Media Labs will open its Rs 1,789-crore IPO for public subscription on January 13 with a price band of Rs 343-361 per share, while SME IPOs - Avana Electrosystems, and Narmadesh Brass Industries will open their public issues on January 12, followed by Indo SMC, and GRE Renew Enertech on January 13. Armour Security India will be the last IPO, opening on January 14.

Bharat Coking Coal, a part of Coal India, will close its Rs 1,071-crore initial share sale on January 13, while Defrail Technologies, a part of the SME segment, will also close its maiden public issue on January 13.

Meanwhile, Bharat Coking Coal will list its equity shares on the bourses on January 16, while in the SME segment, Gabion Technologies India shares will be available for trading effective January 13, Victory Electric Vehicles International, and Yajur Fibres on January 14, and Defrail Technologies on January 16.

Technical View

Technically, with the formation of a long bear candle, the Nifty 50 turned weak, falling not only below the 10-week EMA but also breaking the upward sloping support trendline during the week. Further, the index tested the 20-week EMA and reached closer to the midline of the Bollinger bands. Hence, if the index decisively breaks last week's low of 25,623, the fall toward 25,500-25,400 can't be ruled out; however, on the higher side, the 25,950-26,000 is expected to act as a resistance zone as decisive trade above it can resume buying interest, experts said.

F&O Cues

The weekly options data indicated that the Nifty 50 is expected to face resistance at 26,000 with support at the 25,500-25,400 zone.

The maximum Call open interest was observed at the 26,000 strike, followed by the 26,200 and 26,100 strikes, with the maximum Call writing at the 25,800, 26,000 and 25,900 strikes. On the Put side, the 25,500 strike holds the maximum Put open interest, followed by the 25,600 and 25,400 strikes, with the maximum Put writing at the 25,400, 25,200 and 25,650 strikes.

India VIX

Meanwhile, the fear index India VIX signalled discomfort and caution for bulls as it rallied 15.61 percent during the week to 10.93. It also touched the short term moving averages in last two-week uptrend. The bulls may be at risk if it surpasses 12 zone, experts said.

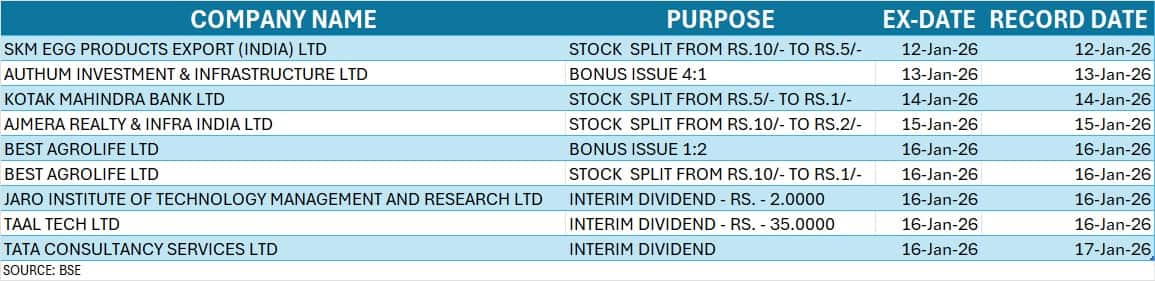

Corporate Action

Here are key corporate actions taking place this week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.